Despite each city within the region having certain characteristics and established performance, decline — brought about by the pandemic and the anticipated changes in supply and demand dynamics — will have a remarkable impact on future hotel performance and profitability.

Here, we will consider 10 key cities for the purpose of presenting performance between 2008 and 2021, in addition to a 2022 forecast.While most markets are likely to have fully recovered by 2024, some cities have been able to achieve stronger recovery in 2021 and will further grow in 2022 on the back of fewer travel restrictions, which will result in an increase in regional and domestic demand.

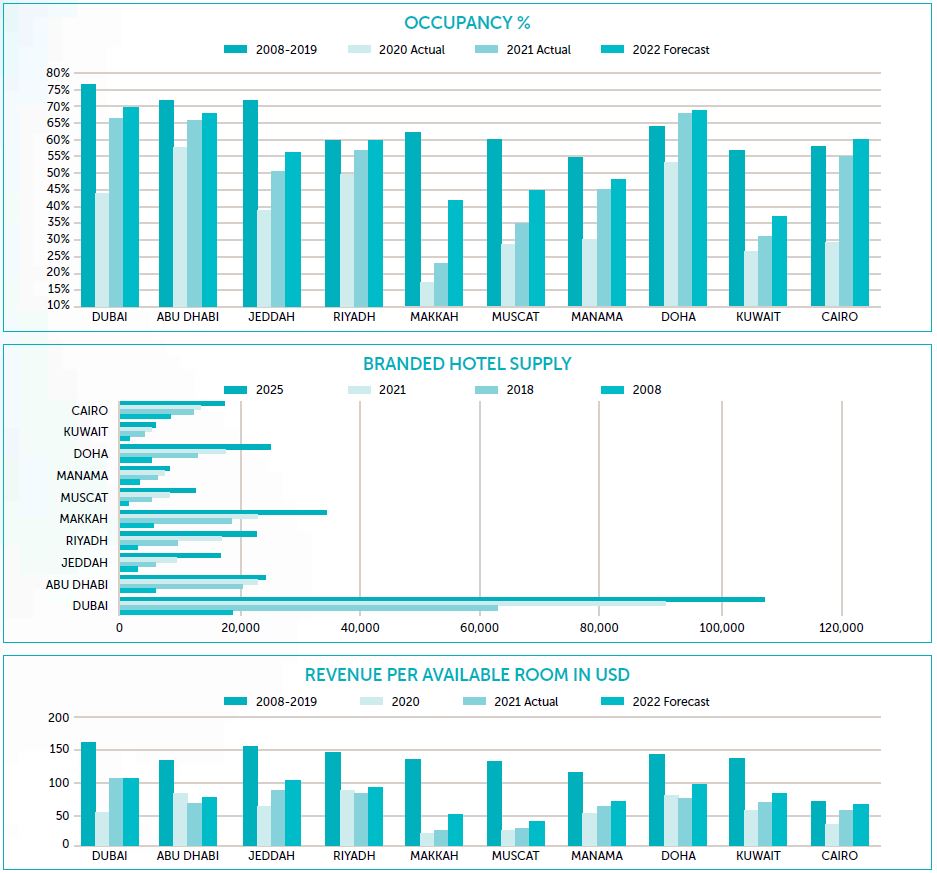

Hotel supply

Branded hotel supply across the 10 cities grew from 57,000 rooms in 2008 to 159,000 in 2018. An additional 56,000 hotel rooms were added between 2019 and 2021. It is estimated that the total number of branded hotel rooms in 2025 will exceed 275,000.In 2021, 42 percent of the branded supply was in Dubai, followed by 11 percent in both Abu Dhabi and Makkah. Of the total branded supply, approximately 75 percent is considered upscale and luxury, with some prominent hotel management companies dominating the markets. With the exception of the UAE, the resort and quality-serviced apartments markets in 2021 remain largely unrepresented across most markets and present a strong opportunity for future hotel developments.

Excluded from the forecast displayed are some 20,000 hotel keys that are planned to be developed by 2030 across several mega developments in the Kingdom of Saudi Arabia.

As primary markets continue to mature and saturate with upscale and luxury brands, secondary markets, notably in Saudi Arabia and the United Arab Emirates, have seen growth in investment opportunities and accommodated demand as a result of robust tourism plans, improved modes of accessibility and infrastructure development. We therefore anticipate a healthy influx of economy and midscale hotels and rise in alternative accommodation, including camping/glamping, wellness resorts, ecolodges and experiential options.

Hotel performance indicators

Key performance indicators for the branded hotel supply across the established markets in the region are presented in the graphs on the opposite page.Average occupancy across the 10 cities was 64 percent between 2008 and 2019, dropping to 38 percent in 2020 and recovering by 12 percentage points to 50 percent by end of 2021. In 2021, Cairo’s market-wide occupancy grew by 88 percent, followed by Dubai, which registered a 51 percent increase.

We forecast additional recovery in a number of markets and expect the average occupancy to be around 56 percent by end of 2022. Market leaders in terms of occupancy in 2022 are expected to be Dubai, Abu Dhabi and Doha, while strong growth is also anticipated in Jeddah, Riyadh and Makkah.

In line with the declining occupancy levels, the average rate in the respective markets fell from USD 208 for the period of 2008- 2019 to USD 145 in 2020. Only a few markets were able to register an average rate growth in 2021: Dubai (+28 percent), Kuwait (+9 percent) and Jeddah (+8 percent). On the other hand, with the exception of Abu Dhabi, Riyadh and Doha, RevPAR increases were witnessed in the remaining seven cities in 2021. The average RevPAR in 2021 was USD 66, which remains significantly lower than the historic average of USD 132 between 2008 and 2019.

It is expected that the entry of new hotels, supported by the ongoing tourism developments and improved travel conditions over the next few years, will allow most cities to fully recover in terms of occupancy and room nights’ demand. However, we anticipate that as the midmarket expands with contemporary yet affordable branded hotel products, the primary and secondary markets will be susceptible to significant average rate pressure which may prevent RevPAR from recovering to historic levels.

Declining RevPAR’s over the last couple of years in the GCC region because of oversupply and changing market dynamics, coupled with increasing operating costs, resulted in significant decline in gross operating profits, which is increasingly becoming the most important key metric in evaluating a brand’s ability to perform and drive value. With the current performance indicators, and as a result of travel restrictions and the softening of demand, the pandemic has provided hotel operators and owners with an opportunity to review some of the industry best practices and cost structures, adopt a more flexible approach to reduce the payroll cost, improve efficiencies and shift the focus from RevPAR to GOPPAR. We take the view that future success will highly depend on assessing revenues per sqm of built-up area in order to optimize performance and ensure long term profitability.

Trends in future developments

The outlook for the hospitality sector remains strong in the region, and once international and regional travel resumes fully, it is anticipated that there will be further increases in overall demand to the region, which currently attracts less than 10 percent of total worldwide tourist arrivals.Equally, travel trends and travelers’ preferences have changed over the last decade, and the emergence of new concepts and alternative accommodation will continue to challenge the current and traditional hotel model. Some of the current development trends are:

• All-inclusive concept in the midscale and upscale segments

• Repositioning and/or repurposing of existing assets

• Investing in and implementation of technology and sustainable solutions/ products

• Re-engineering F&B offerings and turning vacant spaces into revenue-generating streams

• Branding versus deflagging

• Boutique hotels with character

• Eco-friendly hotels/resorts

hospitalitynewsmag.com retains the copyrights of this article. Article cannot be republished without prior written consent by hospitalitynewsmag.com

View Article on https://www.hospitalitynewsmag.com/the-region-in-numbers/

HVS Dubai has been featured in the prestigious Hospitality News Middle East magazine, leader in its field. This prominent publication has highlighted our expert opinion on the matter of the Middle East hotel market. Hospitality News Middle East is the go-to source for the latest news, developments and trends in the region’s hospitality and foodservice industries. www.hospitalitynewsmag.com, features essential market insights, analysis and guidance from experts in the field, in addition to special reports on the latest concepts and interviews with top international names in the sector.

Widely regarded as a must read, the magazine has built a solid reputation as a reference for hospitality professionals in the Middle East and beyond. Daily news bulletins can be found online.