Since December 2019, outbreaks of coronavirus (COVID-19) have led to global economic disruptions as cities and countries attempt to slow the spread of the disease by implementing lockdowns and social distancing measures. At the time of publishing this article, the number of cases in the United States and California exceeded 680,000 and 28,000, respectively. The federal government, along with state and local governments, has implemented restrictions to slow the spread of the disease, including stay-at-home or shelter-in-place orders. Major events have been canceled, and travel has been curtailed to “essential business” only. These measures, coupled with individual fears of contracting the disease, have profoundly affected the hospitality industry, in various aspects; this article looks at how the pandemic has affected lodging demand in Southern California and presents an outlook for the region for the months to come.

Beginning in early March, prominent events (e.g., sporting events, award shows, group conferences, etc.) in Southern California, similar to many regions around the world, were canceled or postponed. Major attractions such as Disneyland, Universal Studios, Knotts Berry Farm, Six Flags Magic Mountain, the Santa Monica Pier, Big Bear Resort, and Mammoth Mountain also quickly closed in response to the pandemic. On March 19, 2020, California became the first state in the country to issue a statewide “Stay at Home” order and, since that time, economic activity has ground to a halt; the order remains in place until at least May 15.

As can be imagined, the hospitality industry in the region, as with the rest of the country, is now reeling from the unprecedented drop in demand caused by these measures, which have resulted in substantially lower occupancies and average rates. For the combined L.A., Anaheim/Santa Ana, and San Diego lodging markets, RevPAR grew 3.2% in 2018, and then increased by only 0.3% in 2019; this weak performance was due primarily to the supply increase in 2019. Demand growth resumed in early 2020; up until the end of February 2020, hospitality markets in Southern California were on track to once again break records, reporting slightly higher RevPAR levels than those achieved during the same period of 2019.

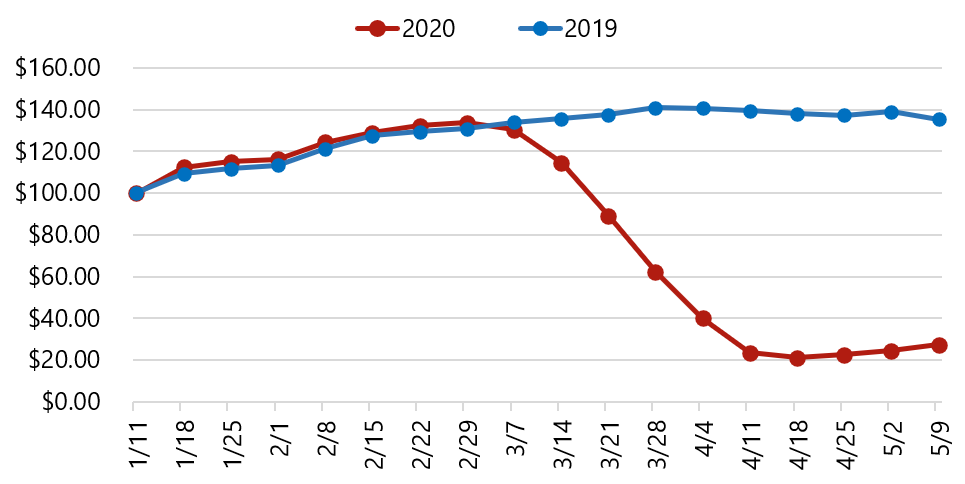

However, in the span of four weeks in March, the industry took a nosedive as travel came to a halt. As of mid-April, absolute occupancies in most markets were reported in the 15% to 25% range, with ADR levels dropping on average 40% to 45%. Ultimately, this resulted in a RevPAR decrease of 80% to 90% for most markets in the region (to an absolute level of approximately $20). The following chart illustrates weekly RevPAR performance thus far in 2020 compared to 2019 (on a running 28-day basis) for the aforementioned Southern California markets combined.

However, in the span of four weeks in March, the industry took a nosedive as travel came to a halt. As of mid-April, absolute occupancies in most markets were reported in the 15% to 25% range, with ADR levels dropping on average 40% to 45%. Ultimately, this resulted in a RevPAR decrease of 80% to 90% for most markets in the region (to an absolute level of approximately $20). The following chart illustrates weekly RevPAR performance thus far in 2020 compared to 2019 (on a running 28-day basis) for the aforementioned Southern California markets combined.

Southern California RevPAR

Source: STR

In California, as of April, all non-essential businesses and even parks have been ordered closed, with residents being allowed to work at or visit essential places of business, such as hospitals, pharmacies, grocery stores, and restaurants (for take-out/delivery only). Flights through LAX, as an example, decreased from over 1,600 per week in January to just 400 per week by early April. Without a doubt, travel, tourism, events, and conferences are now last on people’s mind, as mostly everyone remains at home across the country. Nevertheless, the start and length of the recovery will depend on the duration of the pandemic and on any other economic repercussions that may arise.

A reopening of the local economy is a complex issue. The governor’s office has identified six factors that need to be addressed prior reopening the economy, including increased testing, the protection of vulnerable populations in the state, the provision of PPE to hospitals and their staff, continued work with academics and research, the redrawing of floor plans in various facilities to allow for the continuation of social distancing, and the ability to reinstate more vigorous controls should the outbreak continue.

According to The Employment Situation report released on April 3, 2020, unemployment nationwide increased from 3.5% in February to 4.4% in March. Total unemployment claims from mid-March to mid-April have totaled 22 million; as such, national unemployment is on track to exceed 13% in the coming months. In California alone, jobless claims have exceeded three million since March, also suggesting an unemployment rate of at least 10% as of April. As time passes, it is now becoming more evident that the economic repercussions of this pandemic will be severe and are likely to last long after the virus dissipates.

Almost every industry will be affected by the outbreak of COVID-19. In the following section, we explore how three submarkets within this region are being affected by the pandemic.

A reopening of the local economy is a complex issue. The governor’s office has identified six factors that need to be addressed prior reopening the economy, including increased testing, the protection of vulnerable populations in the state, the provision of PPE to hospitals and their staff, continued work with academics and research, the redrawing of floor plans in various facilities to allow for the continuation of social distancing, and the ability to reinstate more vigorous controls should the outbreak continue.

According to The Employment Situation report released on April 3, 2020, unemployment nationwide increased from 3.5% in February to 4.4% in March. Total unemployment claims from mid-March to mid-April have totaled 22 million; as such, national unemployment is on track to exceed 13% in the coming months. In California alone, jobless claims have exceeded three million since March, also suggesting an unemployment rate of at least 10% as of April. As time passes, it is now becoming more evident that the economic repercussions of this pandemic will be severe and are likely to last long after the virus dissipates.

Almost every industry will be affected by the outbreak of COVID-19. In the following section, we explore how three submarkets within this region are being affected by the pandemic.

Los Angeles

In Los Angeles, the entertainment industry, including the powerhouses of Walt Disney Co., NBCUniversal, Paramount Pictures, Sony Pictures, and Netflix, among others, together with the Port of Los Angeles/Long Beach, contributed $1 billion to the economy alone daily prior to this downturn. As a result of COVID-19, The Hollywood Reporter estimated that just the shuttering of production on a variety of scripted and unscripted series, as well as a number of movies, could cost the industry at least $20 billion if things were to recover by May. To use Downtown Los Angeles as an example, a submarket of approximately 8,500 hotel rooms, approximately 30% of the hotels surveyed had suspended operations as of mid-April. The Los Angeles Convention Center has been converted to a field hospital for the foreseeable future and, while some events after June remain on the schedule, it is unlikely that conferences will return to the convention center for the remainder of the year given L.A. Mayor Garcetti’s announcement in April that large gatherings will likely be canceled through 2021.

Anaheim/Santa Ana

In Orange County, including Anaheim and Santa Ana, the tourism industry will be most affected given the shutdown of venues like Disneyland and Knott’s Berry Farm, as well as all beaches. The closure of Disneyland alone is estimated to cost the Southern California economy as much as $23 million per day, according to an economic impact study by Cal State Fullerton’s Woods Center for Economic Analysis and Forecasting. Our survey of hotels in Anaheim revealed that approximately 30% of the 130 hotels near Disney and Anaheim had also suspended operations as of mid-April. The Anaheim Convention Center has received cancellations through the summer, including the large-scale WonderCon and VidCon, which each attract thousands of attendees.

San Diego

Similar to all markets, San Diego will also be affected by the decline in tourism and the cancellation of a number of large-scale conferences, conventions, and self-contained groups, which typically drive demand for this market. A survey of over 40 hotels in Downtown San Diego revealed that approximately 20% had suspended operations as of mid-April. This percentage is less than in Los Angeles and Orange County, partly due to the closure of some large hotels, such as the 1190-room Hilton Bayfront and the 757-room Hotel del Coronado, which has somewhat benefited smaller properties. The San Diego Convention Center is currently serving as a temporary regional homeless shelter. Some events at the center have been canceled through early summer. The center’s signature event, Comic-Con, is still scheduled for July; however, while not officially canceled, the event is not expected to take place.

In light of COVID-19, as of mid-April, the California state government has procured 140,000 rooms throughout the state for healthcare workers that prefer to stay away from their homes and families. These workers are able to obtain subsidized vouchers to stay at nearly 1,000 hotels closer to their work sites. Also, to protect the homeless population from COVID-19, Project RoomKey has been established. This effort seeks to make approximately 15,000 hotel rooms available to house vulnerable homeless individuals. Approximately 7,000 hotel rooms throughout the state had been secured for this effort as of the writing of this article.

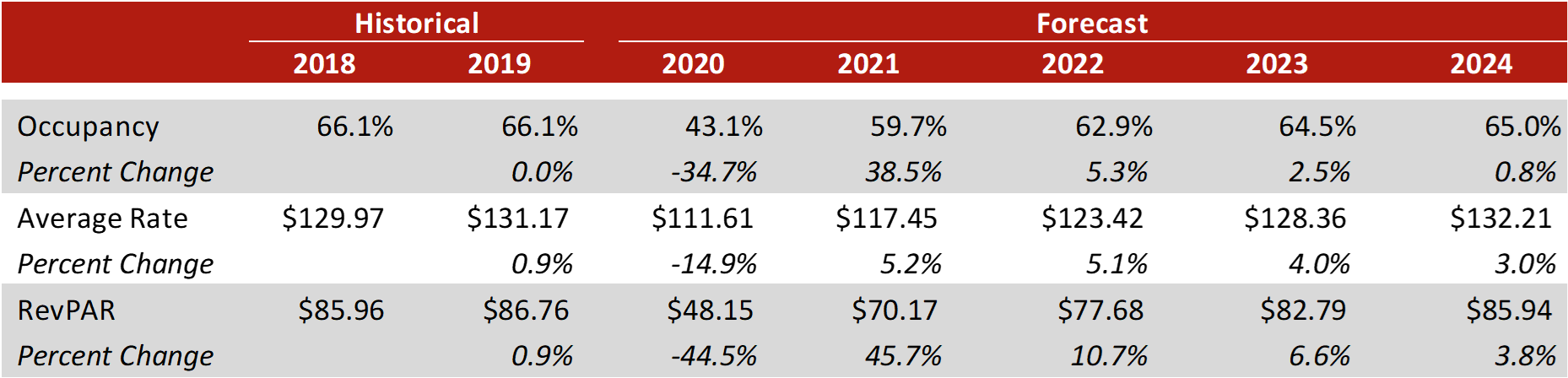

In view of the current environment, HVS’s national RevPAR outlook calls for a 44.5% decrease in 2020 because of COVID-19, followed by a 45.7% increase in RevPAR in 2021 as the market begins to recover. On a nominal basis, RevPAR is anticipated to recover by 2024, four years after the current outbreak. This recovery forecast is in line with the last two recessions, where a recovery also took four years. We note that the situation remains fluid; forecasts may change as time passes and as more clarity comes to light.

In light of COVID-19, as of mid-April, the California state government has procured 140,000 rooms throughout the state for healthcare workers that prefer to stay away from their homes and families. These workers are able to obtain subsidized vouchers to stay at nearly 1,000 hotels closer to their work sites. Also, to protect the homeless population from COVID-19, Project RoomKey has been established. This effort seeks to make approximately 15,000 hotel rooms available to house vulnerable homeless individuals. Approximately 7,000 hotel rooms throughout the state had been secured for this effort as of the writing of this article.

In view of the current environment, HVS’s national RevPAR outlook calls for a 44.5% decrease in 2020 because of COVID-19, followed by a 45.7% increase in RevPAR in 2021 as the market begins to recover. On a nominal basis, RevPAR is anticipated to recover by 2024, four years after the current outbreak. This recovery forecast is in line with the last two recessions, where a recovery also took four years. We note that the situation remains fluid; forecasts may change as time passes and as more clarity comes to light.

National Hotel Performance Forecast

Source: STR and HVS

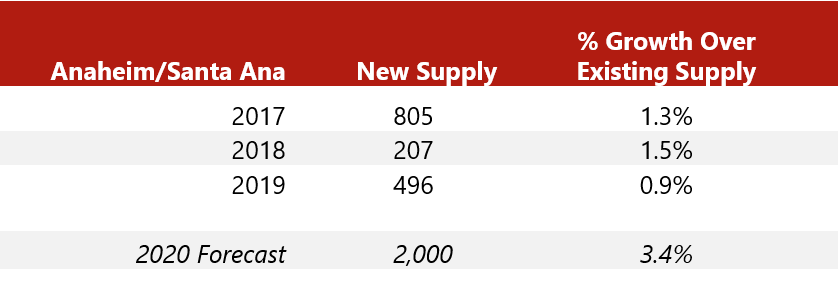

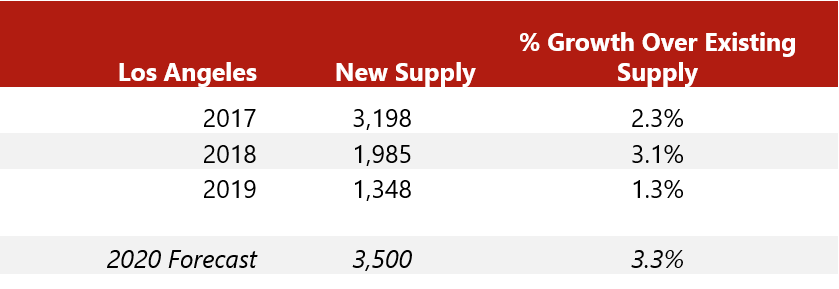

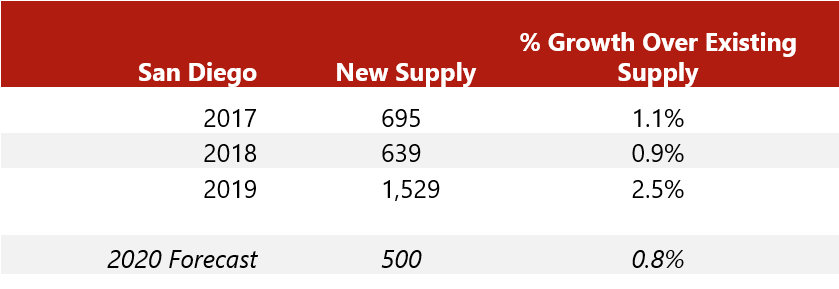

For Southern California, it is highly likely that the effects will be more dramatic and pronounced because of a couple major factors. To start, the region is amid a supply boom that was justified by the ever-increasing demand levels over the last decade. At least 6,000 hotel rooms were under construction throughout Southern California in early 2020 and expected to open this year. The table below illustrates increases in supply over the last three years and shows our forecast of new supply for 2020, based on hotels that are under construction with a planned opening this year.

New Hotel Supply Estimate

Source: HVS

It is still too early to determine the exact number of proposed projects that may stall or existing hotels that will suspend operations that may cause a temporary reduction in supply. As such, the table above does not yet factor in these changes; nevertheless, as mentioned previously, in three submarkets surveyed in Southern California, a total of 20% to 30% of hotels had temporarily suspended operations. As an additional point of reference, in mid-April, Marriott reported that approximately 25% of its hotels worldwide had suspended operations due to COVID-19. While many more rooms are in the pipeline for these various markets, with planned openings in 2021 and 2022, it is expected that many projects not already under construction will be placed on hold because of the drop in demand, coupled with a pullback in construction lending.

Projects under construction may also experience delayed openings due to supply chain issues, and some existing or proposed hotels may also undergo conversion to alternate uses. On the other hand, a deflation in construction costs caused by a drop in construction demand for new projects may also result in lower construction costs for some developers that retain a long-term view and choose to move forward with new developments over the next few years.

On the other hand, destinations in the area will benefit from healthy levels of “drive in” demand originating from within Southern California and from surrounding regions, such as Northern California, Arizona, and Nevada. Thus, hotels in tourist-dependent destinations that accommodate mostly leisure-related demand, such as L.A.’s beach submarkets, Anaheim, Palm Springs, Santa Barbara, and San Diego, for example, will feel the initial effects more but will also recover first. Hotels that accommodate primarily transient commercial demand would be expected to recover next, with hotels that focus on meeting/group demand recovering last.

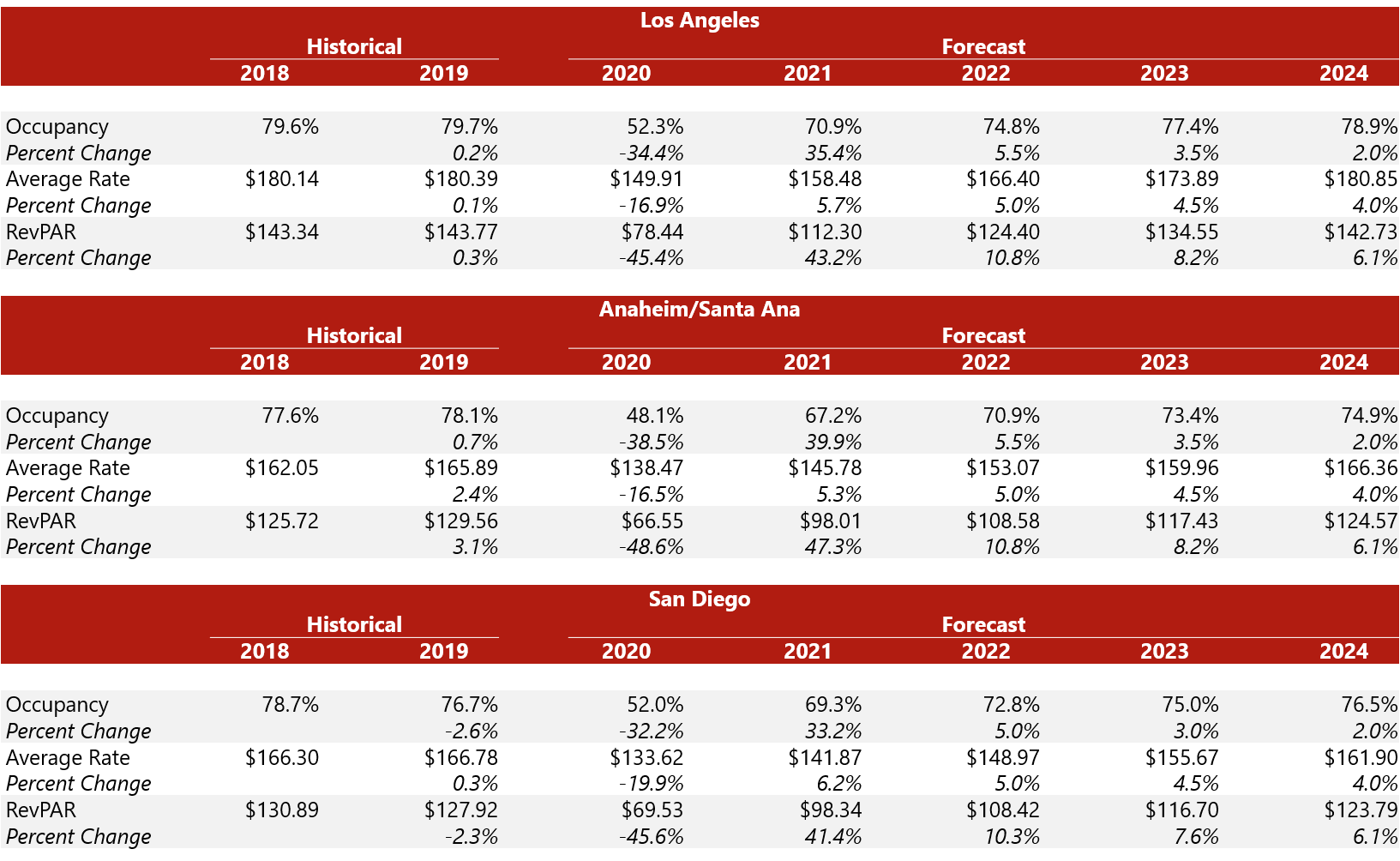

Although many conventions that are due to take place in the summer and fall have not yet been canceled, such as Comic-Con in San Diego, which is attended by over 160,000 people, it remains to be seen whether or not these too will be canceled or postponed if the crisis lasts longer than anticipated. Even if upcoming events are not canceled, the concern has also shifted to how attendance may be affected over the coming years by a decrease in corporate and personal spending as a result of the recent and ongoing economic ramifications. Taking into consideration the above factors, along with the performance of these markets thus far in 2020, we have prepared forecasts of occupancy, ADR, and RevPAR for Los Angeles, Anaheim/Santa Ana, and San Diego through 2024, as set forth below.

Projects under construction may also experience delayed openings due to supply chain issues, and some existing or proposed hotels may also undergo conversion to alternate uses. On the other hand, a deflation in construction costs caused by a drop in construction demand for new projects may also result in lower construction costs for some developers that retain a long-term view and choose to move forward with new developments over the next few years.

On the other hand, destinations in the area will benefit from healthy levels of “drive in” demand originating from within Southern California and from surrounding regions, such as Northern California, Arizona, and Nevada. Thus, hotels in tourist-dependent destinations that accommodate mostly leisure-related demand, such as L.A.’s beach submarkets, Anaheim, Palm Springs, Santa Barbara, and San Diego, for example, will feel the initial effects more but will also recover first. Hotels that accommodate primarily transient commercial demand would be expected to recover next, with hotels that focus on meeting/group demand recovering last.

Although many conventions that are due to take place in the summer and fall have not yet been canceled, such as Comic-Con in San Diego, which is attended by over 160,000 people, it remains to be seen whether or not these too will be canceled or postponed if the crisis lasts longer than anticipated. Even if upcoming events are not canceled, the concern has also shifted to how attendance may be affected over the coming years by a decrease in corporate and personal spending as a result of the recent and ongoing economic ramifications. Taking into consideration the above factors, along with the performance of these markets thus far in 2020, we have prepared forecasts of occupancy, ADR, and RevPAR for Los Angeles, Anaheim/Santa Ana, and San Diego through 2024, as set forth below.

Southern California Hotel Performance Forecast

Source: HVS, STR

Conclusion

Based on how other markets across the world have been (and continue to be) affected by the COVID-19 pandemic, the current expectation is that the worst of the effects in the United States will be felt in April and May, after which health and medical experts anticipate a decrease in COVID-19 cases and a slow resumption of economic activities. A recovery in demand in the hospitality space can be assumed to follow; nonetheless, the situation remains fluid and changes by the day.

While the 2020 COVID-19 pandemic will impact these various Southern California hotel markets, and a recovery will take time, it is important to remember that a recovery will ensue as soon as the trough is reached and as the pandemic and economic crisis subside. The hotel markets of L.A., Anaheim/Santa Ana, and San Diego encompass more than 225,000 hotel rooms, which hosted nearly 65,000,000 room nights in 2019, illustrating the depth of demand that has existed for the region over many years.

Whether it’s the entertainment industry, the tech sector, trade or manufacturing, the multitude of conventions, or the seemingly never-ending array of outdoor and leisure attractions, coupled with near-perfect year-round climate, the area’s economic drivers are deep and robust. Regardless of what emerges following the current situation, Southern California will likely once again be at the forefront of innovation, industry, trade, commerce, and leisure, as it has over many decades, all of which should benefit the hotel sector during the upcoming recovery.

HVS continues to regularly consult in California, with Consulting & Valuation offices in Los Angeles and San Francisco. Luigi Major, MAI, and his team are available to discuss the implications of COVID-19 on your asset or market and can assist you on any consulting needs that you may have.

While the 2020 COVID-19 pandemic will impact these various Southern California hotel markets, and a recovery will take time, it is important to remember that a recovery will ensue as soon as the trough is reached and as the pandemic and economic crisis subside. The hotel markets of L.A., Anaheim/Santa Ana, and San Diego encompass more than 225,000 hotel rooms, which hosted nearly 65,000,000 room nights in 2019, illustrating the depth of demand that has existed for the region over many years.

Whether it’s the entertainment industry, the tech sector, trade or manufacturing, the multitude of conventions, or the seemingly never-ending array of outdoor and leisure attractions, coupled with near-perfect year-round climate, the area’s economic drivers are deep and robust. Regardless of what emerges following the current situation, Southern California will likely once again be at the forefront of innovation, industry, trade, commerce, and leisure, as it has over many decades, all of which should benefit the hotel sector during the upcoming recovery.

HVS continues to regularly consult in California, with Consulting & Valuation offices in Los Angeles and San Francisco. Luigi Major, MAI, and his team are available to discuss the implications of COVID-19 on your asset or market and can assist you on any consulting needs that you may have.

About Luigi Major, MAI

Super insightful and well-written article Luigi, thank you!