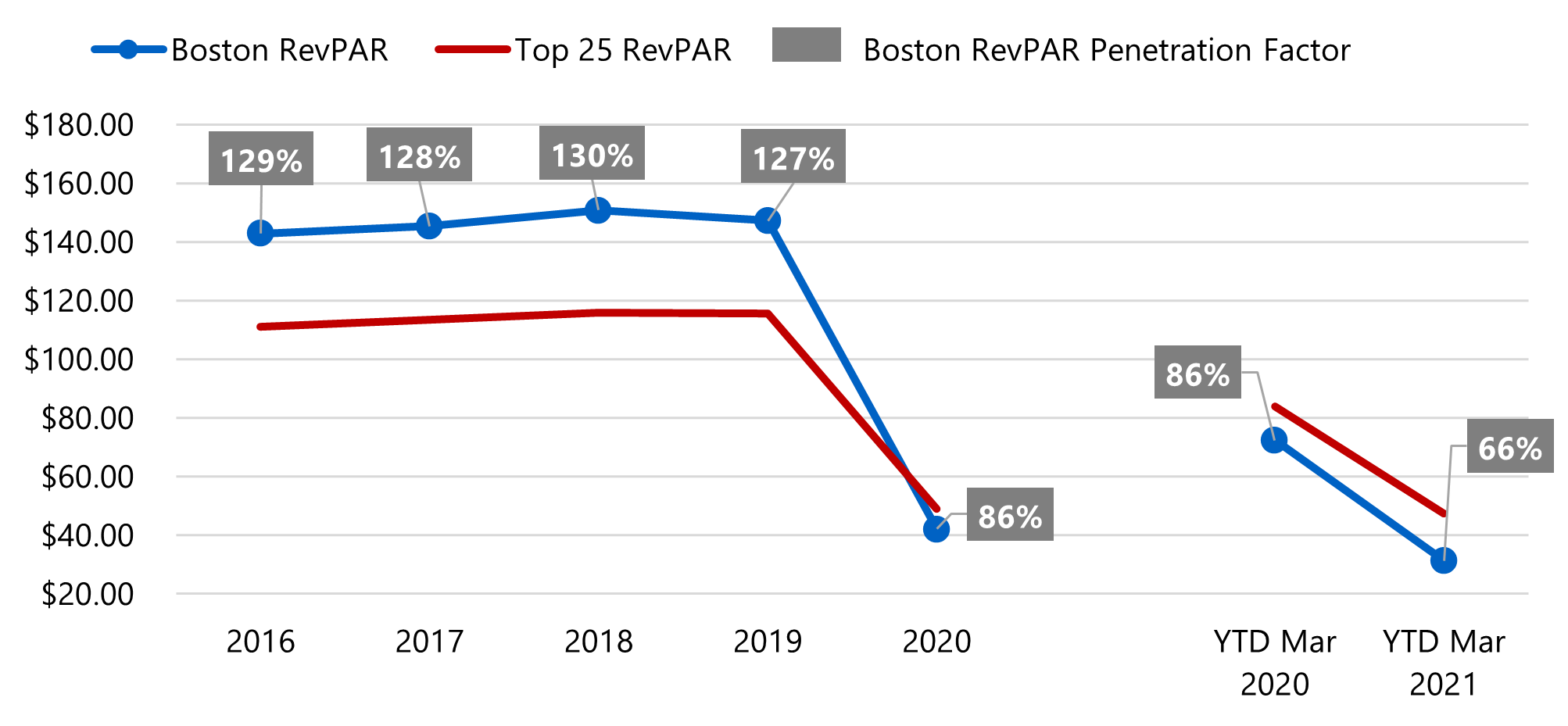

According to STR, Boston’s revenue per available room (RevPAR) fell by more than $100 last year, from $147 in 2019 to $42 in 2020, recording a 71.3% decline that was severe by any measure, but also when compared with that of other major metropolitan areas. Per STR, the Top 25 U.S. markets’ RevPAR fell by 57.6% in 2020. The key reasons for the disproportionate impact on the Boston hotel market follow.

According to STR, Boston’s revenue per available room (RevPAR) fell by more than $100 last year, from $147 in 2019 to $42 in 2020, recording a 71.3% decline that was severe by any measure, but also when compared with that of other major metropolitan areas. Per STR, the Top 25 U.S. markets’ RevPAR fell by 57.6% in 2020. The key reasons for the disproportionate impact on the Boston hotel market follow.

- Boston traditionally accommodates a smaller leisure-segment contribution when compared with markets in warmer climates. Leisure demand has been the most resilient demand segment during the pandemic, and Boston’s leisure demand season is shorter than that of most major markets, especially those in the South and the West.

- Boston has a greater level of dependence on international travel than most major markets, which holds true across all three major segments (i.e., commercial, group, and leisure). International travel has been largely curtailed throughout the pandemic.

- Massachusetts mandated stricter travel restrictions than most other states given the severity of the local impacts. Boston was one of the pandemic’s early hot spots.

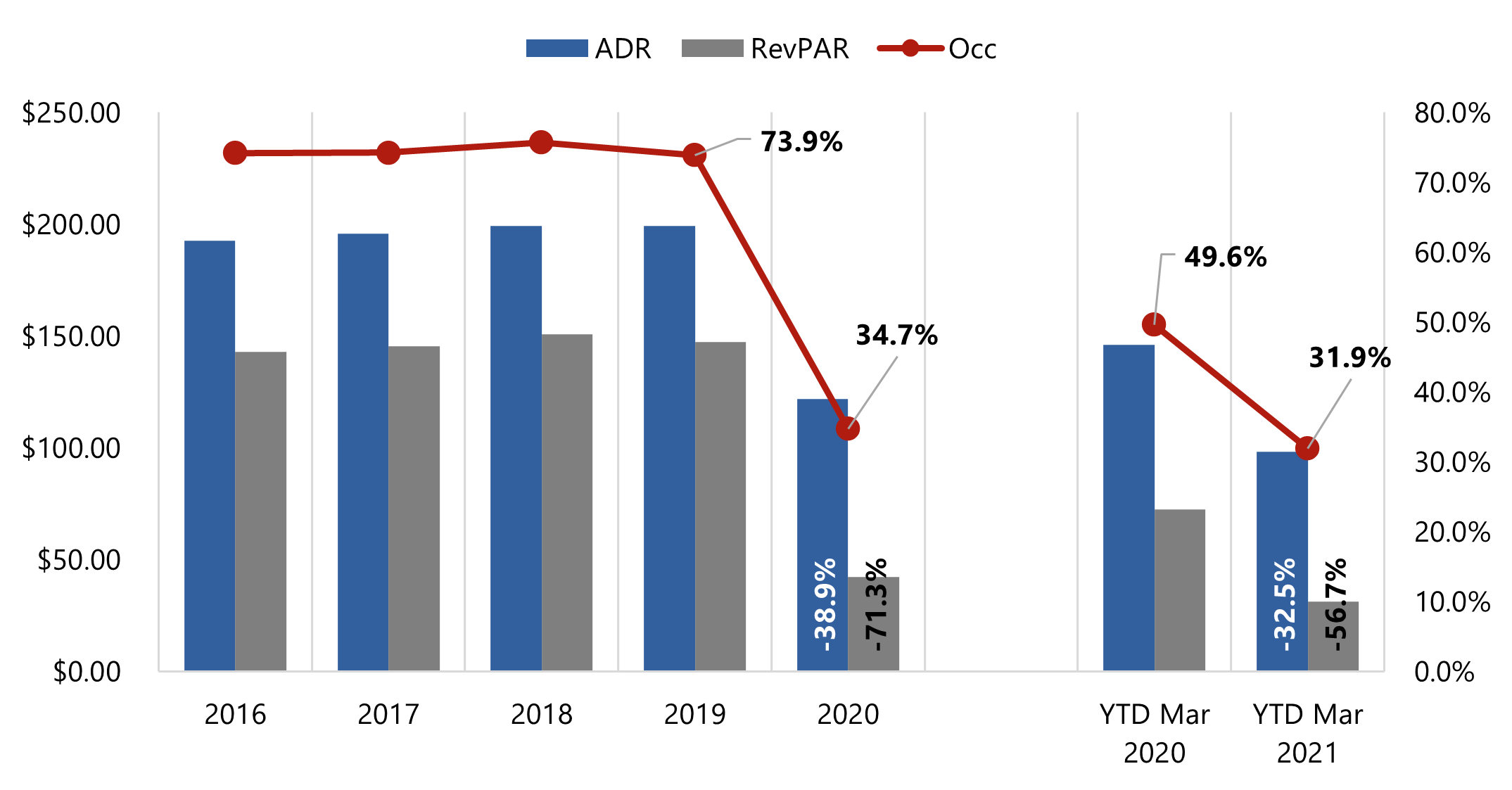

Boston MSA Hotel Trends

Boston MSA ADR, Occupancy, and RevPAR

Source: STR

Boston RevPAR vs. Top 25 U.S. Markets

Source: STR

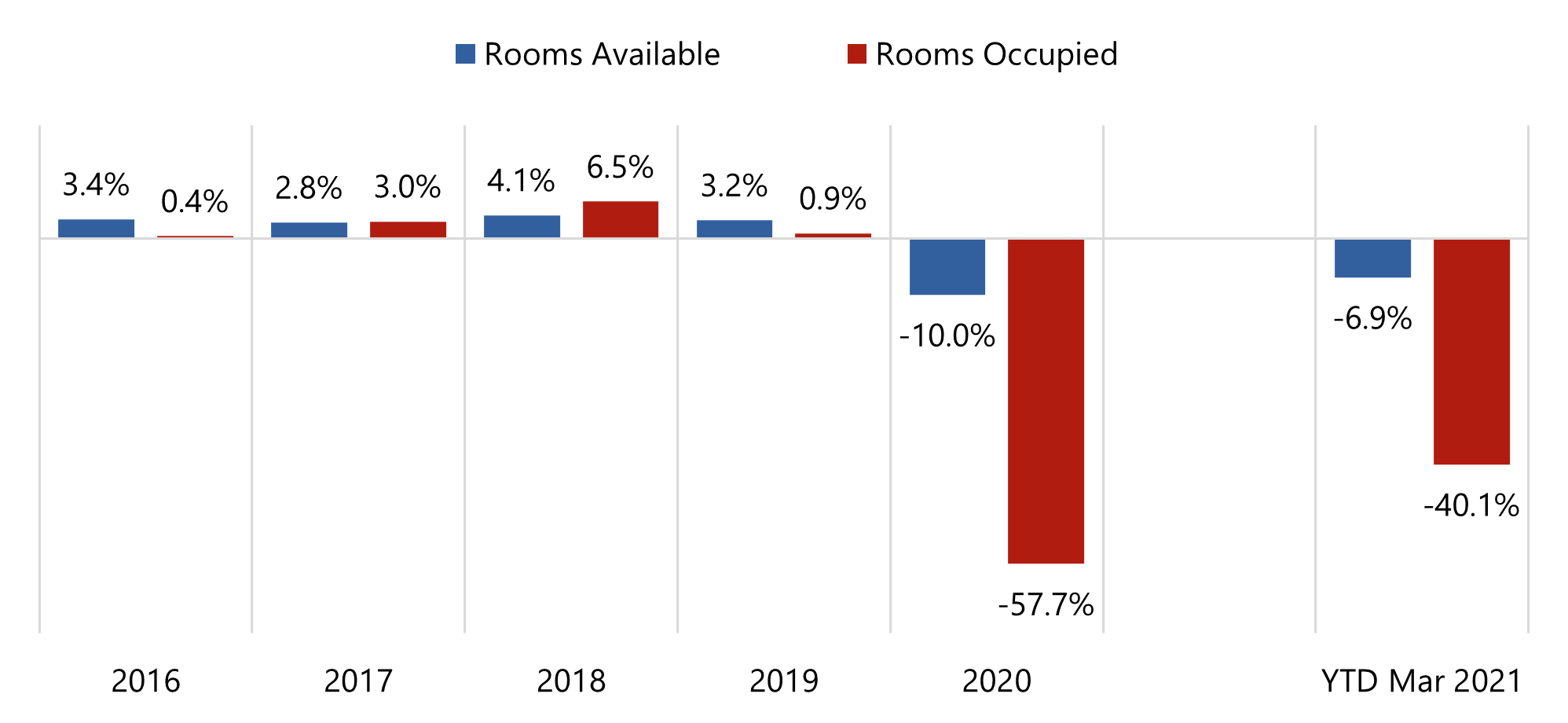

Historical Supply and Demand Changes

Source: STR

Demand Factors

- If citywide conventions are the Boston hotel market’s backbone, year-round commercial demand forms the rest of the skeleton, holding hotel operators over through the off-season and forming the occupancy base that allows hotel operators to leverage significant price increases in the summer and fall when leisure demand peaks. The outlook for recovery in both these demand segments is cloudy.

- Citywide conventions have a lengthy booking window, and although the city’s convention bureau is not starting from scratch, it will likely be years before the calendar (a) returns to pre-pandemic levels and (b) expands to absorb the new Omni (a 1,055-room convention headquarters hotel opening this summer).

- In the commercial segment, the risk that Zoom-style meetings will continue to supplant typical corporate travel is real, as are the potential impacts of a growing work-from-home culture and a movement away from traditional office-building occupancy. Additionally, in Boston, both segments are reliant on a significant share of international travel. Whereas Boston is not a convenient geographic locale for national conventions, it is central for international conventions whose delegates come primarily from the United States and Europe.

- As with the national lodging market at large, demand from domestic leisure travelers is the source of most if not all the Boston hotel market’s positive news. Consumer spending, propped up by the federal stimulus, is robust. Although most downtown Boston hotels have been sustaining operating losses through the pandemic, healthy leisure demand on weekends has softened the blow.

- Boston’s leisure segment is heavily reliant on sports events, such as the Boston Marathon and Red Sox, Bruins, and Celtics games, which historically drew travelers from all over the region. The Boston Marathon is traditionally held on Patriot’s Day (the third Monday in April). The 2020 Marathon was canceled, and the 2021 race has been delayed until October 11, 2021; moreover, it will be limited to 20,000 runners. The cancellation of the Marathon last year, coupled with event restrictions preventing spectators from attending sporting events in person, has further hampered the leisure segment in Boston. It should be noted that stadium capacity was increased to 12% in March 2021 and was increased further to 25% on May 10, 2021.

Transaction Activity

- Only one major downtown Boston hotel has transferred during the pandemic. The 245-room Hotel Commonwealth sold in November 2020 for $117 million, reflecting a 17% discount from its prior transaction in January 2016 for $136 million. This loss factor excludes the effects of value appreciation between January 2016 and March 2020, but the sale also closed before the approval of multiple COVID-19 vaccines was announced.

- A second major hotel sale occurred mid-pandemic across the river in Cambridge, where a 221-room Residence Inn by Marriott sold in October 2020 for approximately $486,000 per room.

New Supply Considerations

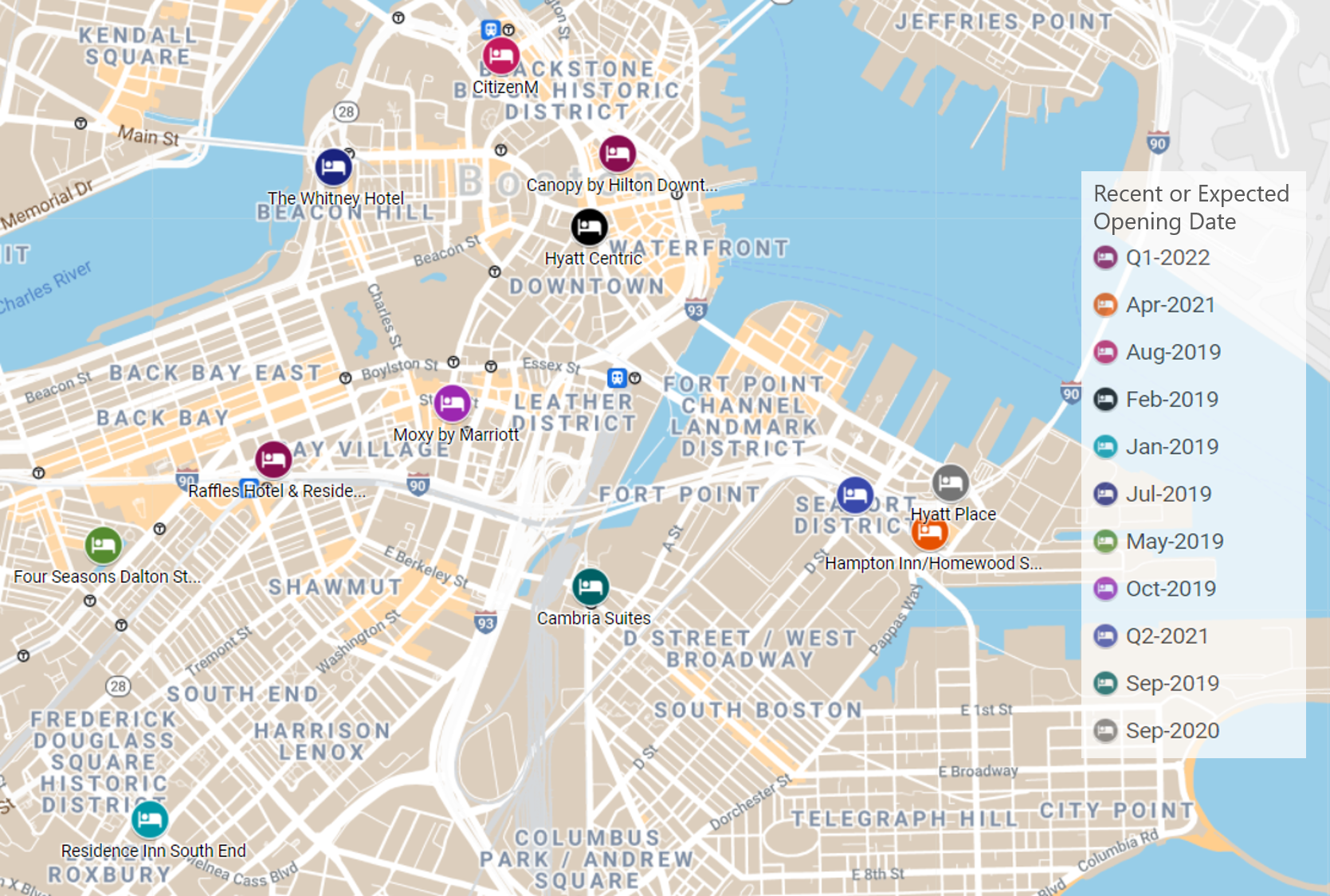

- The decreases in supply noted above are misleading. The market’s inventory has not been permanently reduced. The 10.0% and 6.9% supply loss factors in 2020 and in the year-to-date period through March 2021, respectively, reflect the impacts of temporary closures, including the 1,220-room Sheraton Boston, the city’s largest hotel. Instead, the market’s inventory level has continued to physically grow even while the number of rooms made available has decreased. Unfortunately, Downtown Boston will record a historic increase in hotel inventory through 2021, just as the market struggles with inconceivably low levels of demand. In addition, seven new hotels opened in 2019 and were still in the process of being absorbed when the pandemic began. The following map summarizes the downtown development pipeline as of May 2021.

- Of particular concern is increased congestion in the luxury sector, which has historically been limited to three to five hotels, depending on how this product type is defined. Once the Raffles Hotel opens in 2022, the sector will have doubled, adding another four hotels. Other entries include the renovated 312-room Langham and 286-room Newbury (formerly Taj) hotels, each of which closed in 2019 for redevelopment, with reopening dates slated for 2021. We note that these two hotels are not technically new supply and are excluded from the preceding table. Otherwise, the Four Seasons One Dalton, which had a soft opening mid-year 2019, was also still in the process of being absorbed when the pandemic began.

- The luxury sector expansion notwithstanding, the market’s major new supply factor is the 1,055-room Omni, the new convention headquarters hotel scheduled to open in June/July 2021, to be introduced at a time when the adjacent Boston Convention & Exhibition Center is largely idle. The Omni opening follows the completion of 705 other new hotel rooms (the Hyatt Place and the dual-branded Hampton and Homewood Suites by Hilton) in the Seaport/BCEC District within the last year, with these hotels having opened mid-pandemic.

Looking Forward

- Adverse pandemic-related impacts across all three of Boston’s primary demand segments are likely to be lasting for at least the next few years, and whereas atypical weakness in any one segment would have an adverse impact on hotel real estate values, the current challenges require unprecedented patience on the part of owners and lenders. The extent of the challenges in the Downtown Boston hotel market is daunting, but Downtown Boston is not unusual. The pandemic and its associated hotel-sector traumas have largely been urban phenomena. First-tier cities across the nation face similar conditions, with convention centers basically idle and the rebound in corporate travel yet to materialize in earnest. Nevertheless, investor interest in these same gateway cities remains high due to faith in their long-term return capacities; reports of massive capital stores looking for a home are numerous.

- Although this article highlights the challenges and ongoing adversity associated with the pandemic, most industry perspectives are optimistic. HVS and other industry experts generally project national RevPAR levels to return to pre-pandemic levels in 2024, supported by reasonable assumptions about (a) the mitigation of health risks associated with travel and in-person meetings through vaccines and public policy, and (b) the stabilizing effects of governmental intervention through stimulus spending.

- While the modern hotel industry has never faced a trauma like the COVID-19 pandemic, we know from previous disruptions and economic shocks that the arc of real estate value tends toward appreciation. As group and meeting restrictions continue to be rescinded, international travel resumes, and corporate travel patterns normalize, Boston will rebound. How long the recovery will take, and how complete it will be, remains to be seen.