With contributions by Eric Guerrero, Neil Flavin, Brian Bisema, Marc Greeley, James Rebullida, and Brett Testa

Another exceptional Hunter Conference is in the rearview mirror, with much thanks to Lee Hunter and his team, as well as the Atlanta Marriott Marquis, for pulling off a terrific event. Never a dull moment in the hotel industry, which is why many of us never leave the sector, with attendees having such varied opinions on how this year may play out.

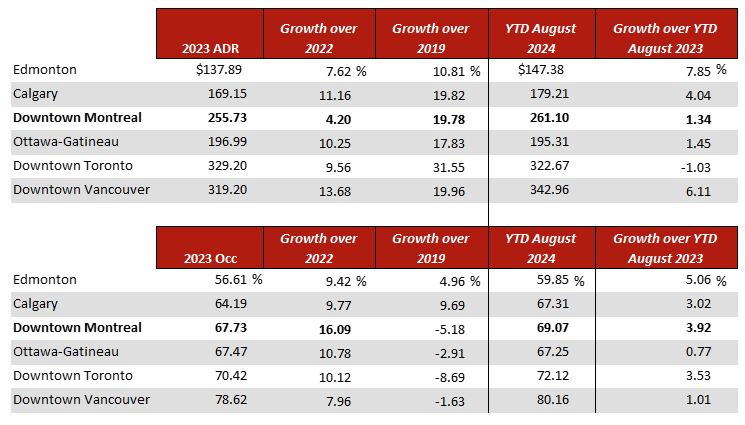

The Industry’s Performance Continues Its Upward Climb

Early 2023 comparisons continue to look favorable, due in large part to the early weeks of 2022 that were negatively affected by the Omicron variant and its effect on travel. Year-over-year comparisons will start to normalize as we extend into April and May, but ADRs are expected to remain notably above last year’s levels due to inflation and the strength of travel overall.

Adam Sacks’ take on the hospitality sector’s defiance of “economic gravity” highlighted the resilience of the service sector in recent years following the pandemic. His highlight of the structural differences between the 2009 recession and the pandemic recession, primarily the financial strength of the household, was an interesting one: the “bailout” on this recession went directly to households, as opposed to bailouts going primarily to financial institutions, like in 2009. Accordingly, the strength of the household is directly benefitting the hospitality sector.

Short-term rental environments are tightening, with many cities and municipalities enacting new zoning codes that restrict their proliferation. This factor, together with residential conversions, may speed the pandemic-related recovery of certain submarkets that are struggling.

Moreover, as the hybrid workweek takes a firm hold on how we accomplish our jobs, the industry is finally experiencing the return of midweek travel (albeit with shorter trips that are primarily on Tuesday and/or Wednesday nights), which has been coupled with strong Thursday-through-Sunday stay patterns. The popularity of work-from-home job structures is settling in, prompting the management of the “super commute” phenomenon, where individuals must travel to visit home offices now for extended periods. Also, other leisure trips remain strong just to escape the now combined work/live environments that so many manage, with little change in scenery in their day-to-day lives. This need to escape the home is benefitting our industry and is likely here to stay for a while.

Despite Top-Line Strength, Transactions Face New Challenges

There was certainly talk of hotel values being down in today’s market, due primarily to financing constraints. However, from a valuation perspective, if someone is under significant and abnormal pressure to sell within a quick timeframe right now (vs. wait for the right deal at the right price), it is more akin to liquidation value and not market value. This is likely the case for assets that are selling today at the highest discounts, compared to late last year’s prices. It will be important for the market to appreciate any strangely low values that emerge during this period as possibly an indication of liquidation value and not necessarily market value. Over the course of 2023, it is likely that more sellers will meet the market in order to get deals done, but not necessarily at that ultra-urgent liquidation point.

The expectation that interest rates may decline later this year is fading, with this dream shifting to mid-to-late 2024. The market is having to recalibrate to a higher debt-cost reality that may be here to stay for a while. Investors are anticipating more deal flow later this year, as loans come due and as owners are unable to refinance given the changes in the lending environment. Buyers are seeing less product on the market today, but the sentiment is that this will change as the year progresses. Accordingly, institutional and private investors are sitting on the sidelines (“patient” money) waiting to acquire these assets.

With all the funds raised from investors, more private equity groups are also entering the lending space this year as an alternative method to earn yield. These groups are offering creative financing options such as bridge loans, mezzanine debt, construction loans, and PIP loans. As deals are becoming more difficult to execute with the traditional lending sources, many are still working their way through, with creative financing becoming the needed lifeline.

The Highlight of Hunter, Sheila Johnson

Certainly the highlight of the conference was the keynote address provided by Sheila Johnson, CEO of Salamander Hotels and Resorts. Her story, both inspiring and frustrating, is a reminder that inclusion in the hospitality field, especially among hotel owners, is not a given, even when approached with all of the appropriate financial backing. She is continuing a much-needed conversation of representation in hospitality leadership, which we here at HVS celebrate. We are happy to announce that our own Chelsey Leffet will be part of the Castell ELEVATE Leadership Training program this spring, and we are sending ten current and future HVS leaders to AHLA’s upcoming ForWard Conference in May.

In Conclusion

Per our clients in attendance, the desire to get deals done and the urge to develop more hotels are as strong as ever, particularly in the extended-stay segment, albeit in a new financing market and high construction-cost reality. Please reach out to any of our leaders across our 35 HVS Americas locations to continue the conversation, and we also hope to see you at upcoming industry events such as the AAHOA Conference, Meet the Money hospitality conference, and ForWard Conference.