Key Highlights in 2025

Singapore, a city-state spanning 734 square kilometres with a population of approximately 6.04 million, remains one of the world’s top travel and business destinations. Its modern infrastructure, cultural diversity, and strategic location continue to attract millions of visitors annually.

In 2025, Singapore’s tourism sector continued to demonstrate resilience, with international visitor arrivals increasing by 2.3% year-on-year. Passenger traffic grew by 3.4%, surpassing pre-pandemic 2019 levels for the first time since the COVID-19 outbreak. While overall hospitality performance moderated slightly, with a 0.7% marginal decline in revenue per available room (RevPAR), hotel investment activity remained robust, with total transaction volume exceeding SGD1.2 billion.

Source: Unsplash

Tourism demand in 2025 was supported by several key developments. New attractions, including the Mandai Wildlife Reserve and the Singapore Oceanarium at Resorts World Sentosa, opened during the year, while existing attractions introduced enhancements such as Jurassic World: The Experience at Gardens by the Bay’s Cloud Forest. Singapore also hosted several high-profile events, including the World Aquatics Championships 2025, the first time the event was held in Southeast Asia, alongside the POP TOY SHOW 2025, regionally exclusive concerts, and recurring events such as the Formula 1 Singapore Grand Prix. These initiatives, together with a growing focus on attracting higher-spending visitors, reflect a strategic shift towards a lower-volume, higher-value tourism model.

Looking ahead to 2026, Singapore’s tourism sector is expected to maintain its upward trajectory, supported by continued investment in attractions and hospitality infrastructure, ongoing rejuvenation efforts, and a strong pipeline of major international events, alongside further emphasis on higher-value tourism segments.

.png)

Source: HVS Research

Economic Outlook

In 2025, Singapore’s economy recorded solid growth, with GDP expanding by 5.0%, slowing slightly from 5.3% in 2024. Growth was held up by global demand, particularly for semiconductor and electronic exports, alongside resilient domestic consumption. The fiscal position improved, with the budget balance reaching a surplus of 0.5%, following a turnaround in 2024 after several years of deficits.

Looking ahead, GDP growth is projected to moderate to 3.2% in 2026 before stabilising at around 2.2% to 2.3% annually over the longer term. Lending interest rates, which peaked at 3.6% in 2023, have declined and are expected to remain below 2.0% through 2030. Supported by continued investments in infrastructure and sustainability initiatives, Singapore’s diversified economy is expected to remain resilient despite ongoing external uncertainties.

Figure 1: Economic Outlook

Source: EIU Country Report March 2026 * EIU Estimates

Economic Performance & Outlook

Singapore’s GDP is projected to grow by 3.2% in 2026, supported by sustained global demand for semiconductors and electronic products. The moderation from the 5.0% growth recorded in 2025 reflects increasing uncertainties surrounding global trade, particularly tariff-related tensions that may weigh on exports and investment flows. The potential impact of US-driven trade shocks could also dampen domestic demand through softer foreign direct investment inflows and a more cautious labour market outlook. Over the longer term, the services sector is expected to remain the primary driver of economic growth, supported by resilient domestic consumption and Singapore’s continued role as a regional hub for finance, trade, and business services.

Currency Exchange Outlook

Singapore has historically maintained a relatively stable exchange rate under the Monetary Authority of Singapore’s (MAS) exchange-rate based policy framework. Amid rising global uncertainties, the Singapore dollar is increasingly viewed as a regional safe-haven currency. As a result, the currency is projected to appreciate modestly against the US dollar in the near term, averaging around SGD1.24 per USD1.

Inflation

EIU reported that Singapore’s inflation rate moderated significantly in 2025, declining to approximately 0.9%, supported by government measures aimed at easing cost-of-living pressures, including targeted fiscal transfers and subsidies. Looking ahead, inflation is expected to normalise gradually, with MAS anticipated to maintain price stability and manage inflation at just under 2.0% over the medium term through a combination of its exchange-rate based monetary policy framework. This outlook is supported by continued cost management measures, including price controls on essential goods, amid external pressures such as elevated energy costs linked to ongoing geopolitical tensions.

Interest Rates

As of 31 March 2026, the 3-month SORA rate stands at 1.07%, while the 1-month rate is 1.03%, reflecting a low interest rate environment. In the United States, the Federal Reserve has maintained policy rates at 3.5% to 3.75%, the highest in over a decade, in response to persistent inflationary pressures, driven by rising energy costs linked to the ongoing war in Iran. Against this backdrop, Singapore’s interest rates are expected to ease gradually, with the EIU forecasting lending rates to decline from 1.8% in 2025 to 1.4% in 2026. This is supported by a more accommodative rate environment.

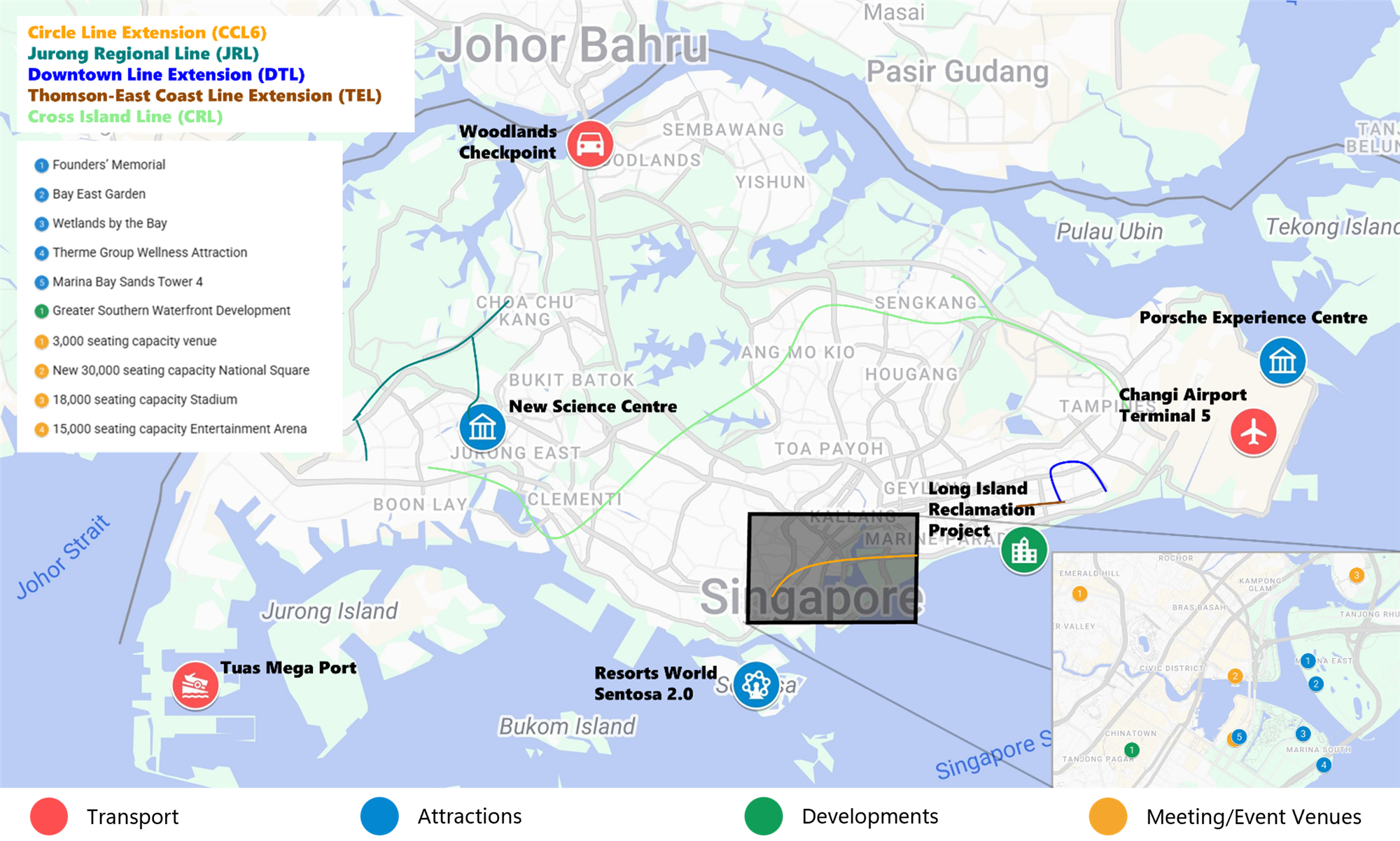

Infrastructure Developments

2026

- Live Nation’s first purpose-built venue in Asia with 3,000 seating capacity to be completed

- TEL Bedok South and Sungei Bedok to open

- DTL Xilin and Sungei Bedok to open in 2H2026

- 4-km CCL6 will close the loop by adding three stations (Keppel, Cantonment and Prince Edward Road), connecting Harbourfront to Marina Bay station

2027

- Bay East Garden to open

- New Science Centre Singapore to open

- New National Square, an amphitheatre with 30,000 seats built at site of former Float @ Marina Bay to be completed

- 21.5-km North-South Corridor connecting northern region to CBD will be completed in phases

- First Regional Porsche Experience Centre to open

- JRL (West) Phase 1 comprises ten stations linking Choa Chu Kang to Boon Lay and Tawas

2028

- JRL Phase 2 to be completed

- Founders’ Memorial to open

- First phase of Woodlands Checkpoint expansion targeted to be completed

- Progressive opening of Wetlands by the Bay to commence

2029

- JRL to be fully completed

2030

- Resorts World Sentosa 2.0 expansion project

- 12-km Greater Southern Waterfront development

- Therme Group’s 4-hectare Wellness Attraction

- Long Island Reclamation project

- 18,000 seat arena replacing Singapore Indoor Stadium

- CRL Phase 1 to be completed

Beyond 2031

- Marina Bay Sands 4th tower expansion project including 15,000-seat entertainment arena to be completed (2031)

- CRL to be completed (2032)

- DTL extension (2035)

- Completion of Changi Airport T5 (2030s – 2040s)

- Tuas Mega Port (2040)

Singapore Tourism Landscape

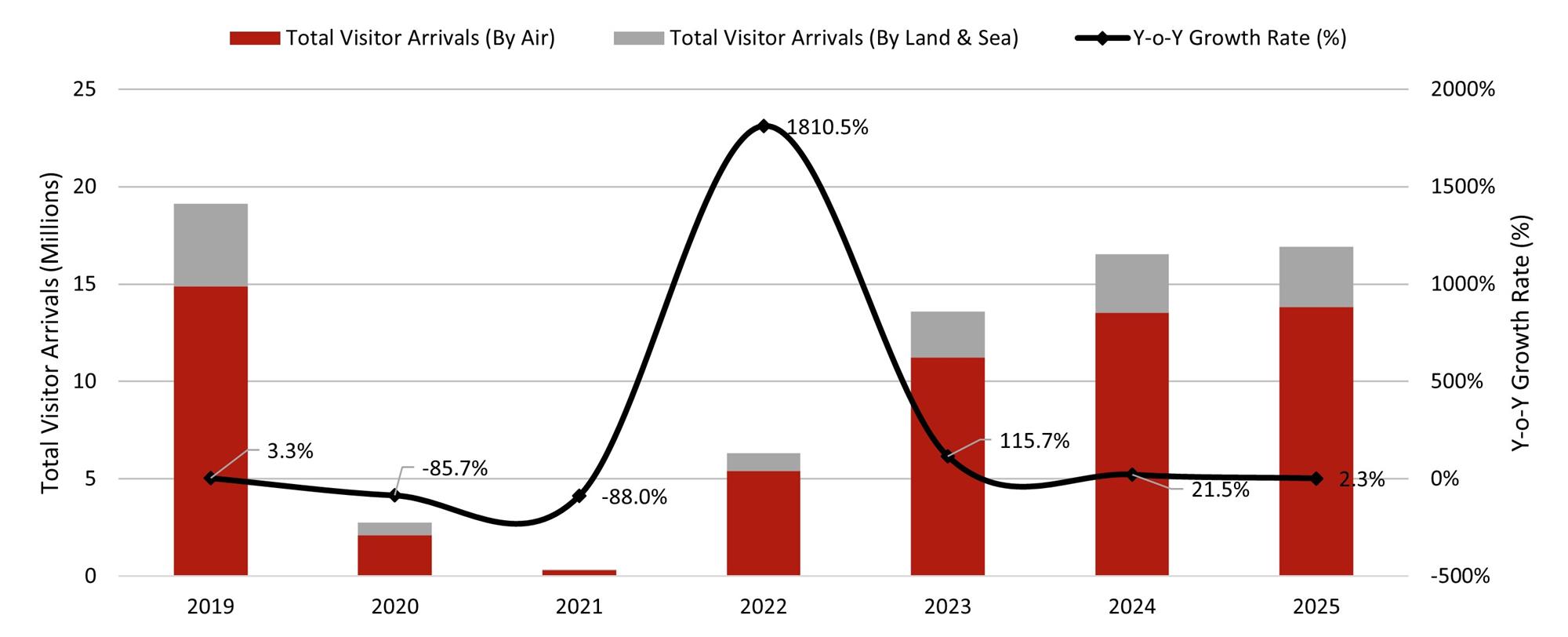

Overnight Visitors

Singapore’s overnight visitor arrivals experienced very minimal growth year-on-year, with an increase of only 538 visitors. The 12.4 million overnight visitors in 2025 amount to around 85.4% of 2019’s numbers.

FIGURE 4: Overnight Visitors to Singapore (2019 - 2025)

.jpg)

Source: STB

Tourism Receipts

Total visitor spending from January to September 2025 reached SGD23.88 billion, reflecting a 6.6% increase from the same period in 2024. Compared to 2019, we observe a shift in spending behaviour, with higher per capita spending overall, and visitors spending proportionately more on experiences and services rather than shopping and accommodation.

FIGURE 5: Visitor Spending by Category (Jan-Sep 2024 vs Jan-Sep 2025)

.jpg)

*SEG – Sightseeing, Entertainment & Gaming Source: STB

International Source Market

In 2025, Singapore’s top five source markets remained consistent with 2024, albeit with minor shifts in ranking. China retained its position as the largest source market, recording marginal growth of 0.6% (approximately +18,000 visitors). Indonesia remained the second-largest market, though it was the only top-five market to register a decline, with arrivals decreasing by 2.0%, likely due to the depreciation of the Indonesian rupiah against the Singapore dollar and softer domestic economic conditions. Malaysia moved up one position, posting strong growth of 7.6% year-on-year, supported by the appreciation of the Malaysian ringgit. Australia also rose in ranking, with arrivals increasing by 8.0%, driven in part by improved flight connectivity and greater travel affordability. India recorded modest growth of 0.8%, supported by repeat visitation, particularly from families, amid ongoing enhancements to Singapore’s tourism offerings.

FIGURE 6: Top Source Markets (2025)

.jpg)

Source: STB

Visitor Spending

In 2024, the source markets with the highest tourism receipts were:

- China – SGD4.58 billion

- Indonesia – SGD2.89 billion

- Australia – SGD2.00 billion

In 2024, the source markets with the highest per capita expenditure were:

- USA – SGD2,166

- Australia – SGD1,702

- Japan – SGD1,657

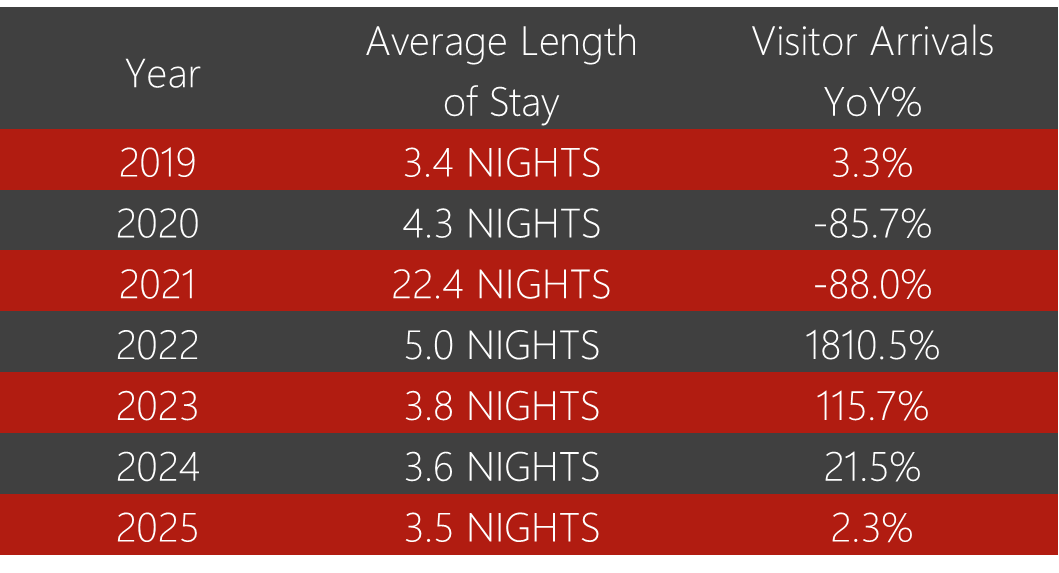

Average Length of Stay

The Average Length of Stay (ALOS) in 2025 is 3.5 nights, a slight decrease from 3.6 nights in 2024. This reduction could be due to higher travel costs in Singapore and shorter business trips due to the adoption of virtual meetings. However, it is noteworthy that the 2025 ALOS is still higher than 2019’s average of 3.4 nights. This suggests a trend towards longer stays compared to the pre-pandemic period. As travel patterns stabilise, we anticipate that the ALOS will return to normal levels.

FIGURE 7: Average Length of Stay and Visitor Arrivals Growth (2019 – 2025)

Purpose of Visit

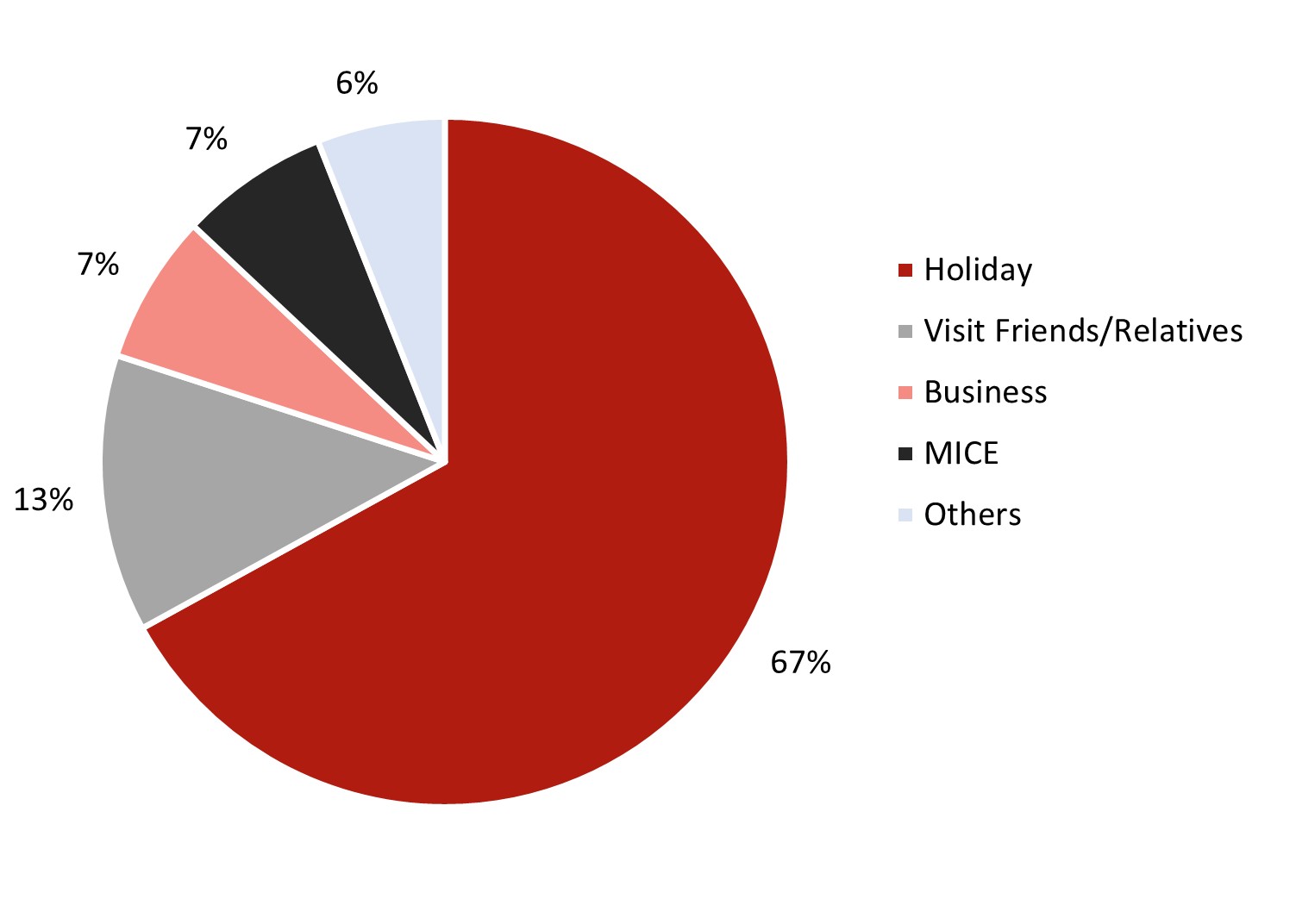

Singapore's year-round tropical weather supports a diverse range of tourism offerings. In 2024, the majority of international travellers visit Singapore for holiday purposes, accounting for 67% of visitors. This is followed by visits to friends and relatives (13%). Notably, 60% of the total travellers in 2024 are repeat visitors to the island state, highlighting its enduring appeal. Singapore's cultural richness, vibrant food scene, and world-class attractions contribute significantly to its popularity among tourists.

FIGURE 8: Purpose of Visit (2024)

Source: STB

*Latest data available till 2024

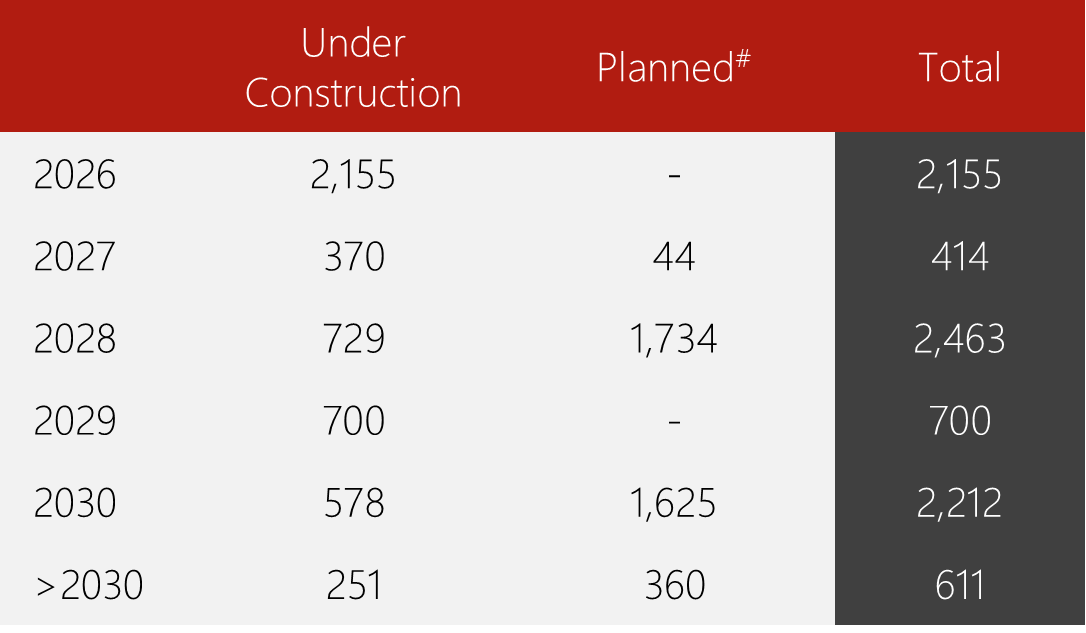

Singapore Hotel Pipeline

2025 was a quiet year for Singapore’s hotel supply growth. The room supply only grew by 0.7%. HVS notes the opening of Mandai Rainforest Resort by Banyan Tree (338-keys), Mama Shelter Singapore Orchard (115-keys), and Raffles Sentosa Singapore (62-keys).

As of April 2026, HVS tracks a total of 79,566 keys on the market. By 2030, an additional 6,768 rooms are expected to be added to Singapore’s accommodation supply, representing 8.5% of the existing supply. Out of the 6,768 rooms, 40.4% or 2,731 rooms are branded, with the majority of them in the upscale segment. In 2026, a total of seven branded properties are expected to enter the market: two have opened, and five are upcoming.

Hotel Openings (Branded)

2026:

- Hotel Waterloo Singapore - Handwritten Collection, 502-key (opened)

- Varel Singapore, a Tribute Portfolio Hotel, 128-key (opened)

- Movenpick Living Singapore, 40-key

- Movenpick Singapore, 808-key

- Somerset Clarke Quay Singapore, 192-key

- NoMad Hilton Singapore, 173-key

- lyf Chinatown, 90-key

2027:

- Avani Singapore, 200-key

- Moxy Singapore Clarke Quay, 475-key

Beyond 2027:

- Aman Singapore, 11-key

- Hotel Indigo Changi Airport Terminal 2, 255-key

- W Singapore Marina View, 350-key

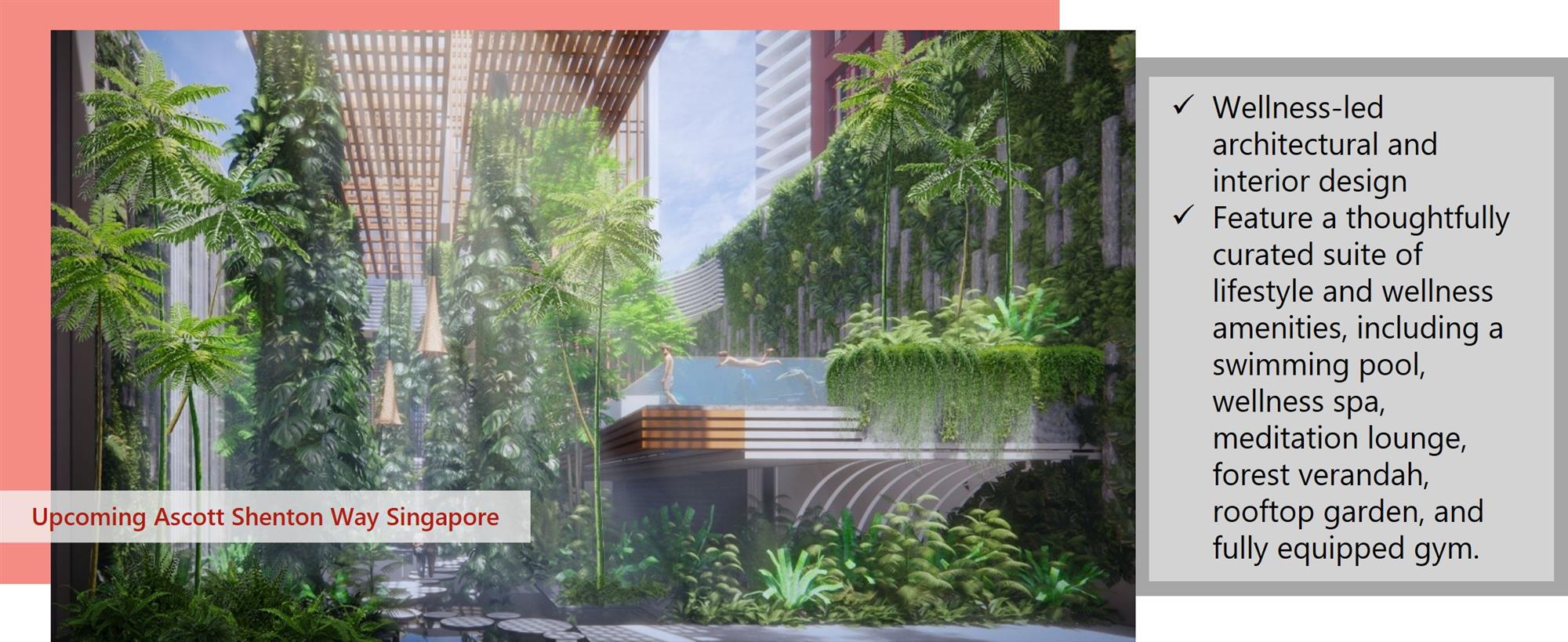

- Ascott Shenton Way, 137-key

FIGURE 9: Singapore Hotel Rooms Pipeline (2026 to >2030)

Source: URA Q4 2025 Commercial Pipeline Report

# Planned refers to projects that are not yet under construction but have planning approvals, written and provisional

Government Land Sales (GLS)

In a bid to provide ample opportunities for developers to initiate additional supply of hotel rooms, the government periodically updates the list of hotel sites available for sale. Two sites are available for hotel development under the 2H2025 GLS programme:

1. River Valley Road

- Carried over from previous GLS programme

- 1.02ha site with a gross plot ratio of 2.8

- Yields up to 530 rooms

- Provide up to 2,000 square metres of commercial space

2. Telok Ayer Street

- New addition to 2H2025 GLS programme

- Mixed-use development comprising hotel, long stay serviced apartment and retail components

- 0.42ha site with a gross plot ratio of 7.0

- Yields up to 440 hotel rooms and 135 apartment units

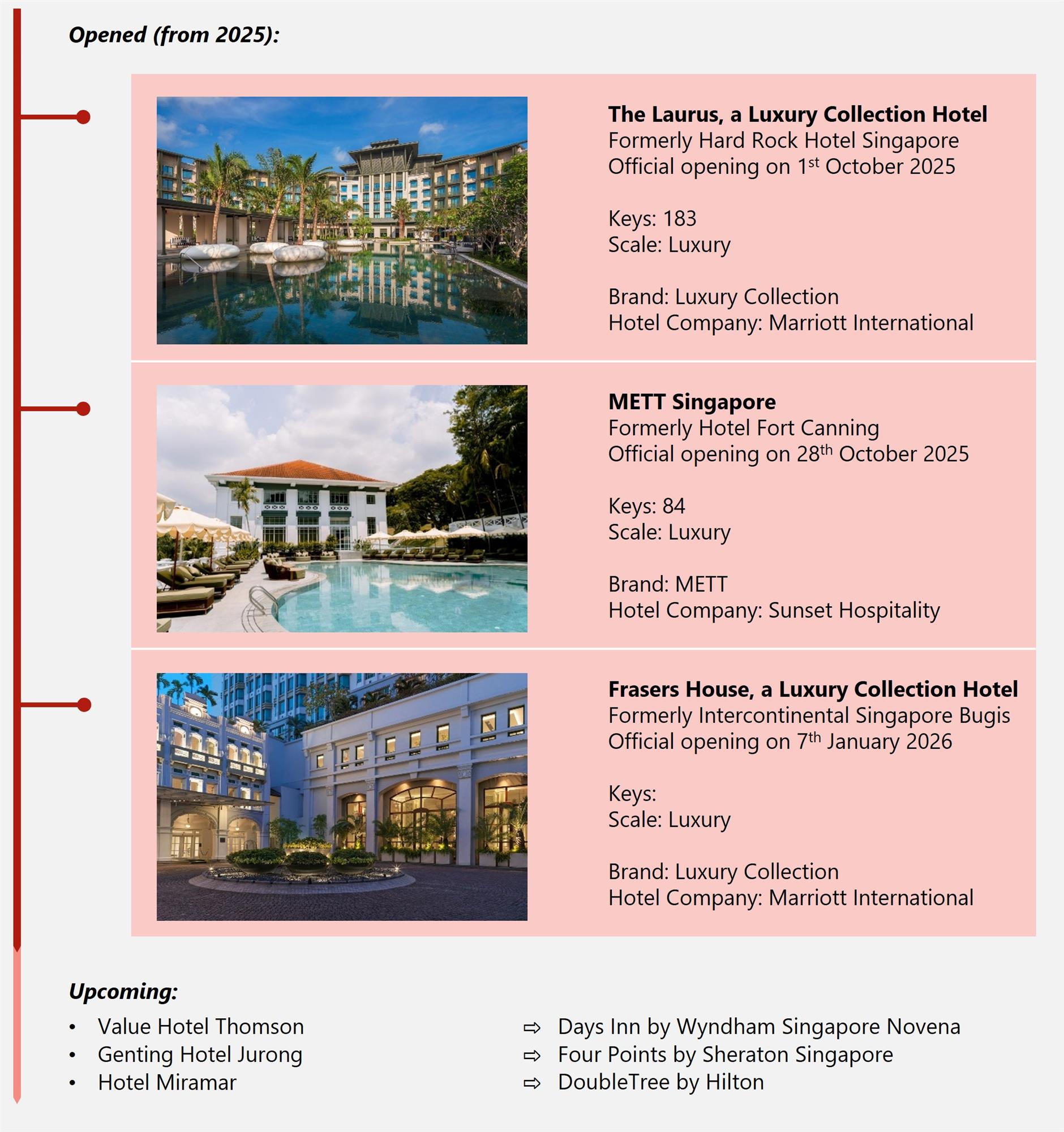

Notable Changes in the Hotel Landscape

Singapore remains a highly sought-after market from a branding perspective, though opportunities for new developments are constrained by limited available sites, particularly in prime locations. Coupled with the rapidly evolving hospitality landscape, longer development timelines for new-build hotels may result in projects becoming misaligned with initial market positioning. As a result, operators are increasingly pursuing refurbishment and rebranding strategies, with 2025 seeing a notable number of such transactions, including several flagship brand entries into the market via repositioned assets.

FIGURE 10: Singapore Hotel Rebranding Timeline (2025 and beyond)

Singapore Hotel Market

Singapore Hotel Market Performance

In 2025, the hotel market experienced a temporary moderation following a period of strong post-pandemic growth, reflecting short-term normalisation rather than a structural downturn. This deviation from the previous positive trajectory is considered atypical, with underlying demand fundamentals remaining intact. As such, performance is expected to recover and return to a stable growth path in the medium term.

FIGURE 11: Singapore Overall Hotel Performance (2019-2025)

.jpg)

Source: STB (taken in April 2026)

Note: On 29 Jan 2018, STB reviewed and updated the data estimation methodology for performance of the hotel industry (for gazetted hotels). The above figures should not be compared to HVS In-Focus Singapore publications prior to 2018.

FIGURE 12: Singapore Hotel Room Revenue by Segment (2024 vs 2025)

.jpg)

Source: STB

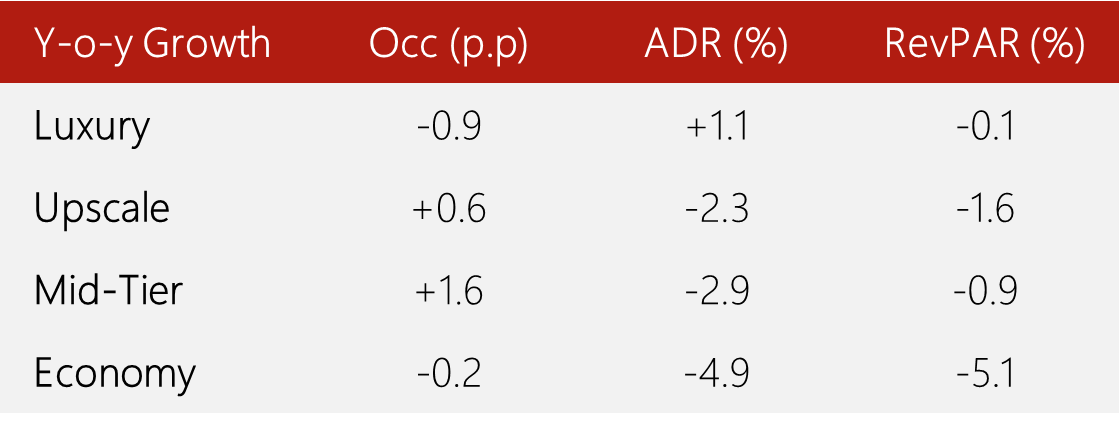

Singapore’s hotel market demonstrated mixed performance across segments. The luxury segment recorded a slight decline in occupancy alongside a modest increase in ADR, resulting in a marginal decrease in RevPAR. In contrast, the upscale and midscale segments saw improvements in occupancy but experienced declines in ADR. The economy segment recorded the sharpest decline in RevPAR, primarily driven by a decrease in ADR. Amid increasing supply and a continued shift in demand towards higher-end accommodation, supported by Singapore’s positioning as a premium destination, the luxury segment has remained relatively resilient, while budget hotels continue to face downward pressure on rates.

FIGURE 13: Singapore Hotel Segment Performance (2025)

Source: STB

Hotel Transactions & Investment

Sustained Recovery Momentum in 2025

Singapore’s hotel investment market has fluctuated in recent years, shaped by economic conditions, investor sentiment, and travel trends. During the pandemic, from 2020 to 2022, transactions were largely limited to smaller, independent hotels, while 2023 saw minimal activity with only three deals recorded. Sentiment improved in 2024, with momentum continuing into 2025, which recorded 10 transactions totalling approximately SGD1.215 billion. The increase in branded assets and larger deal sizes reflects renewed confidence in Singapore’s long-term hospitality fundamentals, supported by a lower interest rate environment. While still below pre-pandemic levels, this recovery signals a strengthening investor appetite for quality hotel assets.

Looking ahead to 2026, Singapore’s hotel transaction market is expected to remain active, supported by a low-interest-rate environment and the country’s positioning as a safe-haven investment destination amid global uncertainty. However, ongoing financial and geopolitical volatility is likely to temper investor risk appetite, resulting in steady but measured growth in transaction activity rather than a sharp rebound.

Key hotel transactions in 2025:

- 48-key 21 Carpenter at SGD100 million (SGD2.08m/key) in April

- 299-key Citadines Raffles Place at SGD280 million (SGD936k/key) in May

- 50.1% interest in the 634-key JW Marriott Hotel Singapore South Beach at SGD285.6 million reflecting the hotel value at SGD570.1 million (SGD899k/key) in September

FIGURE 14: Singapore Hotel Transactions (2019 – 2025)

.jpg)

Sources: HVS Research & Real Capital Analytics (RCA)

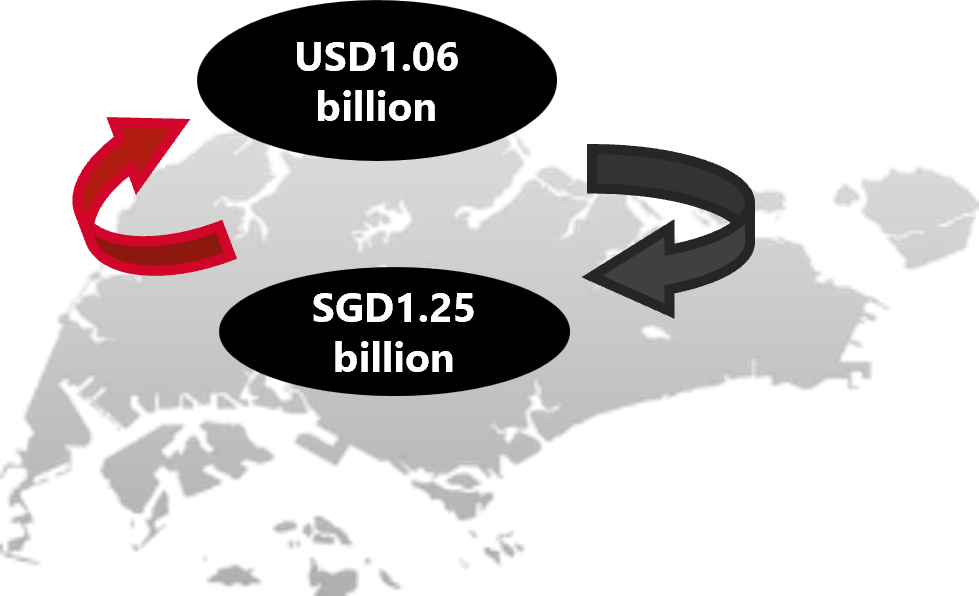

Outbound

In 2025, Hotel Investment Volume outbound investment by Singapore investors decreased by 31.3% in volume from USD1.54 billion in 2024 to USD1.06 billion.

FIGURE 15: Singapore Inbound and Outbound Hotel Transactions (2025)

Sources: HVS Research & RCA

Approximately 61.7% of the total outbound hotel investments were made in Asia Pacific, while 38.3% were made in Europe, the Middle East, and Africa (EMEA). There were no outbound hotel investments made in the Americas in 2025.

The top 3 outbound hotel markets for Singapore in 2025 were:

- United Kingdom (USD394.4 million)

- Japan (USD263.5 million)

- South Korea (USD119.2 million)

FIGURE 16: Outbound Hotel Transaction Markets (2025)

.jpg)

Sources: HVS Research & RCA

Wellness-Focused City in Nature

Wellness Tourism Landscape in Singapore

Singapore is renowned as a “City in Nature” and an urban wellness destination, underpinned by a holistic approach in which infrastructure, environment, and lifestyle converge to make wellness an integral part of everyday life.

The city seamlessly integrates greenery into the urban fabric through parks, nature reserves, vertical gardens, and tree-lined streets, with biophilic design increasingly embedded in its architecture. This is complemented by an extensive Park Connector Network that links green spaces with key urban attractions, creating an integration of nature and city life that supports both physical and mental health.

The country has also cultivated a strong wellness ecosystem. From luxury spas and integrative medical centres to boutique fitness studios and recovery-focused spaces, the city offers a wide spectrum of services that cater to both residents and wellness travellers.

According to the latest report by the Global Wellness Institute, Singapore’s wellness economy is rapidly growing. In 2024, the city ranked 37th globally and 14th in the Asia Pacific region with a market value of approximately USD23.2 billion, or about 4.2% of total GDP.

Aligned with this trajectory, the Singapore Tourism Board’s Tourism 2040 roadmap positions wellness as a key pillar of its value-over-volume strategy, focusing on high-end, science-backed offerings to enhance the city’s global appeal.

Wellness is increasingly viewed not just as a necessity, but as a curated, luxury experience—one that is compelling enough to inspire travel in its own right. Today, the wellness scene in Singapore spans far beyond spa and delivers multifaceted offerings:

FIGURE 17: Multifaceting Wellness Offerings

Wellness Attractions

An Urban Wellness Hub

In 2024, Singapore Land Authority awarded the tender for wellness and fitness uses at 13 and 13A Dempsey Road to Power Moves, which has since commenced operations of its pilates studio, medical spa, and aesthetic services.

In 2025, the Singapore Tourism Board awarded the tender for Singapore’s first dedicated wellness attraction at the Marina South Coastal site to Austria-based wellness developer and operator, Therme Group. This represents the Group’s first foray into the Asia Pacific region.

Source: Therme Singapore and DP Architects

Slated to open by 2030, the SGD1 billion state-of-the-art wellbeing destination will span 4 hectares along the Marina South waterfront. The world-class facility will feature a wellness-themed hotel, thermal pools, saunas, steam baths, water slides, lush botanical landscapes, world-class art installations, and cutting-edge health technology. Therme Group will also develop a public park of nearly four hectares, creating a seamless green link between Marina Barrage and the upcoming wellness attraction.

When completed, it is projected to welcome around 2 million visitors annually, with approximately half being foreign visitors. The main target markets are families with children, seniors and working adults.

Source: Therme Singapore and DP Architects

Therapeutic Gardens

Pioneering Therapeutic Gardens Tourism

In Singapore, therapeutic gardens are intentionally designed to deliver both physical and mental health benefits. They support rehabilitation and relaxation, enhance well-being, help reduce anxiety, while also benefiting individuals with conditions such as autism, dementia, depression, attention-deficit/hyperactivity disorder (ADHD), and agility. Many of these spaces feature interactive wellness activities that improve physical skills and enhance cognitive functions, alongside sensory zones designed to stimulate the senses and evoke positive emotions. Beyond public parks, the therapeutic garden concept has been integrated into hospitals, senior care facilities, and schools.

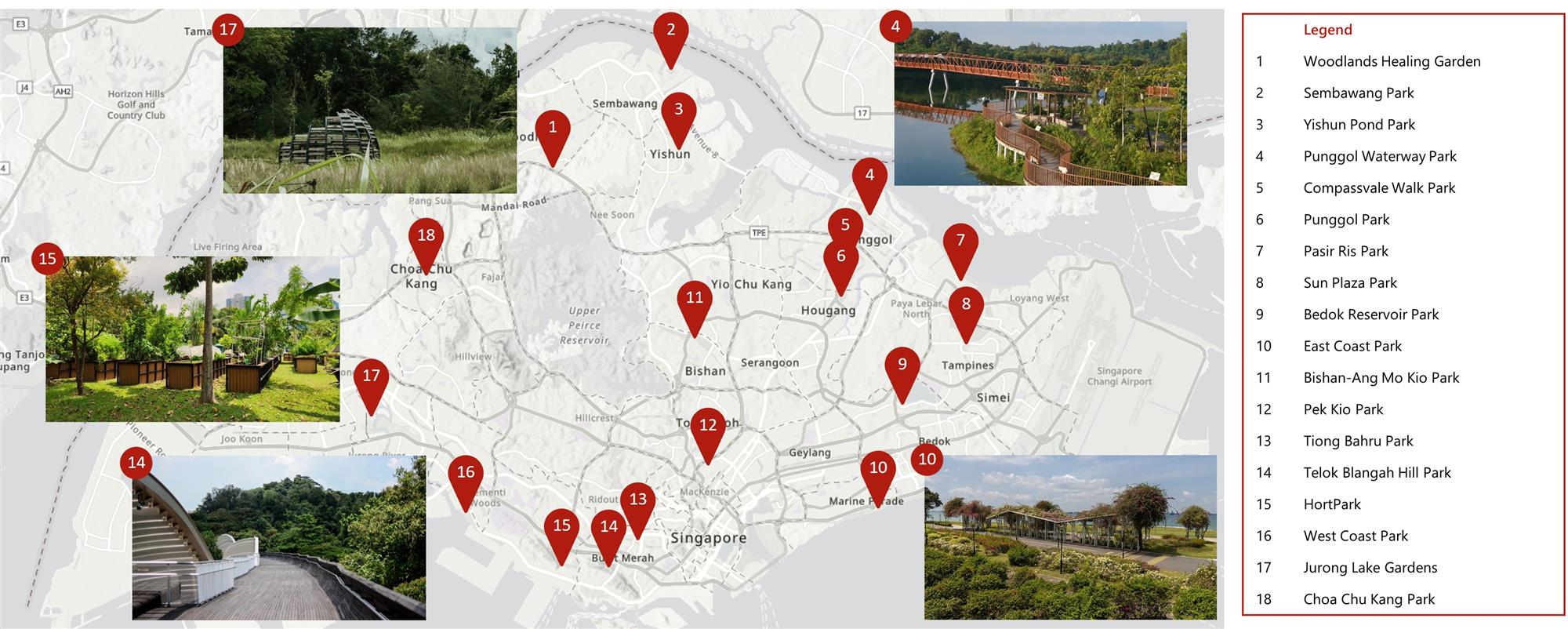

Currently, the country boasts 18 therapeutic gardens, and there are plans to establish 30 by 2030. The National Parks Board is also developing a therapeutic horticulture programme, through which interested groups can register for guided sessions.

The establishment of therapeutic gardens across the country aligns with its aim to become one of the world’s leading wellness destinations while addressing the diverse needs of various users, including an aging population, individuals seeking mental health support, persons with special needs or physical disabilities, and patients undergoing rehabilitation.

FIGURE 18: Location Map of Therapeutic Gardens

Sources: HVS Research, Unsplash, Flickr, Wikimedia Commons

Wellness Centres and Medical Spas

Premier Wellness Centres and Medical Spa Scene

Singapore is experiencing a notable rise in wellness centres, medical spas, and bathhouses. Medical aesthetics, along with advanced therapies like infrared sauna, cryotherapy, red light therapy, hydrogen therapy, hyperbaric oxygen therapy, hydrotherapy, lymphatic technology are becoming increasingly mainstream, reflecting a broader shift toward preventive, recovery and tech-enabled wellness. Fitness centres are also evolving to integrate recovery facilities within their premises.

Specialised recovery centres such as Rekoop offer members-only social wellness clubs featuring science-backed recovery therapies and Ayurvedic treatments, while Soma Haus focuses on restorative practices including craniosacral therapy, physiotherapy, and Pilates. These facilities support a wide range of health concerns, including cancer, chronic pain, anxiety, trauma, mental health conditions, skin disorders, sleep disturbances, digestive issues, as well as stress, burnout, and fatigue.

Recently opened, BUBBLE HOUSE+ is an urban bathing and city wellness house featuring soaking pools with rotating herbal infusions. The space also offers a comprehensive range of facilities, including a dry steam room, salt therapy room, earth nest room, mugwort herbal room, private sanctuary suites, buffet dining, cinema, an esports room, and a lounge area.

Soft launched in March 2026, Capybara Bathing features magnesium infused thermal baths, a traditional hot stone sauna, cold plunges, steam room and a Nordic-inspired hot lounge.

Looking ahead, Madison House, a wellness-focused private members’ club by Sunset Hospitality Group, is set to debut in Q2 2026 at Fort Canning. The club integrates wellness, fitness, dining and social experiences within a single venue.

Source: BUBBLE HOUSE+, Freepik, Unsplash

Wellness Hotels

Surge in Wellness-Focused Hotels

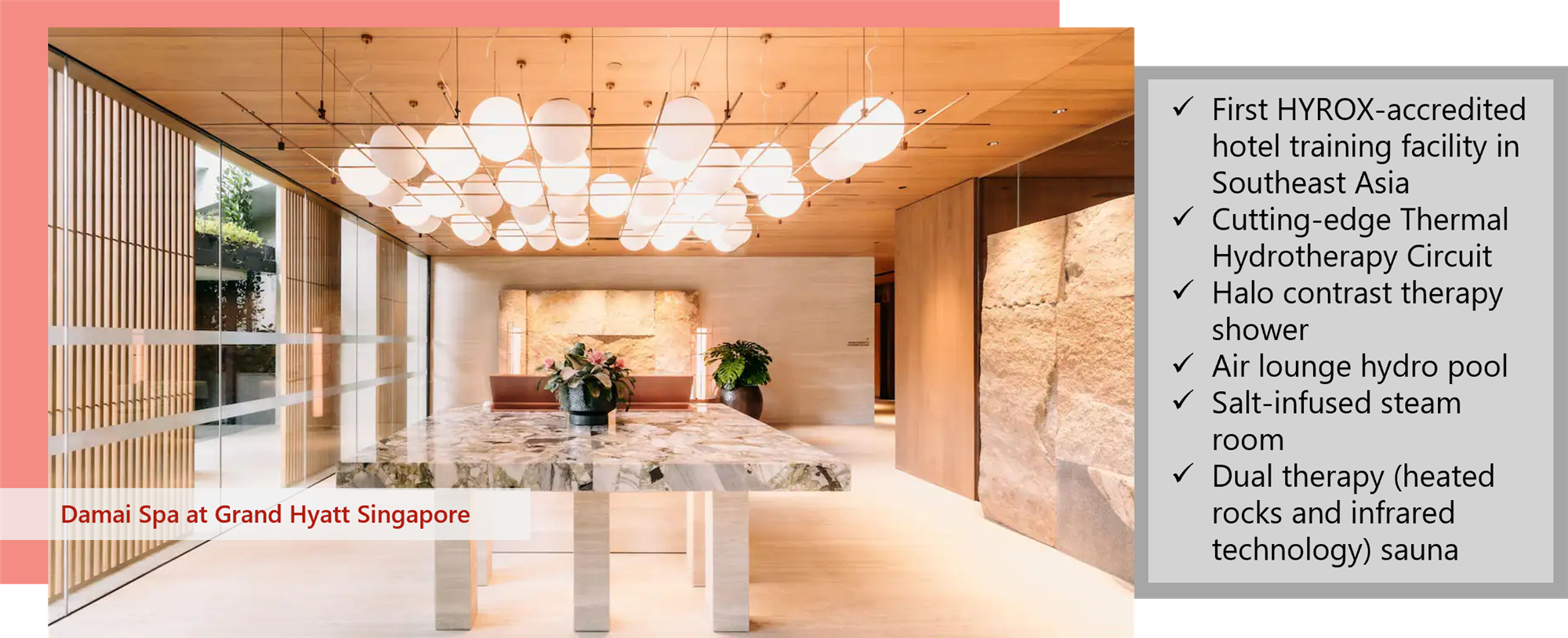

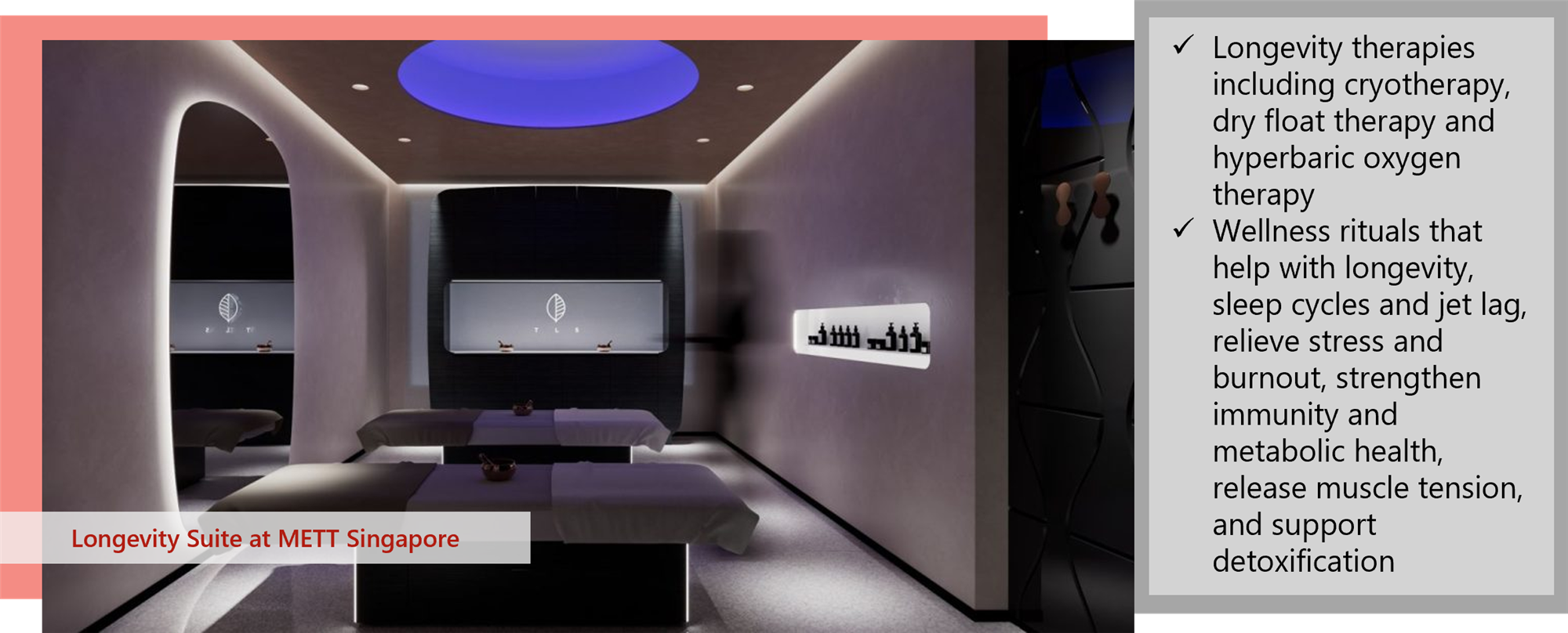

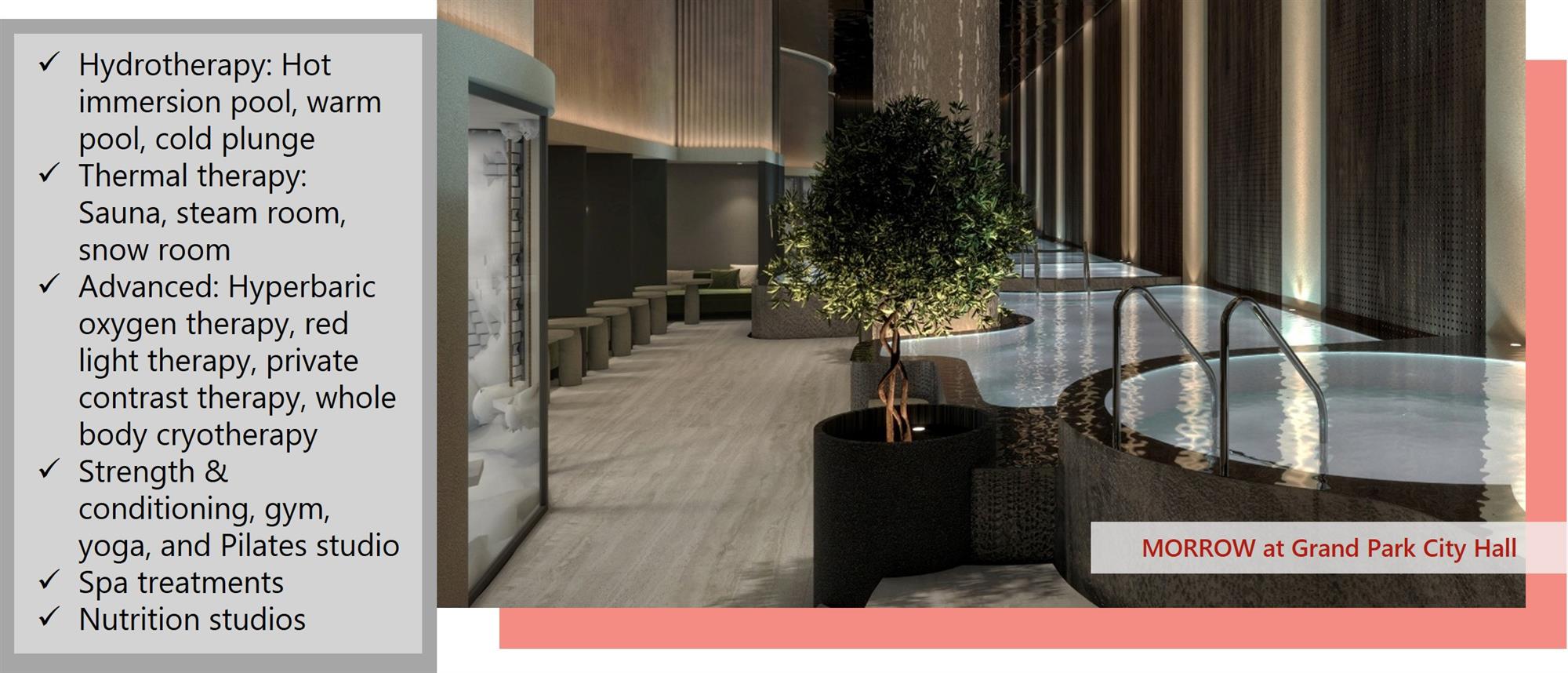

International hospitality brands with strong wellness offerings include Six Senses, Aman, COMO Shambhala, and Chiva-Som. In Singapore, hotels are increasingly pivoting toward a wellness-focused positioning, incorporating science-backed technologies and structured health programs.

In 2025, Four Seasons Hotel partnered with Chi Longevity to open its first private longevity clinic in Singapore. The medically licensed clinic offers advanced diagnostics, targeted therapeutics, and personalised lifestyle intervention aimed at slowing the biological ageing process. In the same year, Pan Pacific Hotels Group announced plans to reposition St. Gregory as a part of a larger wellness destination within each hotel. In November 2025, St. Gregory at PARKROYAL on Beach Road was relaunched following a comprehensive refurbishment. The new St. Gregory spa now combines spa therapies and hydrotherapy at a dedicated wellness floor with upgraded facilities to support holistic wellness and curated fitness programmes. New features include the installation of a professional-grade diagnostic body composition machine, the integration of neuroscience-based sleep and relaxation technology.

Source: Grand Hyatt Singapore

Source: Freepik

Source: METT Hotels and Resorts

Source: MORROW

Source: The Ascott Limited

Wellness Real Estate Alternatives

Wellness Senior Living

In August 2025, Singapore-headquartered Perennial Holdings unveiled Perennial Living, Singapore’s first private assisted living development, blending luxury living and five-star hospitality services with comprehensive care provided through Perennial Wellness, an integrated medical, Traditional Chinese Medicine (“TCM”), rehabilitation and fitness, and diagnostic imaging centre within its premises, as its core offering. The five-storey development consists of 200 assisted living apartments, 100 nursing home beds and a Clubhouse with an All-Day Dining restaurant, hydrotherapy and swimming pool, rehabilitation and fitness centre, karaoke lounge-cum-movie theatre and multi-purpose room. Residents also enjoy seamless access to an adjoining functional and innovative therapeutic park of approximately 1.5 hectares. The development’s comprehensive suite of services also includes dementia and nursing care, and outpatient clinical and wellness services.

The basic package spans accommodation, regular cleaning, housekeeping and linen service, meals, use of all amenities, social and wellness programmes and curated East-meets-West care, comprising consultations with Western medical specialists, TCM physicians or rehabilitation therapists. This package also includes bi-annual health screenings, preventive health and vitality treatments, such as mild hyperbaric oxygen therapy, strength training and usage of health vitals’ monitoring devices.

Payable add-on services comprise treatments with partner medical specialists, TCM therapies, integrated rehabilitation programmes, nursing care and home visits by medical and care teams, dental and podiatric care. Other payable menu options include concierge services and grooming services.

Source: Perennial Living

Wellness Confinement Hotel

In addition to housekeeping services and complementary access to hotel facilities and in-room amenities, confinement hotel offers a wide range of specialised support services. These include round-the-clock professional care, nursery services, daily confinement meals, lactation consultation, baby care guidance, baby and breast massage, postnatal massage treatments, and cryo facial treatments. Guests can enjoy daily in-house prepared herbal baths, wellness activities, provision of diapers and essential baby consumables, daily laundry, and transportation between the hospital and hotel.

KAI Singapore, the first licensed premium confinement hotel in Singapore, is a one-stop facility offering holistic, specialised pre- and postpartum care services. KAI features 18 thoughtfully designed private suites, a hair salon, lobby lounge, multi-purpose function room, nurseries, private lounge, yoga studio, spa, and wellness treatments.

.png)

Source: KAI Singapore

Located on the 12th floor of Artyzen Singapore Hotel, DeRAMA is Singapore’s first Korean confinement centre. DeRAMA features eight suites for guests, two treatment rooms for massage therapies, a nursery, and a lactation room. DeRAMA offers a postpartum and newborn care program, with meals crafted by Korean nutritionists.

Source: Deenise Glitz

Oasia Resort Sentosa has established a collaborative partnership with My Queen to offer a premium, resort-style prenatal and postnatal care experience. These retreat packages range from a 3-day short-stay option to a comprehensive 28-day full-service programme.

Source: My Queen

Wellness Cruises and Festivals

Wellness Cruises

Cruise ships are redefining well-being by offering an expanding array of holistic experiences that integrate therapies, fitness, nutrition, movement, and mindfulness. The spa has evolved into a central feature on most luxury vessels, reflecting a broader commitment to wellness at sea, supported by significant new investment in innovative spa concepts and comprehensive wellness programmes.

In January 2026, StarCruises partnered Under Armour to launch 'Fitness @ Sea’, a fitness-themed cruise sailing from Port Klang to Phuket and Singapore. The cruise features a structured fitness programme integrated into a standard cruise itinerary. The daily complimentary workouts were led by Under Armour-certified trainers and guests completing the full series can receive Under Armour merchandise.

On March 2026, Disney Adventure officially set sail from Singapore. The cruise features a comprehensive wellness sanctuary including a spa with hammah, salt room and aromatherapy steam rooms, a fitness centre with meditation rooms, dedicated spaces for yoga and cycling, and a juice bar.

Between September 2027 to December 2028, Explora Journey will debut its first Asia sailing, with EXPLORA III operating 28 journeys to 47 destinations, including Singapore. The newest addition to its luxury fleet will feature an expanded Ocean Wellness Complex that integrates spa, fitness and mindfulness spaces into a single immersive zone. Enhancements include new signature spa treatments, the Sava Sound Pod for restorative audio therapy, upgraded Technogym fitness and Pilates equipment, an expanded sports court and a longer open-air running track.

Wellness Festivals

Conclusion: Wellness-Focused City in Nature

Across Asia, an increasing number of countries are prioritising wellness tourism, leveraging nature-based experiences, retreat-style offerings, medical wellness, and technology-driven solutions. Singapore must leverage its unique strengths to differentiate itself from other wellness destinations. These include its positioning as a leading urban wellness hub, complemented by diverse architecture, world-class gastronomy, proximity to other Asian destinations, exceptional cleanliness, robust healthcare infrastructure, excellent accessibility, strong sense of safety and security, and the availability of high-quality wellness products and services.

Outlook

Looking ahead to 2026, Singapore’s tourism and hospitality sector is expected to sustain its growth momentum, driven primarily by higher visitor spending rather than volume, in line with the country’s strategic shift towards a quality-over-quantity (value-over-volume) tourism model. In 2025, Singapore welcomed approximately 16.9 million international visitors, reflecting moderated growth of 2.3% year-on-year and reaching 88.5% of 2019 levels. In contrast, tourism receipts rose strongly, reaching SGD23.9 billion over the first three quarters, 6.5% higher than the same period in 2024, and setting a record for this period. Full-year receipts are expected to exceed STB’s initial forecast of SGD29.0 to 30.5 billion, marking a new peak in visitor spending.

For 2026, STB projects continued but measured growth, with international visitor arrivals expected to reach 17 to 18 million and tourism receipts forecast at approximately SGD31.0 to 32.5 billion. This reflects a resilient outlook supported by higher-value tourism, albeit tempered by global economic uncertainty and geopolitical risks that may influence travel patterns.

In line with this trajectory, the Tourism 2040 roadmap, announced in late 2025, underscores Singapore’s long-term focus on sustainable, high-value tourism growth. Under this strategy, STB targets tourism receipts of SGD47 to 50 billion by 2040, reinforcing the shift towards attracting higher-spending visitors rather than maximising arrival volumes.

The core pillars of the strategy are:

- Capturing future demand

- Enhancing destination appeal with new products and experiences

- Developing a future-ready tourism industry

In 2026, Singapore will introduce a strong pipeline of new experiences, including the F1 Singapore Grand Prix sprint race, Disney Cruise Line’s first Asia homeport, and the opening of LiveNation’s Grange Road Events Space, further enhancing its events and entertainment offerings. These developments also support Singapore’s efforts to capture future demand, particularly from higher-value segments such as MICE and experiential travellers.

To enhance destination appeal, Singapore is expanding into high-value growth segments such as wellness, with STB identifying opportunities across wellness attractions, centres, medical spas, longevity clinics, and wellness hotels, while broader trends such as sustainability and experiential offerings continue to shape the market. Notably, approximately 61% of hotel room stock has already achieved internationally recognised sustainability certifications, reinforcing Singapore’s positioning as a responsible tourism destination.

In line with developing a future-ready tourism industry, the refreshed Hotel Industry Digital Plan is accelerating the adoption of technologies such as AI, smart room systems, robotics, and digital concierge platforms to enhance operational efficiency and guest experience, positioning Singapore’s hotel sector to remain competitive in an increasingly technology-driven landscape.

Additional Contributors to this article: Chariss Kok, Vice President, and Vanessa Jaquemet, Analyst