The 2026 U.S.-Iran conflict triggered one of the most severe non-pandemic disruptions to the GCC hospitality sector. The shock was defined not only by its magnitude but by the speed at which aviation, demand, and traveler confidence deteriorated simultaneously. While aviation capacity began to recover following the April ceasefire, hotel demand has lagged, highlighting the central role of confidence in recovery dynamics.

Why It Matters for Gulf Tourism

The GCC hospitality sector is structurally dependent on aviation connectivity, international demand, and corporate mobility. The conflict disrupted all three simultaneously during peak trading months, amplifying its economic impact.The escalation of the 2026 U.S.-Iran conflict triggered one of the sharpest non-pandemic disruptions to Gulf tourism in recent years. Within days, the region’s core transit corridor, linking Dubai, Doha, and Abu Dhabi and carrying roughly 40 million passengers annually between Europe and Asia, was severely disrupted. For both the UAE and Saudi Arabia, where tourism and hospitality underpin economic diversification strategies, the timing significantly amplified the impact.

Tourism contributes approximately 11% of GCC GDP, with the UAE and Saudi Arabia among the most aviation-dependent markets in the region. This reliance made them particularly vulnerable to airspace closures, in contrast to markets such as Qatar and Bahrain, where land-based arrivals account for a larger share of demand. Across the Middle East, tourism generates around $367 billion annually, and early estimates suggest the conflict could reduce international arrivals by 23 to 38 million in 2026, equating to a loss of $34-56 billion in visitor spending.

Crucially, the impact stems less from physical disruption and more from the breakdown of the systems that sustain hospitality demand: air connectivity, traveller confidence, corporate mobility, and event activity. This effect is magnified by timing: March to May represents one of the region’s highest-yield periods. Any shock to travel sentiment during this window carries a disproportionate impact, as lost peak-season demand is difficult to recover later in the year.

Aviation & Accessibility

Aviation acted as the primary transmission channel of the crisis, and both the speed and scale of disruption were unprecedented. According to Cirium, capacity across the Middle East fell by approximately 55-60% versus scheduled levels at the peak of disruption, compared to a low single-digit contraction globally over the same period. This divergence highlights how geographically concentrated the shock was, despite limited direct impact on the wider global aviation system.The EASA conflict-zone advisory and subsequent airspace closures sharply reduced activity across the Gulf’s main hub airports: Dubai International Airport (DXB), Zayed International Airport (AUH), and Hamad International Airport (DOH). Flight tracking data from Cirium and FlightAware indicates that, in the first weeks of the conflict, GCC based airlines experienced a decline of roughly 50% in flights and available seat capacity, with some hubs facing near total operational shutdowns for short periods.

This disruption is amplified by the Gulf’s structural role within global aviation networks. Industry estimates from organisations such as International Air Transport Association (IATA) suggest that Middle Eastern carriers account for a significant share of long-haul transit traffic, particularly on Europe-Asia and Europe-Africa corridors. More broadly, hub airports in the region facilitate approximately 10-15% of global international transit flows, acting as critical connectors between major long-haul markets.

Figure 1 — Annual Capacity Flown vs Schedule (March 2026)

/Screenshot%202026-05-05%20105844.png)

Figure 2 — Airport Flight Movements (March-April 2026)

/Screenshot%202026-05-04%20201755.png)

Source: FlightAware

Taken together, Figures 1 and 2 highlight several defining dynamics of the aviation impact. The data shows an extreme regional concentration of disruption, with the Middle East standing out as a clear outlier. Aviation capacity declined at a level roughly twenty times deeper than the global average, with no other region experiencing a comparable gap between planned and actual capacity. This confirms that the shock was not a broad-based global downturn, but a targeted breakdown of one of the world’s most critical transit corridors.This pattern underscores the structural dependence on Gulf airspace within global aviation networks. While international traffic flows remained largely intact, they were increasingly re-routed rather than replaced, effectively bypassing the Gulf’s hub system. For the GCC, this had direct implications for stopover traffic, airline connectivity, and downstream hotel demand.

The disruption was not only highly concentrated, but also exceptionally rapid. In several cases, most notably in Doha, aviation activity fell to near-zero levels within days, leaving no time for demand to adjust and amplifying the immediate impact on hospitality markets.

At the same time, the recovery pattern has been uneven and decoupled from demand. Although flight movements began to recover from April onwards, this operational rebound has not translated directly into a recovery in hotel performance. Demand, particularly from long-haul international markets, continues to be driven by traveller confidence, booking behaviour, and perceptions of regional stability.

Structural differences across markets have further shaped outcomes. The UAE, with its high exposure to international transit and global travel flows, experienced a sharper initial shock but has shown a faster operational recovery as connectivity improves. In contrast, Saudi Arabia, supported by a stronger domestic base and more stable religious demand, has exhibited lower volatility and more consistent performance throughout the disruption.

Finally, recovery is being influenced not only by regional conditions, but also by broader global dynamics. Rising fuel costs and capacity adjustments by international airlines have introduced an additional constraint, meaning that GCC markets are recovering within a weakened global aviation environment, rather than a fully restored one. This adds complexity to the recovery path and reinforces the importance of both regional stability and global aviation conditions in shaping the outlook for hospitality demand.

Demand Segments

Pre-Conflict Market Positioning: Strength with Structural DifferencesThe GCC entered 2026 from a position of strong tourism momentum, with most markets benefiting from sustained post-pandemic recovery, rising international demand, and increased government investment in the sector. However, beneath this shared growth trajectory, there were important structural differences in demand composition that would shape how each market responded to the crisis.

United Arab Emirates: High Growth, High Exposure

The UAE entered 2026 at a cyclical peak. The country recorded approximately 32.3 million hotel guests in 2025, with tourism contributing around AED 257 billion (13% of GDP), supported by strong international visitor spending of approximately AED 228 billion. This performance is structurally underpinned by three major demand segments: International arrivals, transit passengers, and corporate and MICE demand.

This elevated level of global integration makes the UAE one of the most aviation-dependent hospitality markets globally, and therefore particularly vulnerable to disruptions in air connectivity and traveller confidence.

Saudi Arabia: Strong Momentum with a More Stable Demand Base

Saudi Arabia also entered 2026 with rapid growth momentum. Total tourist trips reached 115.9 million, with inbound spending exceeding SAR 168 billion, supported by continued progress toward Vision 2030 targets. Unlike the UAE, Saudi Arabia’s demand structure is more diversified and largely driven by a large domestic travel base, religious tourism in Makkah and Madinah and lower reliance on transit flows.

This results in a more stable baseline of demand, particularly during periods of regional uncertainty, even as international, corporate, and event-driven segments remain exposed.

Other GCC Markets: Positive Momentum, Smaller Scale

Across the wider GCC, tourism activity was also expanding ahead of the conflict.

- Qatar welcomed 5.1 million visitors in 2025, continuing post-World Cup momentum.

- Bahrain recorded 15 million visitors, supported by regional travel.

- Oman saw international arrivals recover to 3.9 million, above pre-pandemic levels.

- Kuwait handled 14.9 million passengers, with tourism contributing 7% of GDP.

Demand Dynamics

Demand weakened sharply in the immediate aftermath of the conflict. Within 48 hours of the initial strikes, hotel booking cancellations across Dubai were running at 60%, and occupancy fell from an average of 84.8% in the first two months of 2026 to 22.8% in the week ending 14 March. The World Travel & Tourism Council estimated that the Middle East region was losing USD 600 million per day in visitor spending. This translates to roughly USD 180 million attributable to the UAE and USD 120 million to Saudi Arabia daily.The broader outlook weakened notably. Tourism Economics projected that inbound arrivals to the Middle East could fall between 11% and 27% year-on-year in 2026, against a pre-conflict forecast of 13% growth. In real terms, that means 23-38 million fewer international visitors and a USD 34-56 billion loss in visitor spending, including the lingering drop in confidence expected even after the immediate conflict period ends.

This pattern of travelers reacting to headlines and perceived risk before destination fundamentals have time to adjust is a familiar feature of tourism during geopolitical crises. Reuters reported that vacation rental cancellations in the UAE more than doubled after the initial strikes, reaching around 8,450 units, mostly for March stays. Airlines reported a clear change in booking patterns, with travelers choosing destinations outside the Middle East and shifting more towards leisure spots in the Mediterranean.

For hotel operators, this created pressure from two directions at once: falling revenues in the more exposed markets alongside rising operating costs across both. UAE hotels face a sharper revenue risk given their dependence on international visitors and business travel. Saudi Arabia has more protection on the demand side, but it is not immune to wider economic effects. Reuters reported that Saudi Arabia's non-oil private sector contracted in March for the first time since August 2020, as supply chains were disrupted by the conflict, a warning sign for business activity and investor confidence.

Performance Impact

Hotel performance across the GCC in 2026 will be shaped not only by occupancy levels, but also by the scale, depth, and demand composition of each hotel market. As established in the preceding sections, the aviation shock translated into a rapid demand contraction; however, the extent to which this impacted hotel performance has varied significantly across markets as observed specifically during the months of April and May.Therefore, this section first looks at market scale through current room supply and expected occupied room nights, then reviews actual January-April 2026 trading performance and finally places the 2026 outlook in a wider historical context.

Although RevPAR remains a useful indicator, occupancy is used here as the main measure of hotel demand, given its direct relationship with travel flows and booking behaviour.

Dubai stands apart from the rest of the region in supply terms, with 153,053 branded and quality keys, approximately 2.3 times larger than the next largest market, Makkah (65,717 keys). This scale is reflected directly in demand, with Dubai forecasted to generate in 2026 approximately 32 million occupied room nights , more than double that of Makkah at approximately 15 million room nights.

Figure 3 — GCC Hotel Supply by Market (Keys, February 2026)

/Screenshot%202026-05-05%20110106.png)

Source: STR

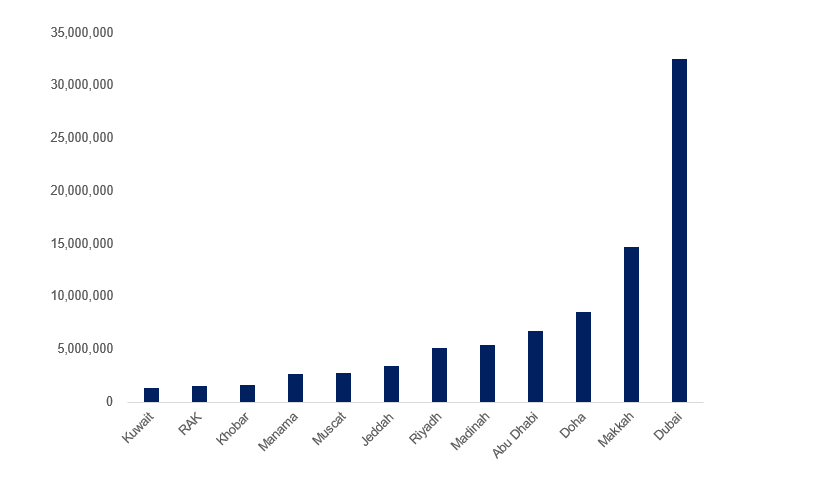

Figure 4 — Forecasted Annual Occupied Room Nights by Market (2026)

The chart highlights a highly concentrated demand structure across GCC hotel markets, with Dubai clearly dominating regional performance. At approximately 32 million projected occupied room nights in 2026, Dubai is predicted to generate more than double the forecasted demand of the next largest market, Makkah (~15 million), and significantly exceeds all other cities. A second tier of markets, including Doha, Abu Dhabi, Madinah, and Riyadh, are expected to operate at a materially smaller scale, each generating between roughly 5 and 9 million room nights. Beyond this, the remainder of the region consists of smaller, more fragmented markets with comparatively limited demand bases.

This distribution has important implications for how performance is interpreted. The concentration of demand in a small number of large, internationally exposed markets means that any disruption to aviation and global travel flows has a disproportionately significant impact on overall regional performance. At the same time, the presence of Makkah and Madinah among the largest markets reflects the stabilising role of religious demand, which is less discretionary and more resilient during periods of disruption. As a result, both market scale and demand composition are critical in explaining the divergence in forecasted performance across the GCC in 2026.

Figure 5 illustrates how hotel performance evolved during the first four months of 2026, capturing both the pre-conflict peak period and the immediate impact of the aviation-led demand shock.

/Screenshot%202026-05-04%20201811.png)

In January and February, most markets recorded strong occupancy levels, reflecting peak-season demand and robust international travel flows. However, following the escalation of the conflict in early March, a clear divergence emerged across markets.

Internationally exposed markets, particularly Dubai, Abu Dhabi, and Doha, experienced a sharp and immediate decline in occupancy, reflecting their reliance on international arrivals, transit traffic, and corporate and MICE demand.

While some recovery was observed from late March into April, occupancy levels in these markets remained well below pre-conflict levels, indicating that demand recovery has lagged the partial restoration of flight activity.

In contrast, holy city markets such as Makkah and Madinah remained the strongest performers throughout the period, demonstrating relative resilience. This stability is primarily supported by religious tourism, which is less discretionary and less sensitive to short-term geopolitical developments. Jeddah also held up better than most other markets, benefiting from a mix of domestic, regional, and religious demand.

Elsewhere, Riyadh, Khobar and Muscat recorded a more moderate softening, reflecting exposure to corporate and business travel segments, while Kuwait and Manama remained among the weakest performers throughout the period, reflecting both smaller market scale and greater sensitivity to regional sentiment.

Overall, Figure 5 reinforces a key pattern established earlier in the report: Markets supported by domestic and religious demand were better able to absorb the initial shock, while those dependent on international and transit-led travel experienced sharper and more immediate declines.

Figures 6 and 7 place the 2026 outlook within a broader historical and comparative context, highlighting both the magnitude of the current disruption and the variation in impact across markets.

Following the pandemic-driven collapse in 2020, most GCC markets experienced a strong recovery, with occupancy levels in 2024 and 2025 reaching or exceeding pre-pandemic benchmarks in several cases. Against this backdrop, the projected decline in 2026 represents a clear reversal of recent growth, driven by geopolitical disruption rather than underlying structural weakness.

However, the data also indicates that the 2026 downturn, while significant, is not as deep as the pandemic shock in most markets. This suggests that the current disruption is severe but temporary, assuming no further escalation.

Figure 6 — GCC Occupancy by Market: 2020, 2024, 2025 and 2026F

/Screenshot%202026-05-04%20201834.png)

Figure 7 further highlights the uneven distribution of forecast performance across markets.

- The sharpest declines are expected in internationally exposed markets, particularly Dubai, Abu Dhabi, and Ras Al Khaimah, reflecting their dependence on international travel, aviation connectivity, and global business activity.

- Makkah and Madinah are expected to remain closest to prior-year performance levels, supported by stable religious demand.

- Markets such as Doha, Muscat, and Manama are also expected to record weaker performance, reflecting softer travel demand and greater sensitivity to regional sentiment.

Together, these figures reinforce a central conclusion: The 2026 outlook is not a uniform downturn, but a structural divergence between market types.

Figure 7 — GCC Markets: Hotel Occupancy Comparison, 2025 vs 2026F

/Screenshot%202026-05-04%20201846.png)

Source: STR / CoStar Group; HVS Forecast

Outlook

The announcement of a two-week U.S.-Iran ceasefire on 8 April 2026 has improved the near-term outlook, although recovery across GCC hospitality markets is expected to be gradual and uneven. Major regional airlines, including Emirates, Etihad Airways, and Saudia, have begun rebuilding schedules, albeit cautiously. Flights across the UAE, Qatar, and Saudi Arabia continue to operate through controlled corridors, with partial restrictions still in place. While the immediate operational shock is beginning to ease, conditions remain well short of normalised travel flows.In the near term, hotel performance is expected to be supported primarily by domestic and regional demand, with staycation offers and targeted promotions helping to offset weaker international volumes through the middle of the year. International arrivals are likely to recover more gradually, with a more meaningful rebound expected only toward year-end, as airspace conditions stabilise and traveller confidence improves. This reflects a pattern observed throughout the report: connectivity can return relatively quickly, but demand recovery is ultimately driven by confidence.

UAE Outlook

Dubai and Abu Dhabi, as the most internationally exposed markets, are likely to see a slower and more uneven recovery. While the UAE benefits from strong fundamentals, including a diversified hotel base, global brand, and government support, recovery will depend on the return of international and long-haul demand, which is expected to lag improvements in flight capacity.

KSA Outlook

Saudi Arabia appears better positioned in the near term, supported by domestic demand and stable religious tourism in Makkah and Madinah. Vision 2030 projects continue to underpin long-term growth, although prolonged instability could weigh on costs, business sentiment, and project delivery.

Outlook Assumptions and Risks

The outlook presented assumes that the conflict remains contained, that airspace restrictions continue to ease, and that traveller confidence gradually improves over the coming months. It also assumes no major new travel bans, border closures, or large-scale event cancellations during the remainder of 2026.

Under these conditions, recovery is expected to be gradual and uneven, with international demand returning more slowly than domestic travel.

However, several downside risks remain. Higher operating costs, particularly driven by elevated fuel prices, alongside broader oil price volatility, could constrain airline capacity and travel demand. In addition, any renewed escalation in regional tensions or prolonged uncertainty would delay recovery further, particularly in internationally exposed markets.

Authors Note: “The key question is how long the effects persist. The trajectory of recovery will depend on whether the disruption remains a short-term operational shock or evolves into a more prolonged confidence-driven slowdown affecting travel behaviour, investment decisions, and market sentiment. The 2026 disruption has reinforced a defining characteristic of GCC hospitality markets: connectivity drives demand, but confidence determines recovery”.

Disclaimer

HVS forecast of occupancy is based on a set of assumptions and information available to us at the time of forecast. HVS forecast should be viewed as indicative only and not relied upon for future course of action. These forecasts may be subject to change, and therefore HVS has no obligation to update these forecasts and makes no representation or warranty and expressly disclaims any liability with respect thereto.