We did see this coming. Last year had its significant challenges. Great uncertainty took hold with the announcement of the tariffs, disruption occurred in the government sector (and its normally steady demand) with DOGE efforts, and interest rate cuts didn’t occur until the last three Fed meetings of the year. Some cities had “off” convention years or closed their convention centers for reconstruction, the L.A. metro area experienced unprecedented fires, and other factors played key roles in diminishing our sector’s performance. And while this year’s challenges are not minimal by any means, last year was, quite simply, worse.

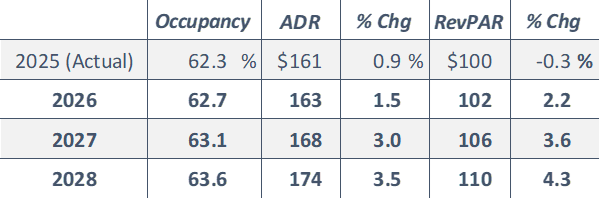

Our latest U.S. forecast is as follows.

HVS Forecast for U.S. Hotel Metrics Through 2028

Source: HVS, STR/CoStar

HVS offers the HVS MarketCast if you require an occupancy and ADR forecast for a specific market or submarket. Please reach out to me to learn more.

HVS offers the HVS MarketCast if you require an occupancy and ADR forecast for a specific market or submarket. Please reach out to me to learn more.

We can certainly hope that our government finds that “exit ramp” from the Middle Eastern conflict sooner rather than later, that Congress finds a path to resuming funding for the Transportation Security Administration (TSA), and that oil prices stabilize and inflation wanes. These possibilities, coupled with further potential interest-rate relief, should fuel continued economic growth and occupancy gains. ADRs will be lifted by special events this year, such as the highly anticipated FIFA World Cup. Better convention calendars are also on tap for certain cities, and atypical 2025 conditions in other cities (such as Austin and Houston) should not recur in 2026. Furthermore, if we enter a period of greater economic certainty this year, corporations are expected to bolster hiring efforts and travel budgets.

The industry’s overall average cap rate is on the decline, with transactions averaging 8.3% for Q4, similar to the 8.2% average for the year.

Source: MSCI Real Capital Analytics (Closed U.S. Hotel Transactions)

We expect average cap rates to trend downward in 2026, as we see more turnaround properties with challenged NOI levels being sold. These hotels, which often sell with a cap rate in the low single digits, will bring down the average that is blended with stabilized assets that sell at 8% to 9% cap rates. A normal cap rate in today’s market (for a stabilized or near-stabilized property) remains near the 8.0% to 8.5% mark, with an exit cap rate 100 basis points higher. Economy, extended-stay hotels and luxury hotels will likely trend below this level, while older limited-, select-, and full-service hotels facing a big renovation will likely trend above this mark.Sales activity is starting to pick up, albeit remaining at levels well below the prior peak. Slow improvement is being registered as declining interest rates are helping bridge the buy-sell gap in the market. Quarterly data for hotel transactions in the U.S. is shown below.

Number of U.S. Hotel Transactions Trended Modestly Upward in Most Recent Quarters

Source: MSCI Real Capital Analytics

Prevalent hotel discount rates are in the 10% to 11% range and could be lower for gateway markets, high-barriers-to-entry markets, luxury hotels, and high-performing economy, extended-stay hotels. Be wary of valuations that use exit cap rates and discount rates that are aggressively low, particularly if the asset is not in a high-barriers-to-entry area. A valuation with an exit cap rate in the 6% to 7% range in a low-barriers-to-entry market for a typical limited-, select-, or full-service hotel should flash yellow lights for your investment review team.

About HVS Leadership

At HVS Americas, our thought leadership is represented by our HVS Standards and Excellence Committee, comprising these leaders:

- Rod Clough, MAI, CRE, MRICS, President of HVS Americas

- Anne R. Lloyd-Jones, MAI, CRE, Director of Consulting & Valuation Services, National Practice Leader

- Katy Black, MAI, Managing Director, Leader of the Rocky Mountain Region and the HVS Americas Complex Consulting Group

- Tanya Pierson, MAI, ISHC, Senior Managing Director, HVS Minneapolis

- John Lancet, MAI, Senior Managing Director, Practice Leader of Southeast and Caribbean Regions

- Carrie Russell, AACI, MAI, RIBC, ISHC, Senior Managing Partner of HVS Canada

- Chelsey Leffet, Chief Operating Officer, U.S. Consulting & Valuation Division

- John Berean, Managing Director, HVS San Francisco and HVS Honolulu

- Ryan Mark, Senior Vice President, HVS Denver

- Marc Greeley, Senor Director, Leader of HVS Nashville Office

In total, we have a 35-person senior leadership team at HVS Americas composed of exceptional, experienced consultants. We are based in cities from Buenos Aires to Montreal and 40 additional cities in between, with teams covering all markets across North and South America. We will be closely monitoring how the year unfolds, and we are here to help when you need us.