Introduction

In a Mediterranean market increasingly defined by density and sameness, Formentera stands out as a deliberately low-rise, nature-led island whose “barefoot luxury” positioning translates into resilient demand and sustained pricing power.

Often described as Ibiza's bohemian sister, the island has built a clear premium identity around protected landscapes, iconic beaches, and a calm, design-forward atmosphere that prioritizes authenticity over spectacle. Despite its understated character, Formentera has become a discreet summer refuge for international high-net-worth visitors. In recent seasons, superyachts linked to figures such as Jeff Bezos and Andrey Melnichenko have been spotted along its coastline, reinforcing the island’s reputation as one of the Mediterranean’s most exclusive seasonal enclaves. Unlike larger resort destinations that compete through scale, global luxury hotel flags and entertainment intensity, Formentera’s competitive edge is its scarcity and simplicity, a proposition that appeals to high-intent leisure travelers and supports a market where value is created through experience, quality, and rate integrity rather than volume growth.

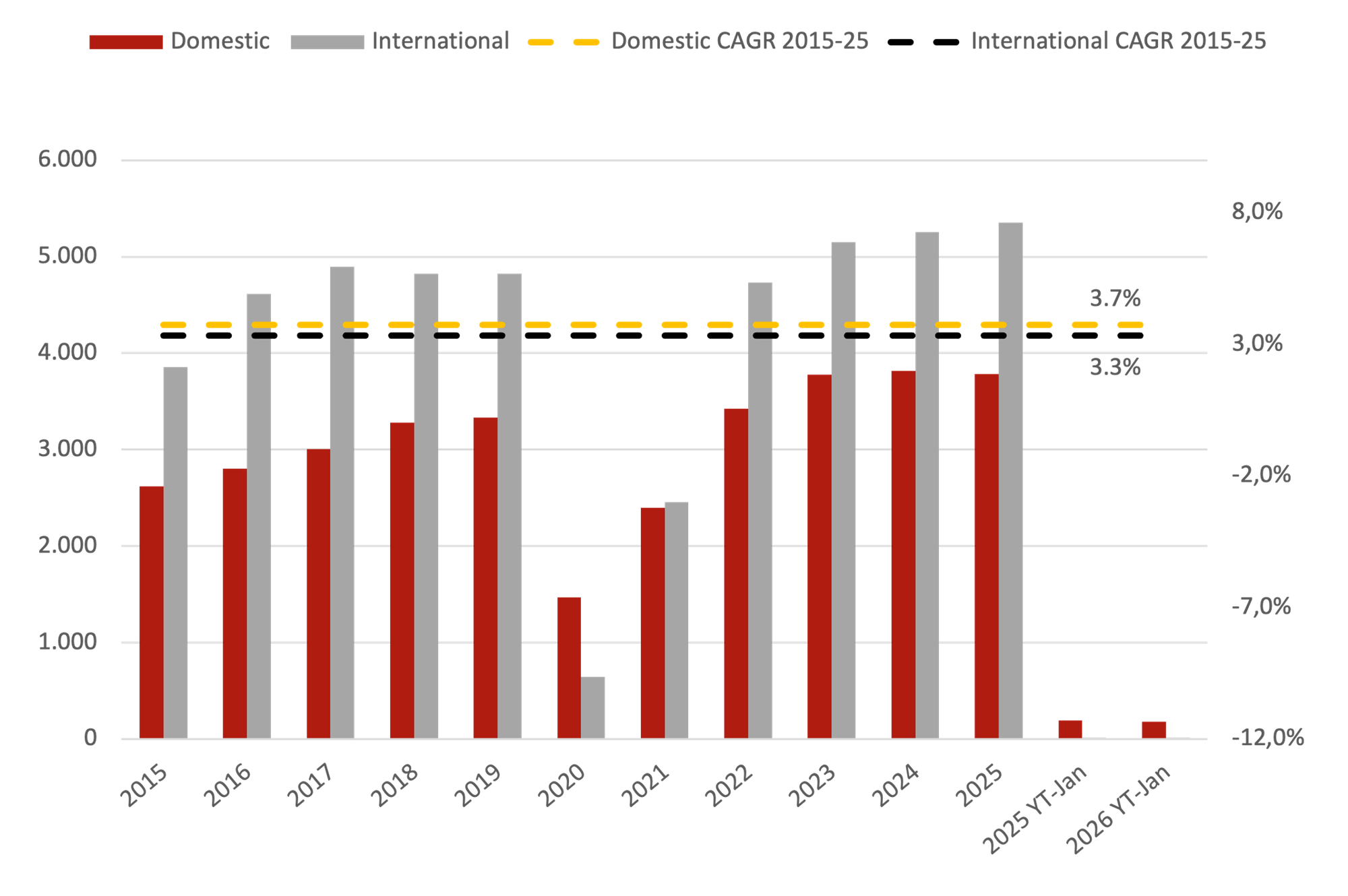

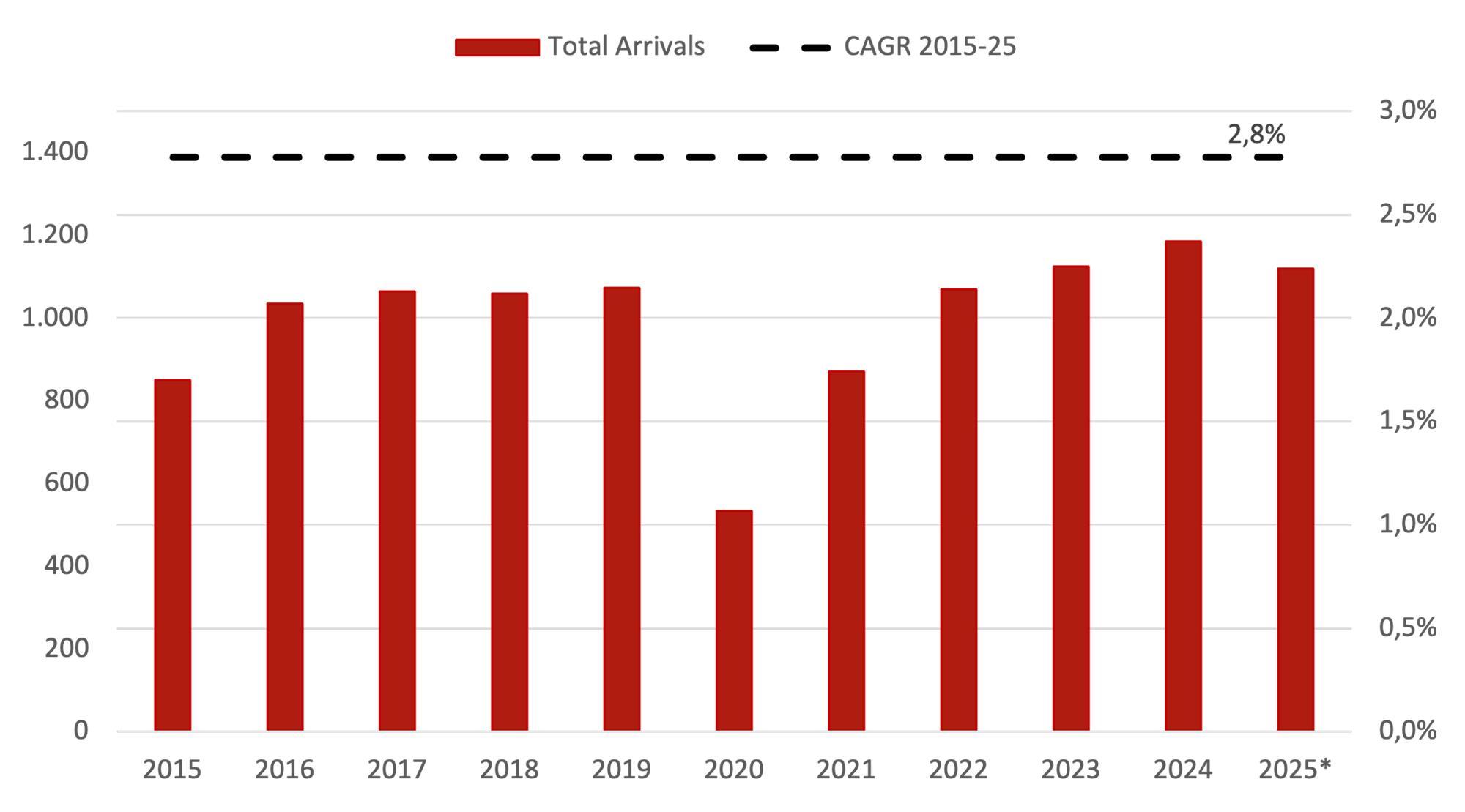

That identity is reinforced by the island’s access structure, which shapes demand as much as the product itself. With no airport, Formentera is effectively paired with Ibiza in a co-dependent access model: the most common route is flying into Ibiza and transferring by ferry (c. 30 minutes), making Ibiza the island’s functional international gateway. Formentera’s appeal lies in offering the proximity of Ibiza’s global connectivity while preserving a level of discretion increasingly rare in Mediterranean resort markets. As illustrated in Chart 1, Ibiza Airport arrivals have shown sustained growth over the past decade, providing the primary airlift that feeds demand into Formentera. This dynamic is mirrored in port flows in Chart 2, with La Savina (Formentera) recording approximately 1.19 million passenger arrivals in 2025 (January to November), underscoring the ferry network as both the island’s lifeline and a key operating constraint during peak week. In practice, it also makes Formentera unusually sensitive to Ibiza airlift, ferry capacity & frequency and intra-day congestion; factors that directly influence day-trip volumes, length of stay decisions, and the destination’s ability to protect rate integrity at the top end.

Chart 1: Passenger Movement - Ibiza Airport, 2015-25 (000s)

Source: HVS elaboration of IBESTAT data

Chart 2: Passenger Movement - La Savina (Formentera) Port, 2015-25 (000s)

*2025 data refer to January-November

This same “easy access & limited capacity” equation sits at the heart of Formentera’s sustainability discussion. Strong excursion demand supports local trade and reinforces visibility, but the concentration of day visitors has triggered debate around introducing a day-and-short-stay tripper tax, aimed at funding services and reducing pressure on fragile ecosystems, while balancing the need to protect accessibility and current visitor levels. Alongside this, Formentera’s offer remains intentionally narrow: beyond its beach and nature core, nightlife is minimal, and local stakeholders have pointed to licensing and safety constraints that make venue operations difficult to scale sustainably.

From a market perspective, however, the wider Ibiza–Formentera system continues to show resilience and pricing momentum. Reported results point to record tourist expenditure and demand that is increasingly consolidating beyond the traditional summer peak, supporting the view that the Pitiusas are gradually moving toward a more extended-season profile at the upper end of Mediterranean leisure.

Tourism Demand

Formentera’s demand fundamentals reflect a premium leisure destination operating within structural constraints. The island’s appeal, defined by beaches, nature, and a low-rise environment, translates into demand that is both high-intent and resilient, yet naturally capped by limited access channels and controlled accommodation supply. As a result, Formentera does not compete on volume. It competes on quality of stay, price acceptance, and repeat-driven loyalty, factors that typically define outperforming small-island markets.

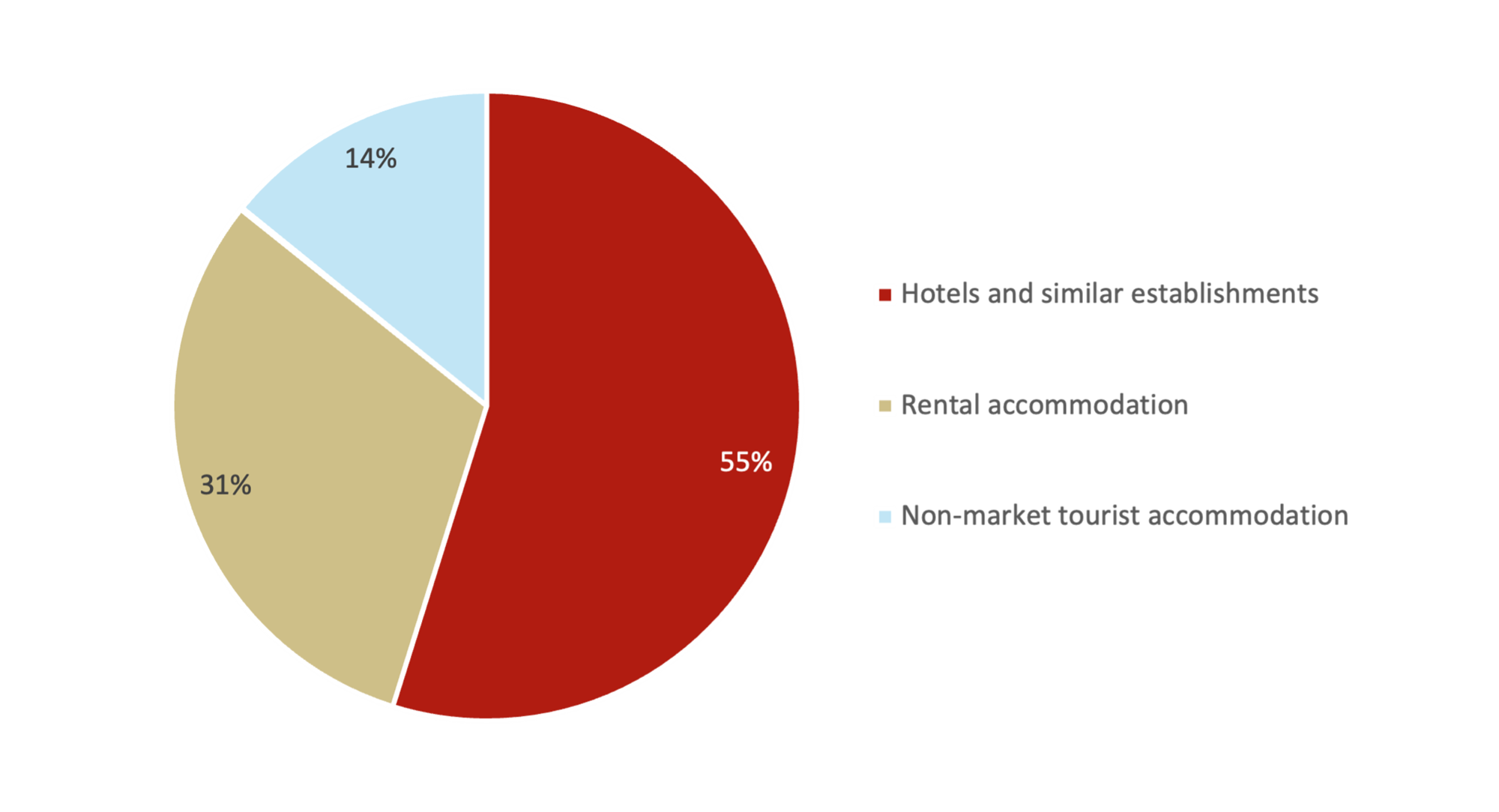

Before examining hotel performance in greater detail, it is important to understand how overall accommodated demand is distributed across lodging formats. As illustrated in Chart 3, 55% of tourist arrivals are recorded under “Hotels and Similar Establishments,” while rental accommodation accounts for 31%, and non-market tourist accommodation represents a further 14%.

It is worth noting that the “Hotels and Similar” category is a statistical classification that includes not only traditional hotels but also apartment-style establishments and other serviced accommodation formats. As such, the formal hotel market represents only a portion of this segment.

Source: HVS elaboration of IBESTAT data

The data confirms that Formentera’s demand base is structurally diversified across accommodation types. While serviced establishments remain the largest single category, a significant share of visitor flows gravitates toward rental and residential formats. This pattern is consistent with the island’s leisure profile, longer stays, family and group travel, and a preference for privacy and self-contained accommodation.

From a market perspective, this blended demand structure reinforces two dynamics. First, hotels operate within a broader ecosystem where alternative formats absorb a meaningful portion of volume. Second, well-positioned boutique and upper-upscale hotels compete not on scale, but on differentiation, leveraging service, design, and brand positioning to capture higher-spend segments within a supply-constrained environment.

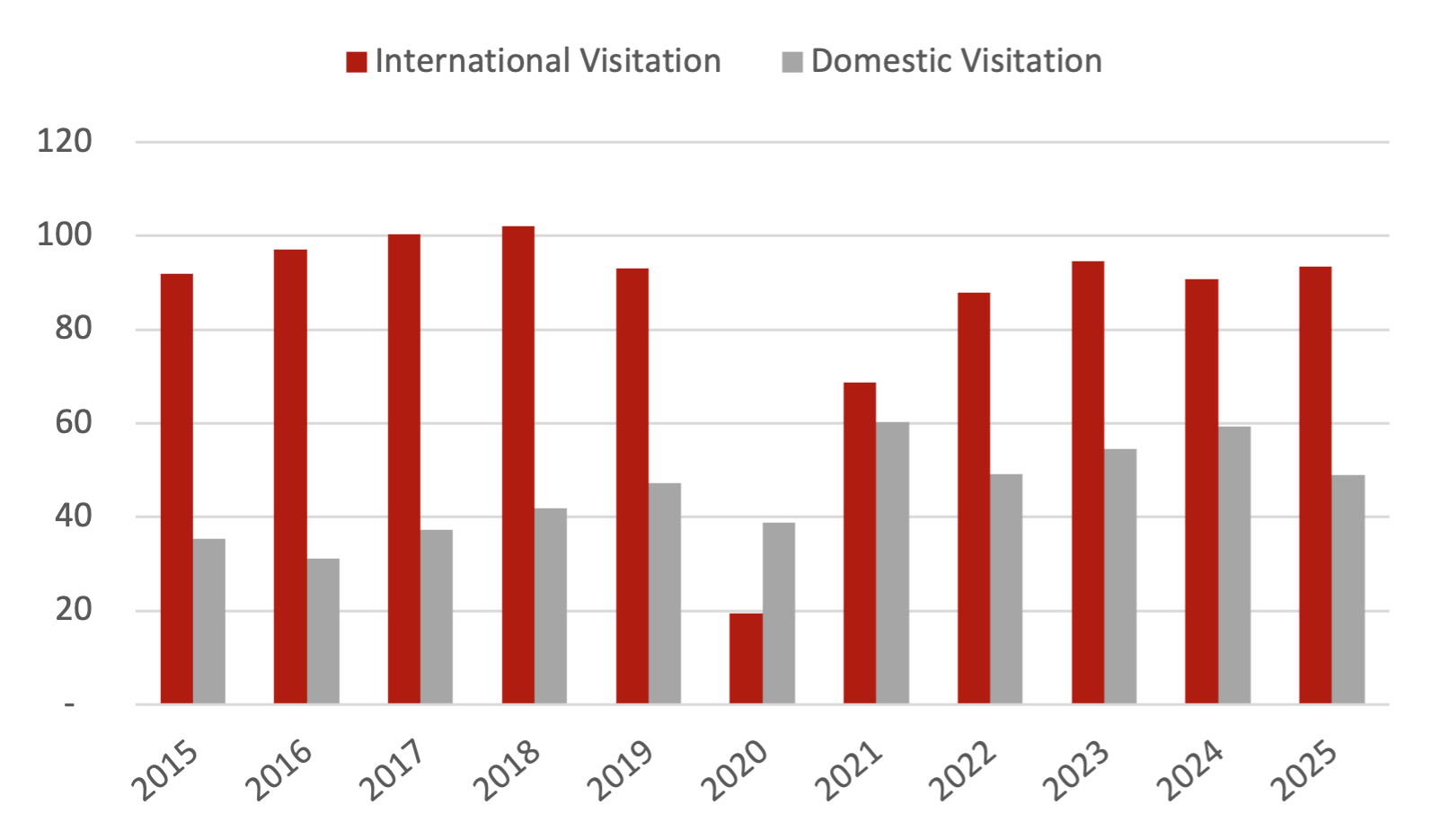

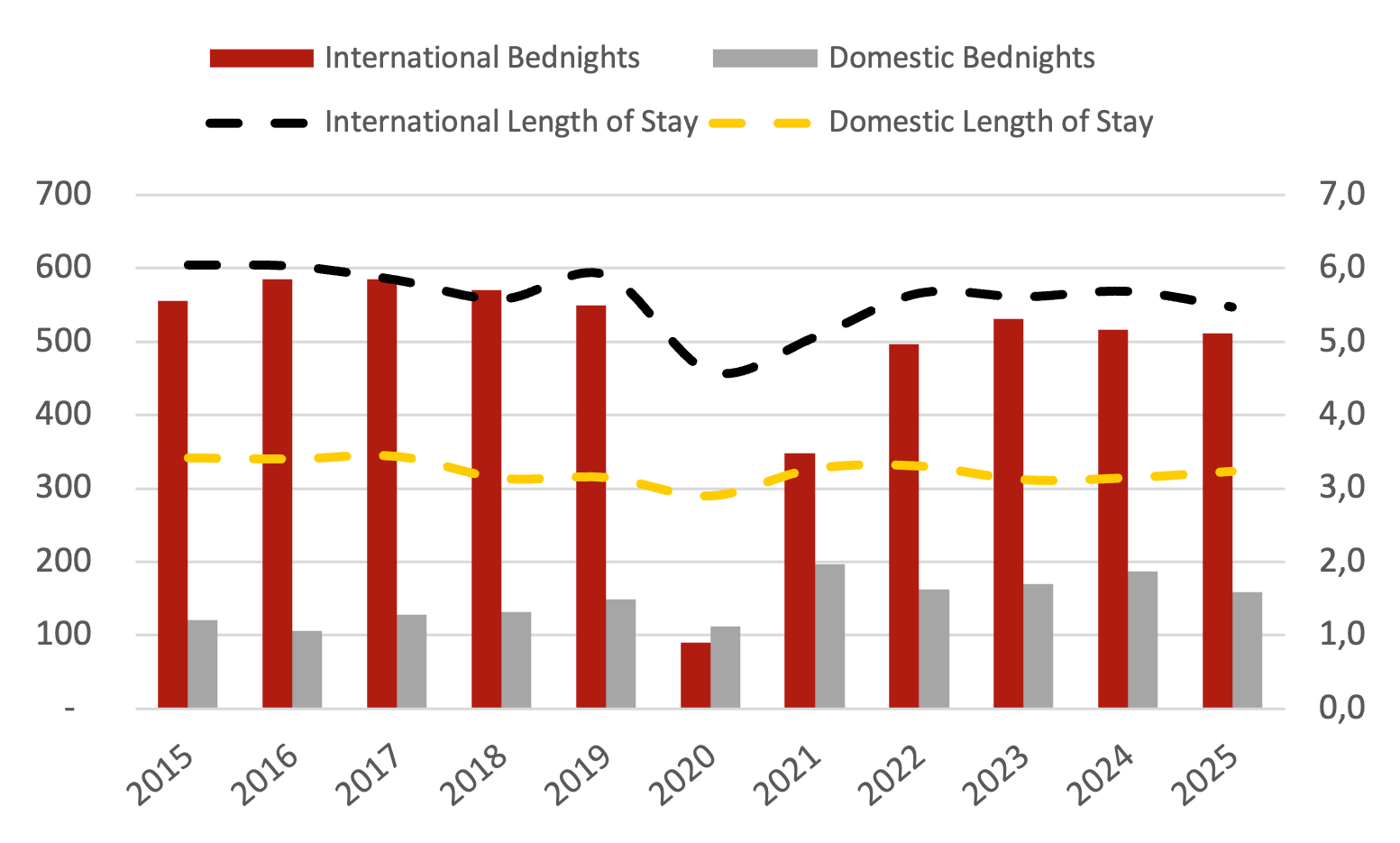

Charts 4 and 5 confirm the market’s long-term growth and its rapid post-pandemic normalization. Between 2015 and 2025, total hotel visitation increased from 127,247 to 142,396 (c. 1.1% CAGR), while hotel accommodated bednights remained relatively stable from 676,760 to 669,862 (c. -0.1% CAGR). The fact that visitation has outpaced bednight growth suggests a gradual shift toward shorter stays and a higher share of excursion-led travel, a pattern commonly observed in capacity-constrained island destinations. In this context, performance is increasingly shaped not by sheer volume growth, but by how effectively the destination captures value through peak compression, trading mix, and rate discipline.

The composition of demand further supports Formentera’s premium positioning. International visitors continue to contribute the majority of bednights due to longer stays. In 2025, international guests represented roughly 65.6% of total visits, yet generated around three quarters of total bednights, supported by a materially longer average length of stay (5.5 nights) versus domestic travelers (3.2 nights). The persistence of this gap over time points to a structurally favorable demand profile: Formentera is not only attracting international travelers, but is also capturing international travelers who stay, consume, and return. For many repeat visitors, the island functions less as a one-off holiday destination and more as an annual ritual that is anchored in beach clubs, serene landscapes, and a tightly curated hospitality scene.

Chart 4: Hotel Visitation - Formentera, 2015-25 (000s)

Source: HVS elaboration of IBESTAT data

Chart 5: Hotel Accommodated Bednights - Formentera, 2015-25 (000s)

Source: HVS elaboration of IBESTAT data

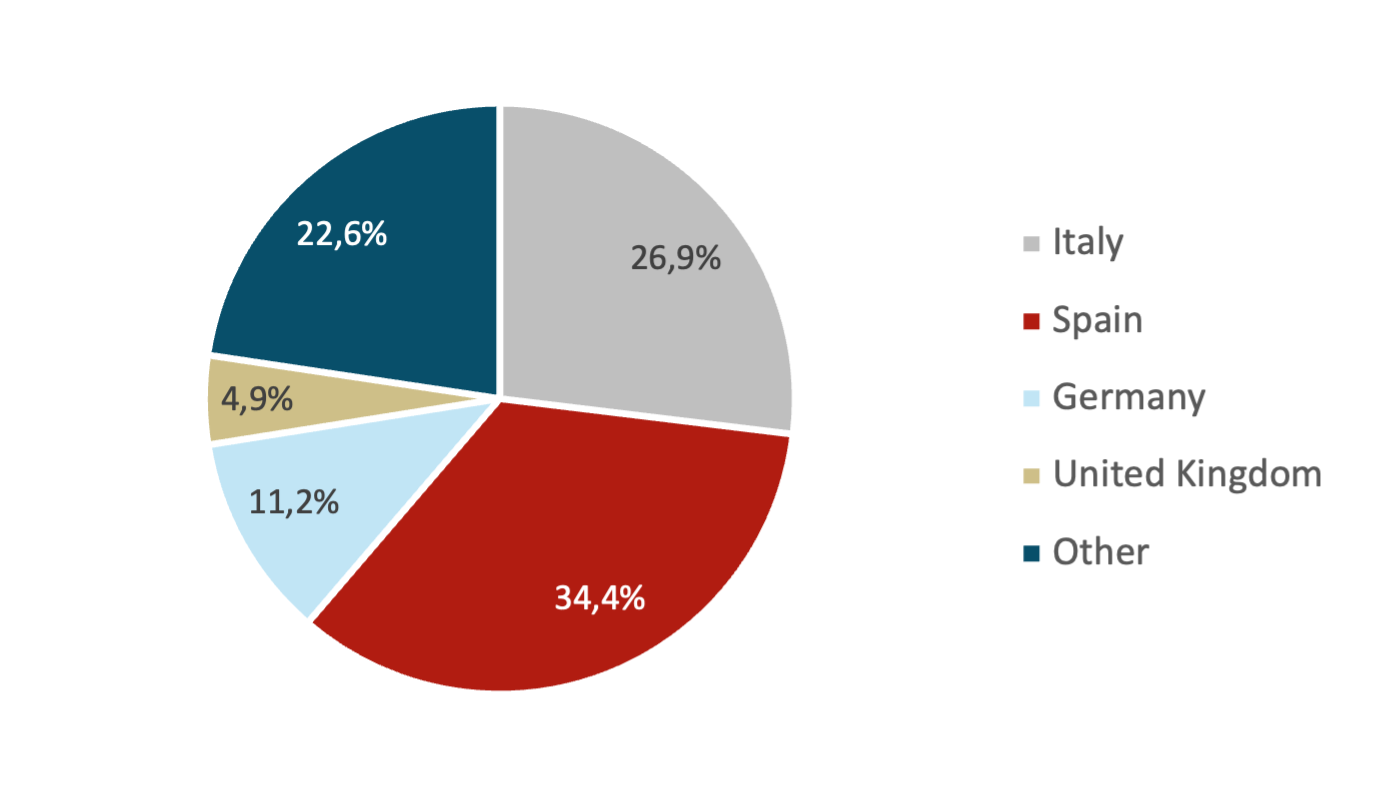

The geographic composition of demand further reinforces Formentera’s position within the Mediterranean leisure landscape. As illustrated in Chart 6, Spain and Italy remain the island’s two dominant feeder markets, accounting for approximately 34.4% and 26.9% of total arrivals in 2025, respectively. Germany represents a further 11.2%, while the United Kingdom and France contribute smaller but stable shares.

This structure highlights two important characteristics. First, Formentera’s demand base remains Mediterranean-centric and culturally aligned, supported by strong air connectivity into Ibiza from Italy and mainland Spain. Second, the market benefits from a degree of diversification beyond its core domestic and Italian base, with Northern European markets providing incremental shoulder and peak-season support.

Over the 2018–25 period, the United Kingdom recorded the strongest compound growth among major markets, increasing its share of total arrivals, while Italy, Spain and France remained structurally important contributors despite short-term volatility. Emerging markets such as Portugal have shown above-average growth from a smaller base, suggesting gradual broadening of the island’s international reach.

Importantly, the source market mix supports Formentera’s pricing profile. Italian and Spanish visitors are typically well-acquainted with the island’s positioning and display strong repeat behavior, while Northern European segments tend to stay longer and support higher average spend. Together, this creates a balanced demand base combining repeat-driven stability with international spending power.

Chart 6: Hotel Visitation by Source Country - Formentera, 2025

Source: HVS elaboration of IBESTAT data

Hotel Performance

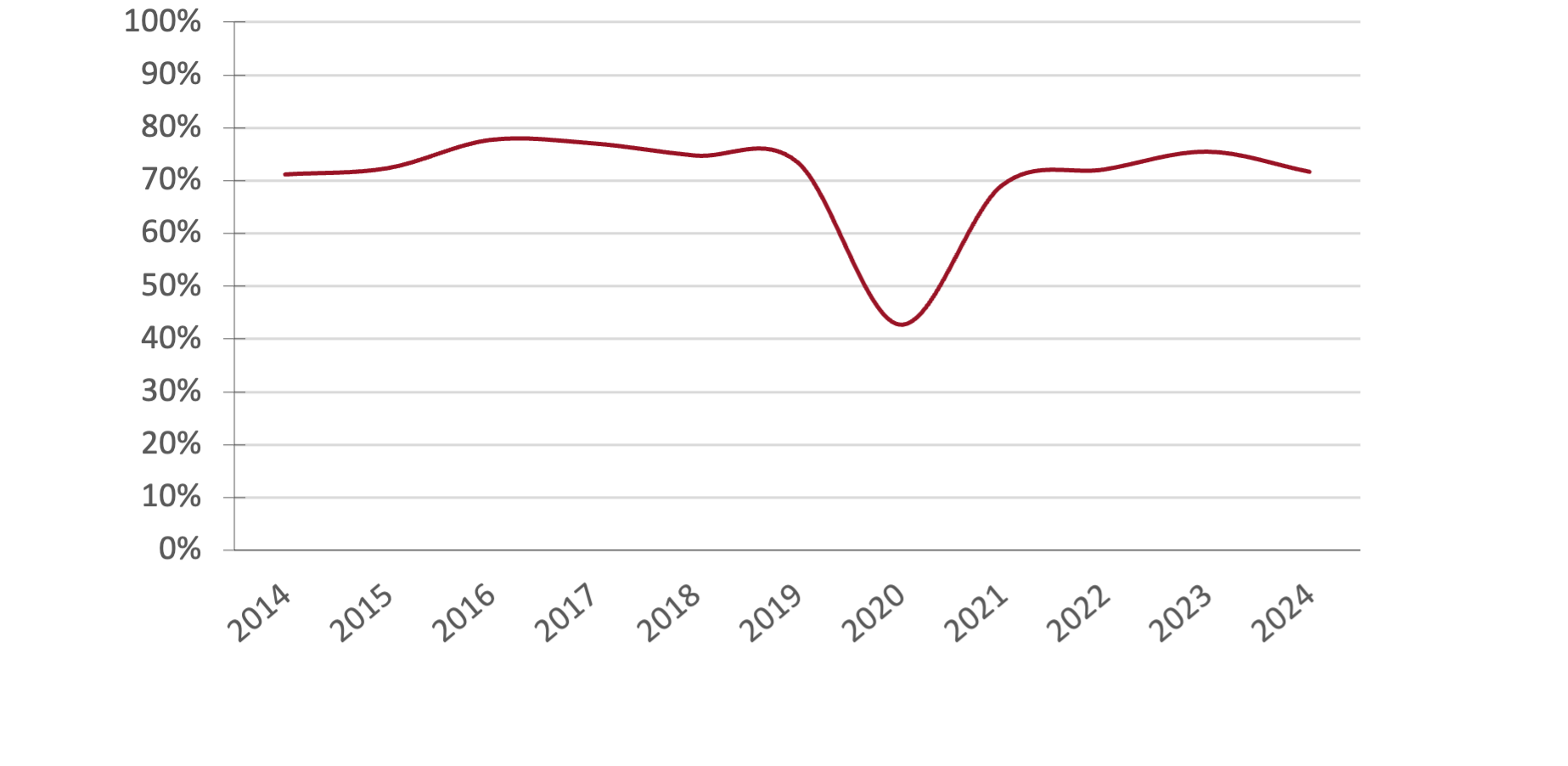

From an operating perspective, Chart 7 shows that hotel occupancy has remained remarkably stable over the decade, typically ranging between 70% and 80% in normal trading conditions. While 2020 represents an exceptional outlier, the broader trend suggests a market that consistently reaches a “full season” equilibrium, where occupancy becomes less a measure of whether demand exists, and more a reflection of how the season is shaped and monetized. In markets like Formentera, occupancy alone rarely tells the full story; upside is usually captured through rate leadership and shoulder season monetization, particularly when accommodation inventory remains constrained.

Crucially, revenue evidence supports this picture. According to latest data, hotels of Ibiza and Formentera closed 2024 as the highest RevPAR markets in Spain, reaching an average €153.8 RevPAR, a 5.9% increase year-on-year, and outperforming benchmark urban destinations such as Barcelona and San Sebastián.

Chart 7: Seasonal Hotel Occupancy - Formentera, 2014-24

Source: HVS elaboration of IBESTAT data

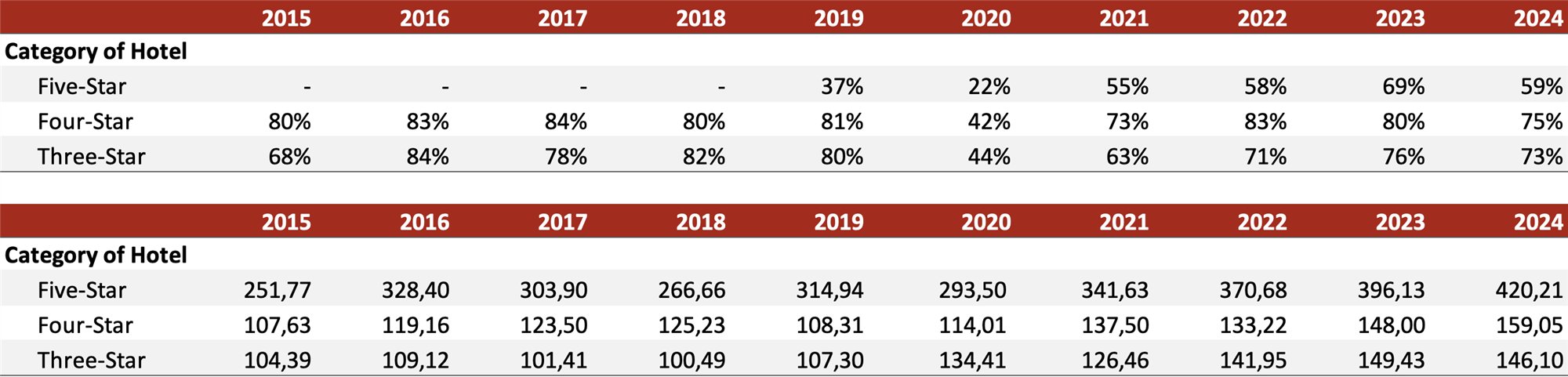

The category view in Table 1 adds another layer of confidence: the upper end of the market has rebounded strongly, with four-star occupancy reaching 75% in 2024 (and 80% in 2023), while five-star properties delivered 59% in 2024 after peaking at 69% in 2023. These levels underscore two points. First, premium demand has returned decisively. Second, the slight softening in 2024 should be read as normalization from an exceptionally strong 2023 and 2022, rather than a weakening of the destination’s fundamentals, especially in a small island market where year-to-year variations can reflect the mix between overnight stays and excursion-led activity, as well as the strength of shoulder trading. It should be noted that early-period rate category data (2015–2018) may reflect classification or reporting adjustments, as no formally classified five-star hotels were operating on the island during part of that period, and segment comparisons should therefore be interpreted with caution.

Table 1: Seasonal Hotel Occupancy and Average Rate by Category - Formentera, 2015-24

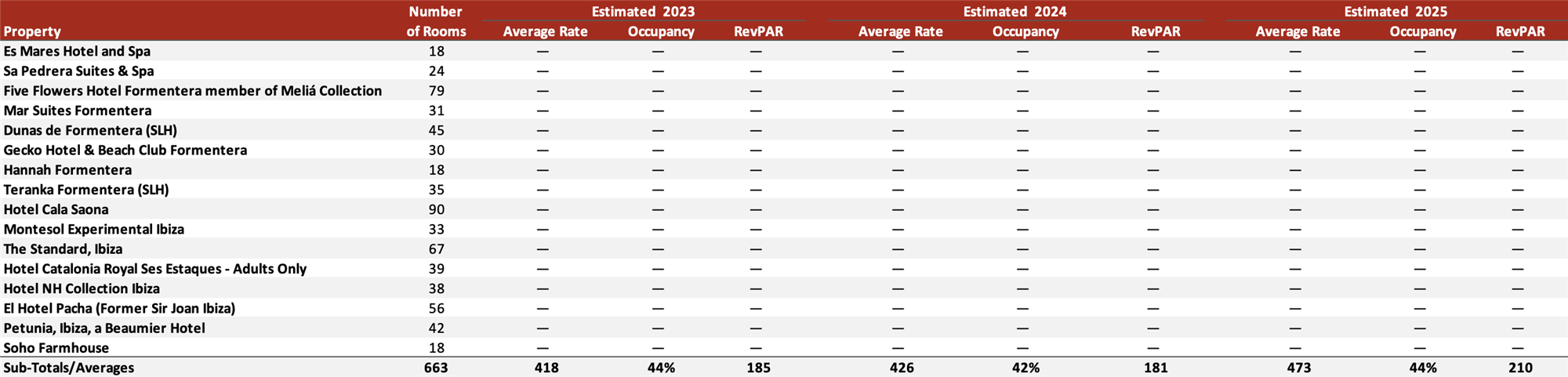

To better assess the forward average rate growth potential of boutique and upper-upscale hotels in Formentera, we analysed a set of 16 small luxury and high-end properties across Formentera and a select set in Ibiza. The sample includes hotels ranging between 18 and 90 keys (average c. 40 rooms), representing more than 600 total rooms.

As shown in Table 2, the competitive set achieved an average rate of approximately €473 in 2025, with occupancy of 44% (75% in seasonal terms), translating into a RevPAR of €210. The benchmarking indicates that well-positioned boutique assets within the Ibiza–Formentera ecosystem are already operating at rate levels materially above the island-wide averages shown in Table 1. In a structurally supply-constrained and premium-driven market such as Formentera, this suggests that future performance upside is more likely to be captured through continued rate progression rather than occupancy expansion.

Table 2: Upper-Tier Boutique Benchmarking Analysis – Formentera & Select Ibiza

Source: HVS Research

High-End Villa Market

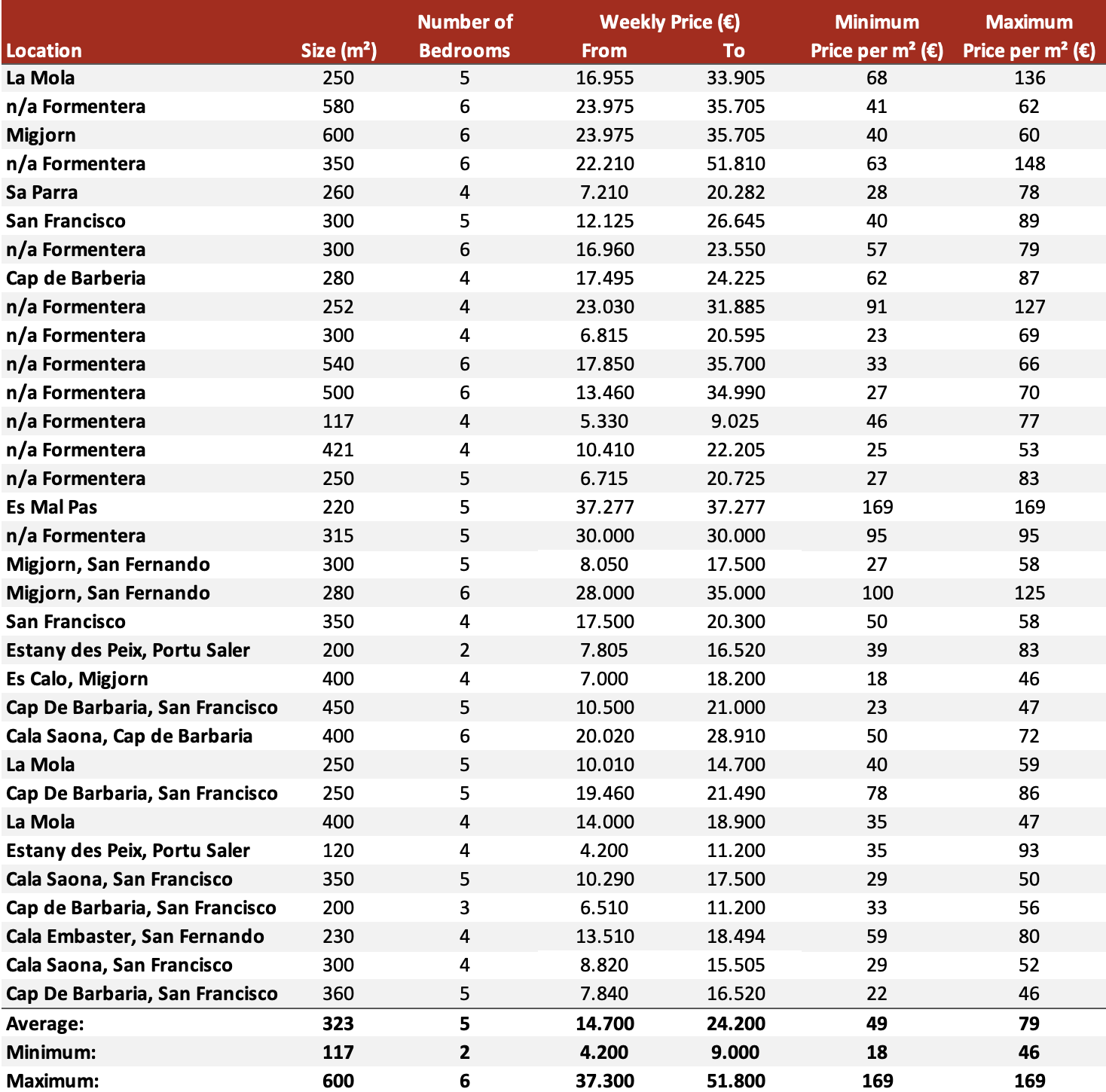

Beyond the formal hotel segment, Formentera’s luxury ecosystem is further shaped by a highly developed high-end villa market, which effectively establishes the upper boundary of pricing within the destination. Based on a review of premium listings across key micro-locations such as La Mola, Migjorn, Cap de Barbaria, and Cala Saona, typical luxury villas range between 250 m² and 600 m², with an average size of approximately 320 m² and five bedrooms.

Weekly rental rates in peak season range from approximately €4,200 – €9,000 at the lower end to €37,300 – €51,800 for trophy assets, with an observed average range of roughly €14,700 – €24,200 per week (equivalent to approximately €2,100–€3,500 per night). Exceptional frontline or design-led estates can exceed €50,000 per week (c. €7,000+ per night).

This pricing environment reinforces two structural dynamics. First, Formentera’s luxury positioning extends beyond hotels into the broader residential and lifestyle market, supporting its reputation as one of Spain’s most exclusive island destinations. During July and August, the island’s coastline regularly hosts a visible cluster of superyachts and VIPs, placing Formentera within the same Mediterranean luxury circuit as Capri and St. Tropez, albeit at a smaller, more controlled scale. Second, the presence of ultra-high-end villa inventory effectively anchors the destination’s rate ceiling, providing indirect support for boutique and upper-upscale hotels seeking to capture high-spend, privacy-oriented travelers within a professionally managed hospitality setting.

Table 3: Luxury Villa Market Overview – Formentera

Supply, pipeline, and regulatory constraints

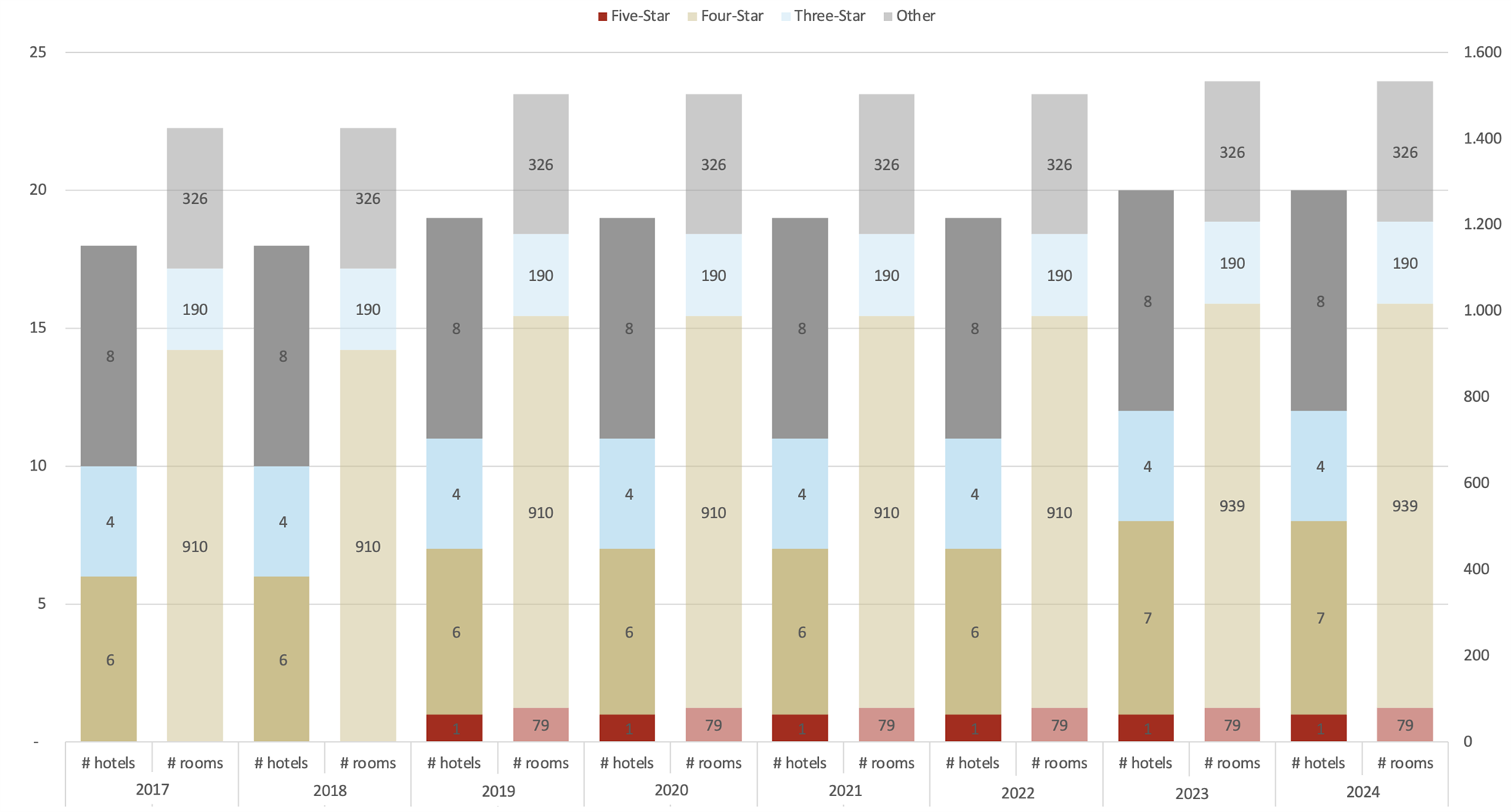

Formentera’s accommodation market is increasingly shaped by a clear strategic direction: managed tourism growth anchored in quality, sustainability, and long-term value protection. The island’s environmental sensitivity, low-rise character, and licensing discipline operate as structural guardrails that preserve the destination’s core identity and help maintain pricing power over time. In practice, this creates a market where value is typically generated through quality-led investment, renovation, repositioning and operational upgrades, rather than by pursuing large-scale volume expansion.As shown in Chart 8, Formentera’s formal hotel base remains modest in absolute scale and has evolved gradually in both property count and room inventory. Total hotel count increased from 18 hotels in 2017 to 20 in 2024 (c. 1.8% CAGR), while total room capacity expanded from 1,425 rooms in 2017 to 1,504 rooms in 2024 (c. 1.2% CAGR). Importantly, growth has been concentrated in the upper segments. The four-star category increased from 6 to 7 hotels over the period, with room inventory rising from 910 to 939 rooms, while the island established a formal five-star presence from 2019 onwards with the opening of Five Flowers Hotel (79 rooms).

This measured expansion, combined with a clear upward shift in room mix, reflects gradual premiumisation rather than scale-driven growth. In a structurally land-constrained island environment, room count discipline is as relevant as hotel count, reinforcing Formentera’s positioning as a quiet, low-density leisure destination where competitiveness is driven by experience, quality and rate integrity rather than inventory expansion.

Chart 8: Hotel Supply - Formentera, 2017-24

Source: HVS elaboration of IBESTAT data

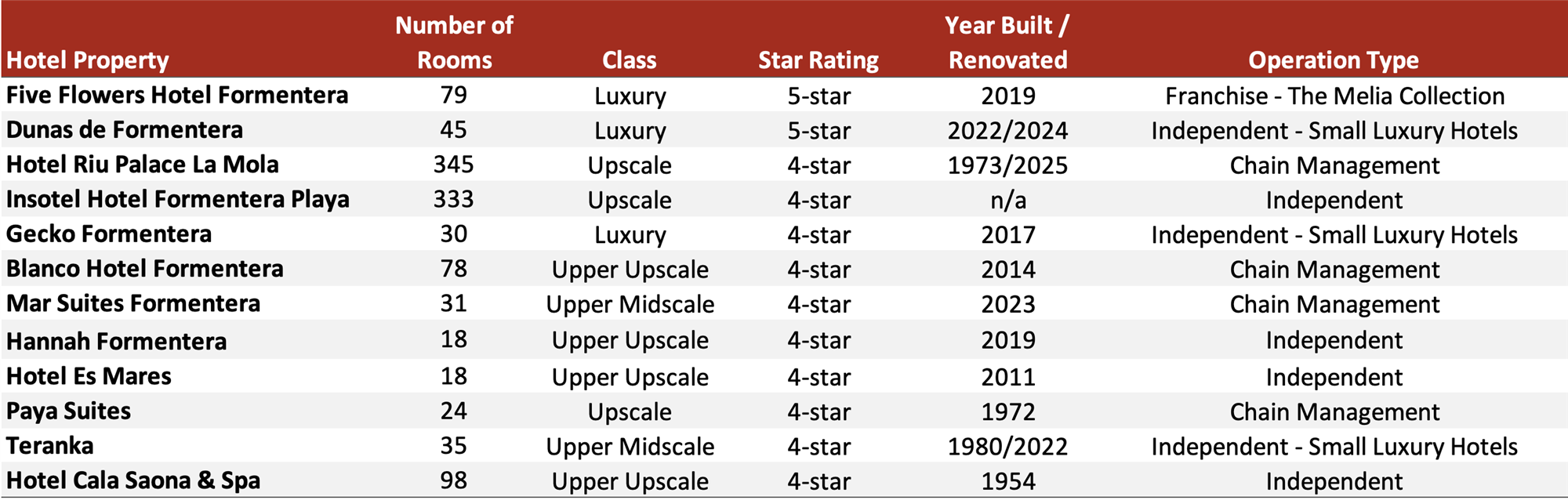

Beyond aggregate supply figures, the composition of the upper-tier hotel set provides further insight into Formentera’s positioning. As illustrated in Table 4, the island’s luxury and upscale inventory remains highly concentrated, with a limited number of properties operating above the 4-star level and only two clear five-star assets: Five Flowers Hotel Formentera and Dunas de Formentera. The remainder of the upper segment is composed primarily of established 4-star upscale and upper-upscale hotels, several of which have undergone recent renovations or repositioning.

Notably, branded penetration remains selective. While franchise affiliation exists through The Meliá Collection and management agreements with international owner-operators such as RIU, a meaningful share of the upper-tier inventory continues to operate independently or under soft-brand affiliations such as Small Luxury Hotels. This structure reinforces Formentera’s boutique-led character while leaving open the question of whether additional soft-branded luxury operators may seek exposure to the island’s premium, supply-constrained market dynamics. In addition, the upcoming Autograph Collection Formentera (34 rooms with expected opening in summer 2026) represents a measured step in international brand expansion, signaling growing institutional interest in the island’s upper-upscale segment.

Table 4: Luxury & Upscale Hotels - Formentera (2026)

Source: HVS elaboration of CoStar data

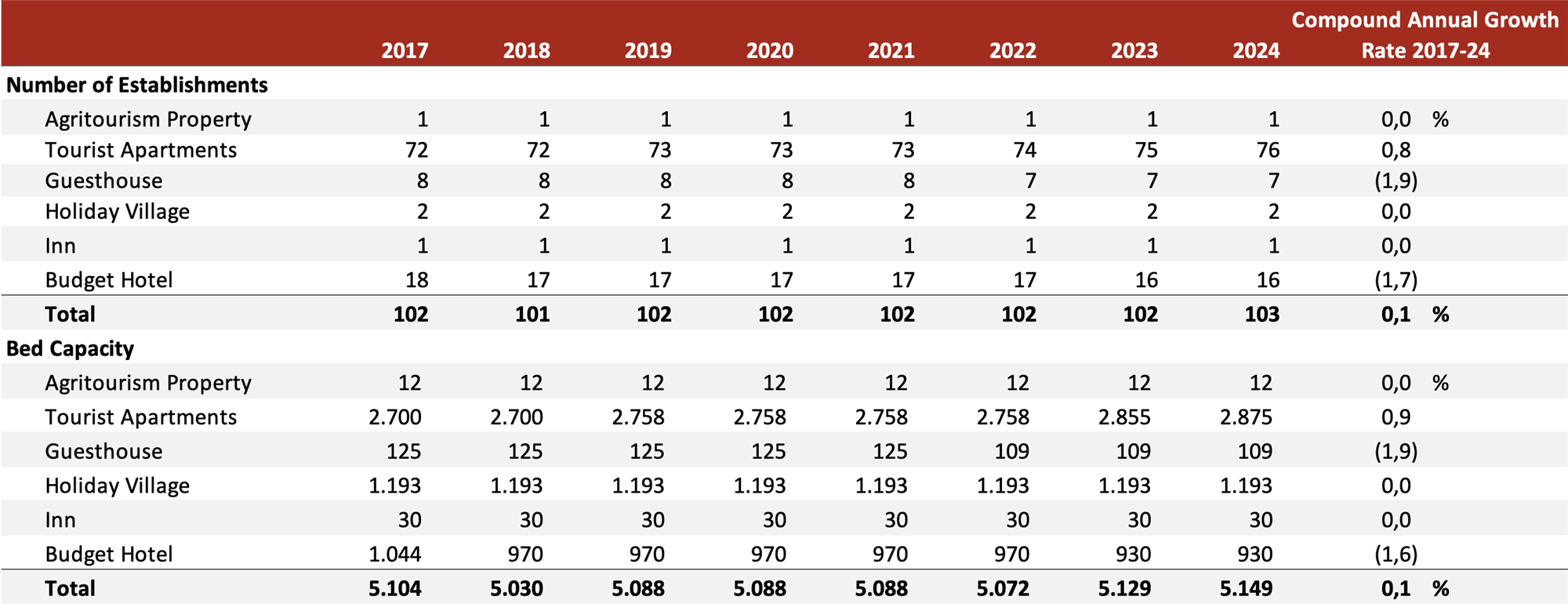

Building on the formal hotel base, the wider accommodation landscape in Formentera is also significantly shaped by alternative tourist establishments, particularly tourist apartments, which absorb a meaningful share of peak demand. As shown in Table 5, the alternative segment remained broadly stable between 2017 and 2024 at 103 establishments, with total capacity increasing slightly from 5,104 beds in 2017 to 5,149 beds in 2024 (c. 0.1% CAGR). Within this mix, tourist apartments represent the dominant format, totaling 76 establishments in 2024 with 2,875 beds, equivalent to roughly 56% of alternative accommodation bed capacity. This scale explains why recent regulatory direction has focused on strengthening oversight of vacation rentals and moderating further expansion, including the prohibition of new tourist accommodation in multi-family housing, with an emphasis on protecting residential use and ensuring legality and quality.

Table 5: Alternative Tourist Establishments - Formentera, 2017-24

Source: HVS elaboration of IBESTAT data

Conclusion

Formentera today operates as more than a resort destination; it functions as a seasonal luxury micro-market within the broader Mediterranean ecosystem. Its appeal is anchored in scarcity, discretion, and a tightly managed supply base that protects both brand identity and long-term pricing power. In peak summer weeks, when superyachts line its turquoise coastline and international high-net-worth visitors anchor in its coves, the island’s positioning is not theoretical, it is visibly validated.

For hotel owners and investors, this creates a distinctive operating environment. With limited developable land and firm regulatory guardrails, growth is unlikely to be driven by scale. Instead, value creation will continue to stem from selective upgrades, design-led repositioning, and the ability to align product with the island’s quiet-luxury ethos. In such a context, rate progression remains the primary performance lever, supported by a clientele that prioritizes experience, privacy, and authenticity over density.

The key question, therefore, is not whether Formentera can sustain demand, but how the next phase of premiumisation unfolds. As selective international brands and soft-luxury operators increasingly seek exposure to scarcity-driven island markets, Formentera stands positioned at the intersection of exclusivity and institutional interest, small in size, but firmly embedded within the Mediterranean’s top tier of seasonal luxury destinations.

This article also benefited from contributions by Audrey Gerken, Research Intern at HVS Southern Europe.