Post-Pandemic Hotel Performance in a Shifting Leisure Landscape

As demand for drive-in markets such as Myrtle Beach spiked in 2021 and early 2022, average daily rates (ADRs) within many of these areas rose notably above historic levels. This trend continued through 2022 and 2023, abetted by atypically high inflationary pressure, with vacation-oriented markets across the Southeast sustaining ADRs well above 2019 benchmarks.However, as pandemic-related travel restrictions began to abate, many of these southeastern vacation destinations began to reach a demand and rate ceiling; this moderation was further influenced by consumer uncertainty associated with the 2024 presidential election, which contributed to reduced discretionary travel spending. As demand began to soften, occupancies wavered, followed by slower growth in ADR as 2024 ended. By early 2025, many of the markets throughout the southeast were experiencing a pullback from peak levels of both rate and occupancy; year-end data has corroborated these trends.

Much of this change is attributable to the normalization of leisure demand patterns toward a more typical distribution, with less demand focused on drive-in southeastern destinations. While broader macroeconomic pressures, including elevated interest rates and inflation fatigue, have also exerted downward pressure on leisure demand throughout the United States, the normalization of demand patterns have played an outsized role in these market changes.

Examining the K-Shaped Recovery in Myrtle Beach

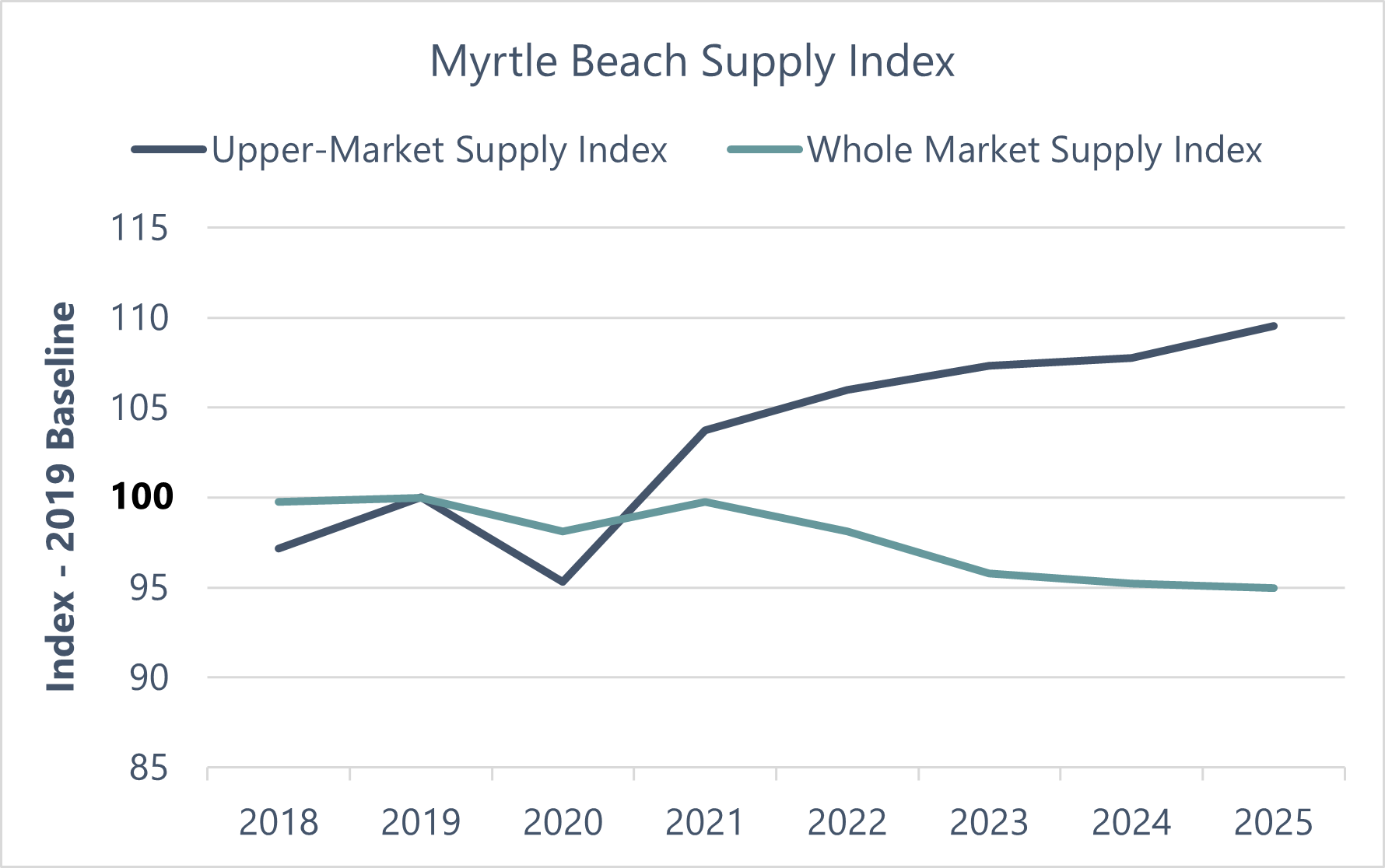

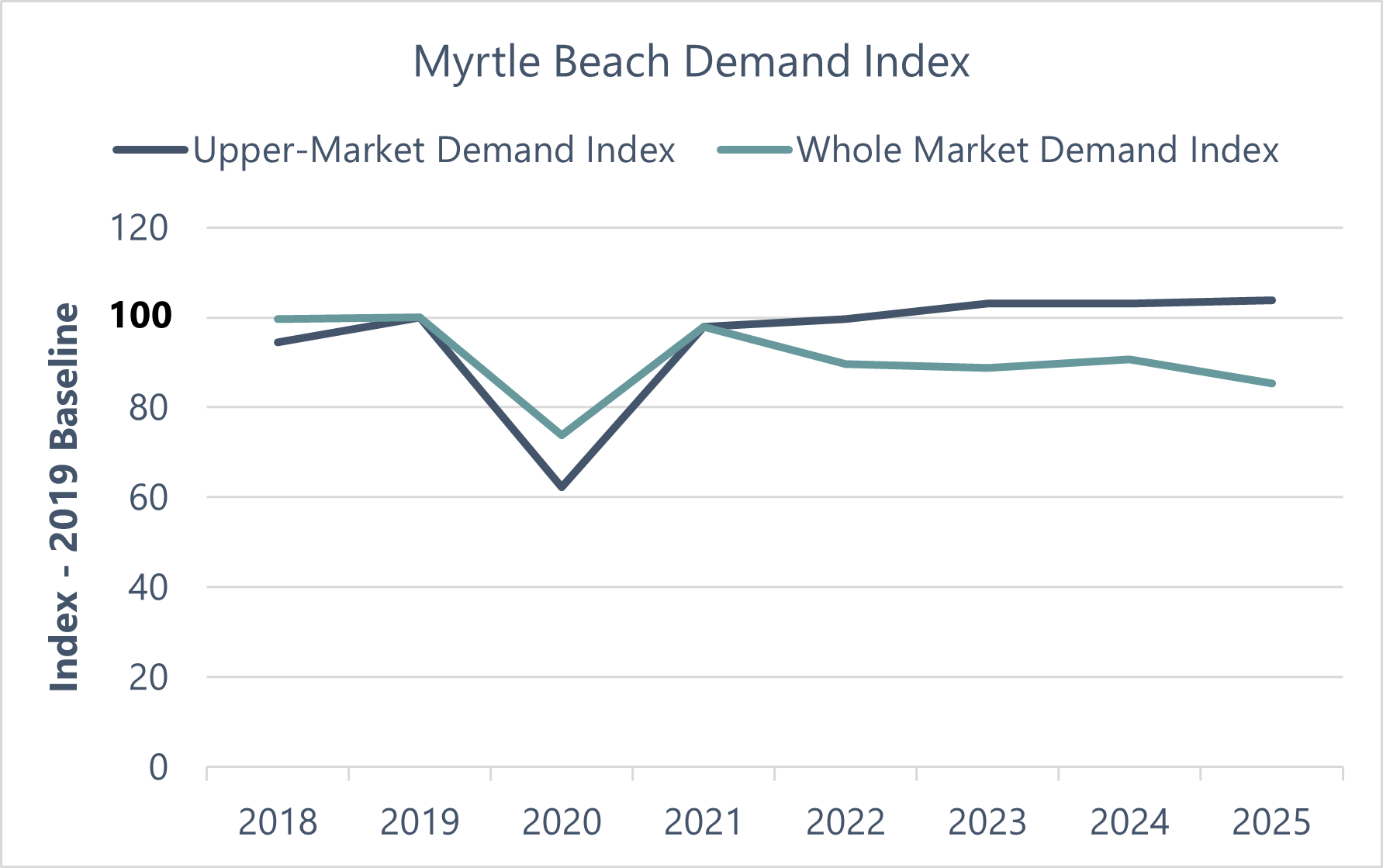

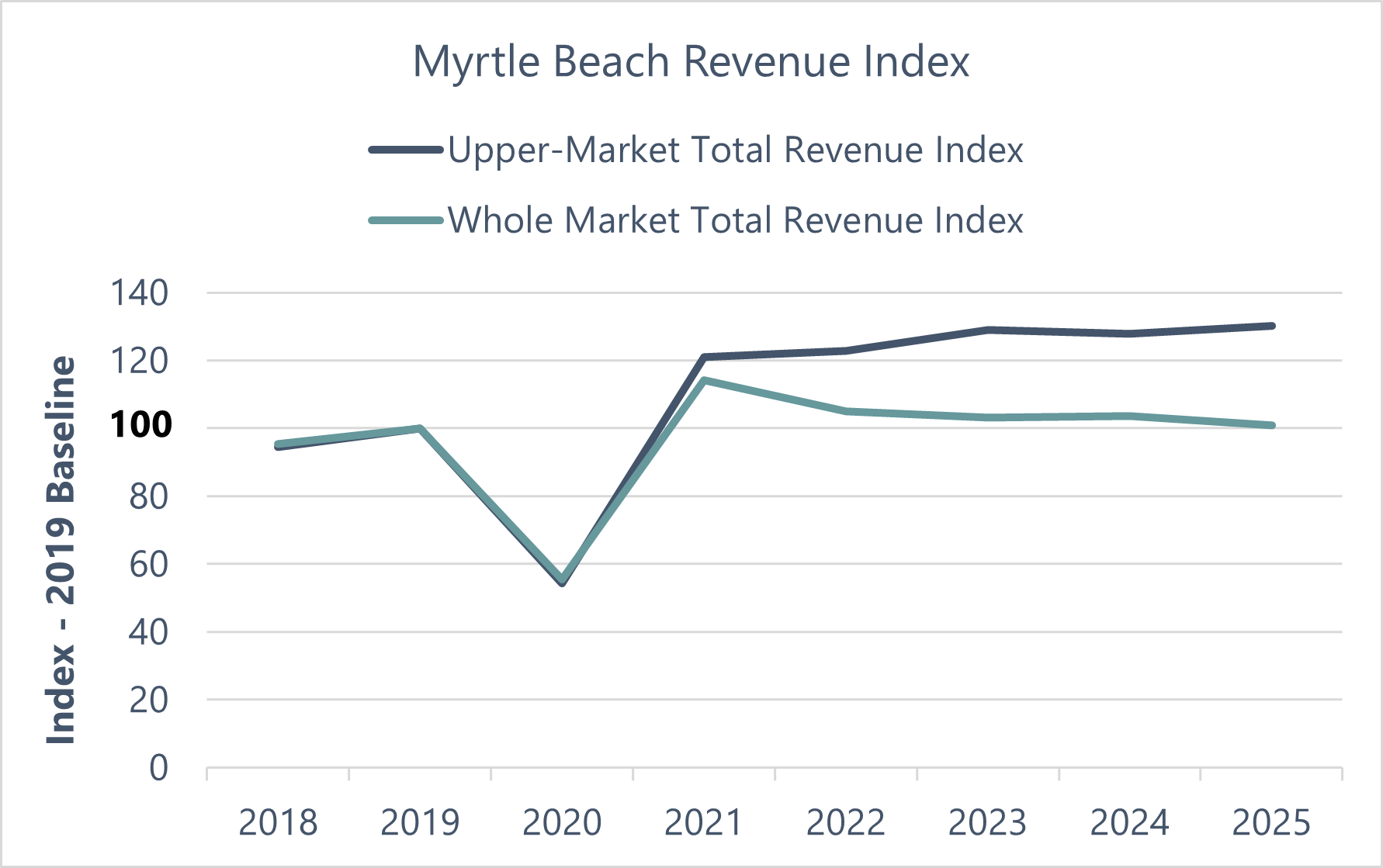

The city of Myrtle Beach is one of the more interesting cases of this pattern in the region. Typically known as a value-driven vacation destination spot, Myrtle Beach’s popularity rose steadily last decade, peaking in 2019 with over 7.5 million occupied room nights, according to data provided by CoStar. Operators in the market were optimistic in 2021 as the market’s ADR surpassed 2019 metrics by 21.3% and revenues peaked at over $1.1 billion. However, the data show that the sharp spike in rate, in addition to the greater demand factors, ultimately had a cooling effect on the market’s overall attractiveness, with demand falling below 6.5 million room nights in 2025. Moreover, rate has yet to eclipse its 2021 peak and continues to normalize, with market revenues for 2025 totaling just over $990 million.However, not all stories in the Myrtle Beach market are of compression and downsizing. The following graphs, where each metric is indexed to 2019, show the supply, demand, and revenue trends that highlight divergence in the market. The contrast between the whole market average and the data for branded hotels in the upper-midscale segment and above (upper market) illustrates a clear K-shaped trend. Although the overall market’s supply, demand, and revenue remain below 2019 levels due to the closure, conversion, or reduced competitiveness of lower-tier and older lodging assets, the upper-market segment has surpassed 2019 across all metrics and has continued to outperform pre-pandemic levels through the first quarter of 2026.

The separation is most pronounced in revenue, as upper-market hotels benefit from higher-quality branded inventory, stronger rate positioning, and sustained investor interest. Conversely, the whole market’s revenue has moderated following the post-pandemic leisure surge. These trends support the characterization of Myrtle Beach’s recovery as K-shaped, with branded upper-market hotels outperforming the broader, value-oriented market.

Supply, Demand, and Revenue Indices Illustrate K-Shaped Recovery for Upper Market vs. Whole Market

Shift Toward Upscale Hotel Development and Brand Conversions

Developers have responded to these shifting market dynamics, and Myrtle Beach’s hotel supply has been increasingly adapted to accommodate travelers willing to spend more on higher-quality experiences. As shown above, the supply index for the upper market has significantly outpaced that of the whole market, reflecting both new construction and the conversion of formerly independent hotels and condominium properties into upscale hotel rooms. In 2023, the Dayton House Resort was aligned with Best Western’s Signature Collection, while half of the DoubleTree Resort was reflagged as The Ellie, part of Hilton’s Tapestry Collection, in June 2024. In early 2025, the long-standing Sea Dip was sold to Drury Hotels for redevelopment under the Drury brand. The Sandcastle Oceanfront Resort at the Pavilion was recently branded as voco The Shelby, IHG’s first voco property in South Carolina. Other hotels in the market are expected to be converted to national brands, though some of these plans remain speculative.Through the concerted efforts of municipal leaders, local developers, and the Myrtle Beach community, as well as the natural beauty of the Grand Strand, the Myrtle Beach hotel market has continued to attract new development and national brand attention at a pace that highlights the destination’s appeal to domestic leisure travelers. Although average hotel performance in the broader market may not inspire investor confidence, the continued upward trend within Myrtle Beach’s upscale hotel segment reflects a sustained belief in the area’s long-term growth potential.

HVS has previously published about the large-scale shift in demand patterns in the hospitality industry; please see the Market Pulse - April 2026 and the 2026 Hunter Hotel Conference Takeaways.

HVS combines rigorous data analysis with local market expertise to deliver insights that move decisions forward. Our unique approach leverages primary, in-market interviews to capture real-time insights straight from local communities. This ensures our conclusions reflect current conditions and evolving trends. To explore the Myrtle Beach market further or discuss investment opportunities tailored to your goals, please contact Brett Testa, your HVS Southeast hospitality expert.