Foreword

Our last review of the Israel Hotel Market was published in the summer of 2020 when the world was immersed in huge uncertainty owing to the COVID-19 pandemic – many countries were in varying states of lockdown, travel was suspended for most and no-one was quite sure whether this was just a short-term inconvenience or something more serious. As I write this in February 2022, we are in an equally unprecedented situation as the Russian invasion of Ukraine unfolds in front of us, making the subject of recovery in the hotel sector less certain as across the world we hope and pray for a swift solution.

Our report focuses on the issues specific to Israel that will encourage recovery and the fact the world has admired the way in which the country has dealt with the pandemic, not least for the speed with which it vaccinated its population, with most now having had a fourth jab. Sadly, that also meant closing down the country to international visitors and the consequent impact that had on Israel’s previously burgeoning tourism sector. Somewhat remarkably during this period, the Abraham Accords were signed with a number of countries – most notably Bahrain, the UAE and Morocco, where tourism plays an enormous part in each country’s economy.

The importance of tourism to each country’s GDP cannot be overstressed. Israel’s contribution at 2.5% lags well behind those of Bahrain (5.3%) and the UAE (5.8%), and Morocco’s tourism contribution is a staggering 12.2%. There are huge opportunities available to Israel by improving its tourism sector, attracting more international visitors and achieving the potentially considerable boost to the Israeli economy that can ensue therefrom.

If Israel is to succeed in achieving its newly appointed Tourism Minister’s present goal of attracting 10 million international visitors (compared with the record 4.5 million achieved in 2019), there needs to be a substantial increase in the number and quality of hotel bedrooms, especially in Tel Aviv and Jerusalem, requiring significant capital investment.

If the tourism sector in Israel can be increased from contributing around 2.5% to GDP to a more realistic 4%-5%, this should result in the following.

- Increasing the number of international visitors, bringing foreign currency and improving the balance of payments.

- Aligned with the development of international visitation to Israel is the encouragement of more international airlines to seek bilateral routes, benefiting from Israel’s existing ‘open skies’ policy which is well established.

- The effect of the ‘tourism multiplier’ enables the country to benefit from visitors' spending in shops, restaurants and bars as well as hotels, transportation and attractions, and consequently the economic impact experienced by each of these enterprises, both secondary and tertiary.

- Increasing the employment of Israeli citizens within the broader tourism sector – not just hotels and restaurants, but in more general tourism employment including inter alia tour guides, coach drivers, car rental, taxis, workers in museums and attractions, and so forth.

- If the quality and pricing of hotels and holidays within Israel can be made more attractive to Israeli citizens, fewer would be inclined to travel abroad and would take their vacations within Israel, thereby further improving the sector’s performance, the overall balance of payments (by reducing ‘leakage’) and improving tourism’s contribution to Israel’s GDP.

- The development of new hotels – or extensions to existing properties – improves employment opportunities for Israelis in the construction and related sectors; suppliers of goods, materials and services; and with a consequent spin-off into secondary and tertiary sectors.

- As more hotels are developed, opportunities for branding with internationally known hotel brands will intensify, thereby broadening the reputation of hotels.

However, the speed with which Israel can derive benefit from these initiatives will heavily depend on how quickly the government can be persuaded to reduce the ‘red tape’ associated with new developments (planning consents and so forth) as well as Israeli banks being encouraged to adopt many of the characteristics of their international counterparts.

My colleagues and I hope that this review of the Israel Hotel Market will assist investors, developers, owners and operators of hotels in Israel – both within the country and from abroad – to be part of the opportunity to grow the country’s hotel sector and the consequent improvement in its GDP as the travel and tourism sector increases its prominence within the Israeli economy.

Country Highlights

A Recovering Economy

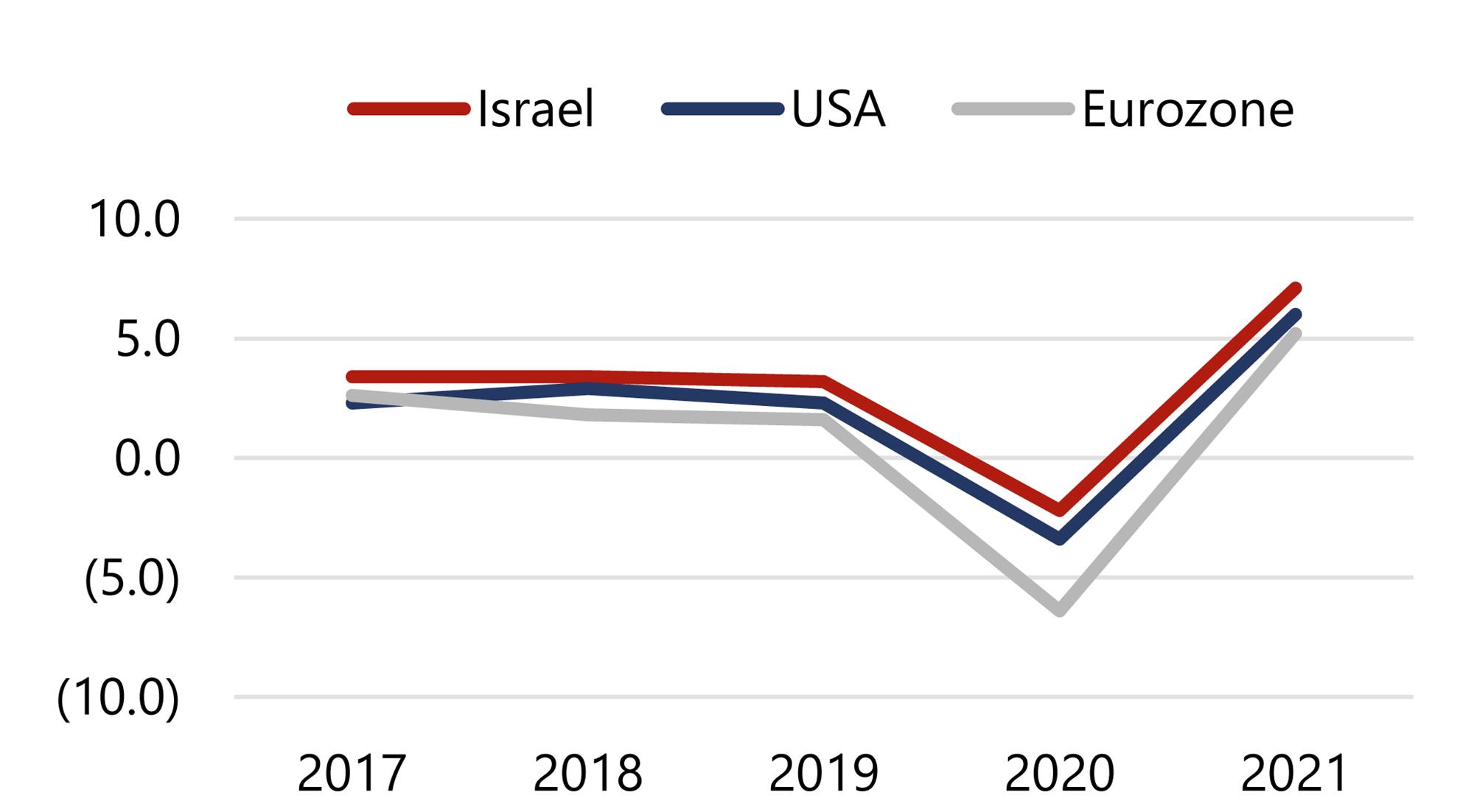

After facing a severe downturn in 2020 with a GDP contraction of around -2.1%, of which Travel & Tourism GDP decreased by 58.6% according to the WTTC, the Israeli economy rebounded strongly in 2021, recording growth of 7.1% (see Figure 1). Despite a strong fourth wave of the pandemic in the summer, economic recovery was accelerated by a successful progression of the booster vaccination campaign, a steadily recuperating labour market, and reducing uncertainty regarding COVID-19.

Figure 1: GDP % Change (Israel, USA & Eurozone)

Source: International Monetary Fund

On the back of increased private consumption and investment growth, alongside the continued strength of Israel's high-technology services, GDP growth is expected to return to its potential rate by 2023, according to the OECD. A worsening health situation or an increased level of inflation could, however, have an adverse impact on the forecast rate of growth.

A Year for the Abraham Accords

On 13 August 2020, the Abraham Accords were reached, a set of collective agreements with the purpose of normalising ties between Israel, the United Arab Emirates (UAE) and Bahrain. The main focus lies on deepening trade, investment, tourism and people-to-people ties among Abraham Accords members, as well as expanding the circle of countries that are part of the accords.

2021 witnessed substantial progress in the deepening of diplomatic relationships between the concerned governments, with the opening of embassies, appointments of first-ever ambassadors and historic bilateral visits between prime and foreign ministers. Furthermore, more than a year after the signing of these historic agreements, substantial improvements can be seen in trade relations and, as a result, commercial trade activities between Israel and Abraham Accords countries, as shown in Figure 2.

Figure 2: 2021 Trade Numbers Between Israel and Abraham Accords/Neighbouring Countries

(% increase over trade activity in 2020)

Source: Abraham Accords Peace Institute

Additionally, a focus has been placed on expanding the people-to-people ties between Abraham Accord member nations. The involved countries will work to increase tourism and cultural collaboration with Israel. Currently, there are direct flights established between Israel and the UAE, as well as between Israel and Morocco, albeit that such flights are currently suspended (Feb ‘22). Flights from Tel Aviv to Manama, Bahrain are set to begin in a few months' time.

Dark Year for Inbound Tourism

Before the pandemic, between 2016 and 2019, Israel's tourism industry recorded impressive growth in terms of tourist arrivals, at a compound annual growth rate (CAGR) of 16.2%. This came as a result of targeted marketing actions, easing of regulations for visas and an increased number of air routes thanks to the Open Skies agreement.

Data for 2020 and 2021, on the other hand, reflect consecutive decreases in visitation by foreign tourists. Since the beginning of the pandemic, Israel had largely barred foreign visitors and effectively 'closed its skies'. Fully vaccinated tourists were only allowed to enter from early November 2021, before this decision was overturned four weeks later in response to the spread of the Omicron variant.

Since 1 March 2022, all tourists, both vaccinated and unvaccinated, have been allowed to enter Israel upon submission of a pre- and post-flight PCR test in an effort to address the tourism industry's predicament.

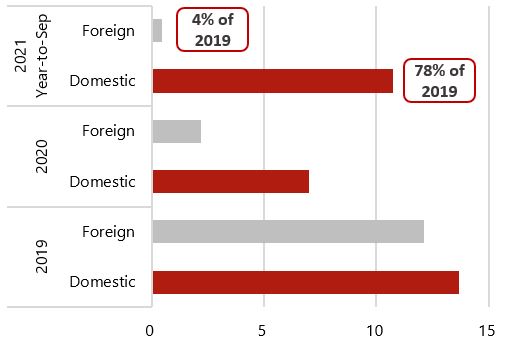

In a more positive light, a growing staycation trend boosted domestic bednights across Israel throughout the first three quarters of 2021, compared to 2020. As shown in Figure 3, domestic bednights for year-to-September 2021 equalled 78% of domestic bednights in 2019 and grew by 68% versus the same period in the previous year. As detailed later in this article, most destinations in Israel benefited from this trend in 2021, helping to drive hotel occupancy levels and average rates upwards.

Figure 3: Domestic & Foreign Bednights in Israel

Source: Central Bureau of Statistics

Hotel Market Performance

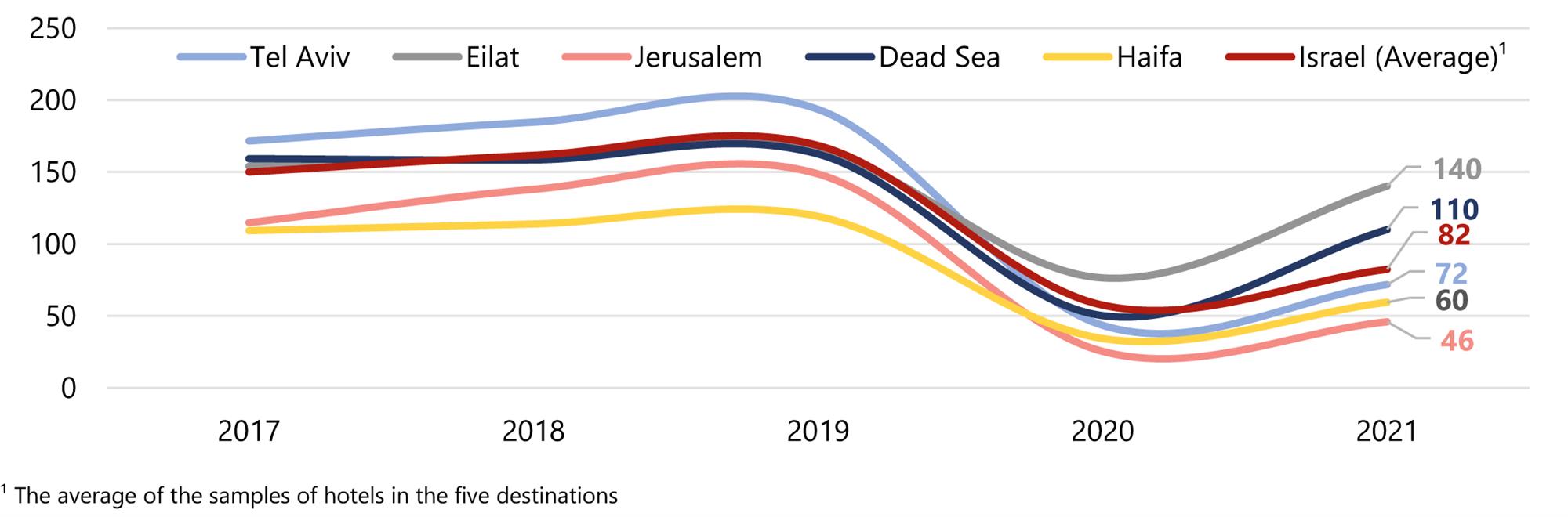

Much in line with the rest of the world, Israel's hotel industry suffered severely in 2020, as reflected in the data presented in Figure 4. The majority of hotels across the country closed for a large part of the year and, for those remaining operational, occupancy levels declined substantially. Average rates also suffered significantly, resulting in an overall RevPAR decrease of 68% for the total Israel market in 2020.

Figure 4: Historical RevPAR Comparison (US$)

Source: HVS Research

2021 reflects some of the positive upsides taken from the boost in the staycation trend as previously discussed. Hotels, especially in resort destinations such as the Dead Sea and Eilat, which in years unaffected by COVID already relied more on domestic visitation, took advantage of this and boosted both average rates and occupancy levels, resulting in impressive RevPAR recoveries of 119% and 84%, respectively. Jerusalem continued to struggle in 2021, reflecting the city’s heavy reliance on international visitation.

An Emerging Recovery

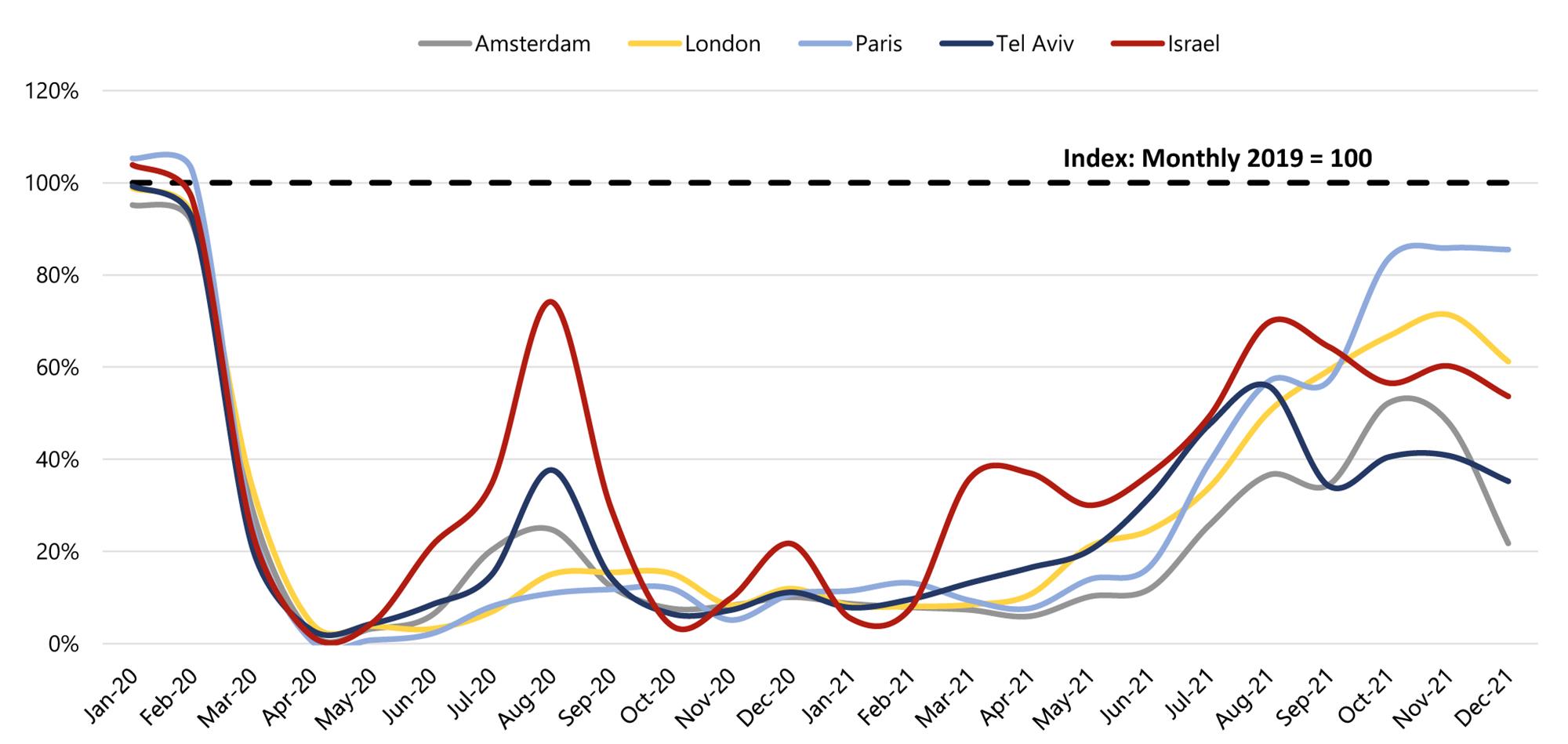

Across Europe, most major cities followed similar trends, as presented in Figure 5, which presents the RevPAR progression from the beginning of 2020 until the end of 2021 in US$ indexed to 2019, as per data from STR. As restrictions began to ease, the summer of 2020 started showing some uplift in hotel performance, especially for the Israel hotel market. However, this was short-lived as the end of the year was marked with further lockdowns, owing to the spread of the Delta variant. Data for January to August 2021, however, show an impressive recovery across most markets, while some experienced delayed uplifts on account of comparatively stricter COVID regulations in countries such as the Netherlands.

Despite the detrimental impact from the continuing closed skies and limited possibility for foreign visitation, July and August, particularly popular months for leisure tourists, witnessed a significant uplift in performance for the Israel hotel market. This can be connected to the staycation trend which played a key role in keeping hotels afloat during these months. Furthermore, the strong uplift in performance throughout 2021 experienced especially in markets where infection rates remained under control and regulations were kept to a minimum, give us a glimpse of light at the end of the tunnel. As world economies are trying to put COVID-19 behind them, we see encouraging signs for the recovery of tourism.

The last quarter of 2021 followed a similar negative trend across all markets, as the Omicron variant surfaced, and several governments reintroduced stricter COVID-19 regulations in order to tackle the situation.

Figure 5: RevPAR Performance Across Israel And European Markets 2020 & 2021 (US$; Index: 2019 = 100)

Source: STR

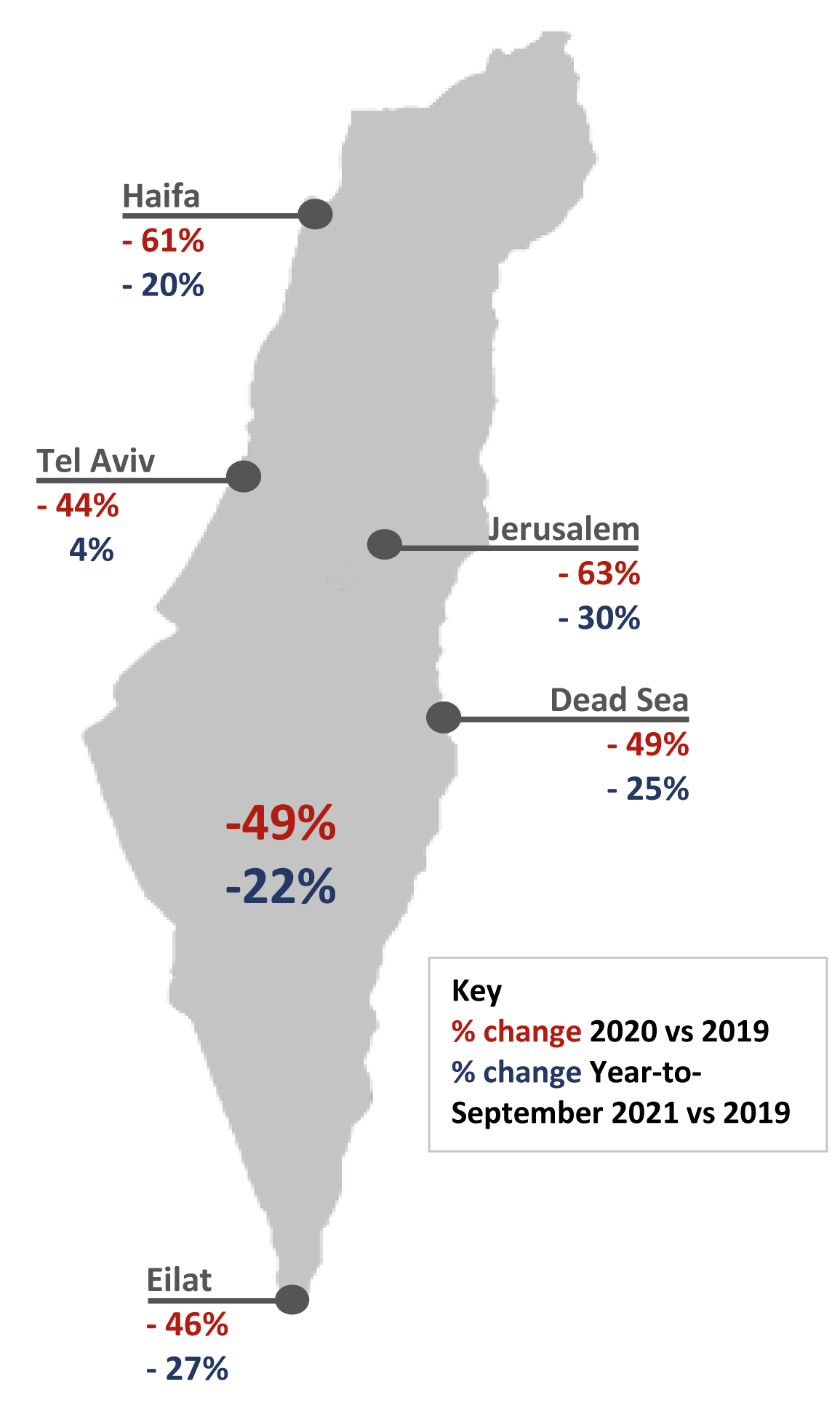

Domestic Tourism Carries Recovery

As discussed in our last Israel Hotel Market Overview, countries and markets with more reliance on international demand and air travel are likely to experience a longer tourism recovery curve. Nevertheless, in the short-term, holidaymakers, used to travelling overseas, opted for domestic destinations, increasing local demand. In 2019, 47% of bednights in hotels in Israel were generated by foreign tourists. This share of demand was almost fully halted by the strict 'closing of skies’ policy throughout most of the pandemic. Additionally, strict rules were put in place restricting overseas travel by Israelis, which in 2019 accounted for almost 9 million trips abroad. Figure 6 provides an overview of the change in room nights arising from domestic guests in year-to-September 2021 and 2020 versus 2019. The data show that, in the first three quarters of 2021, all major markets in Israel generated domestic demand figures close to full-year 2019 results. The Tel Aviv market even achieved a new record of domestic bednights, with approximately 900,000 in year-to-September 2021, compared to a previous high of 873,000 in 2019. We expect domestic demand and the staycation trend to continue to aid the recovery of tourism, albeit to a lesser extent, once international travel freely resumes, especially by returning tourists and business travellers.

Figure 6: Domestic Bednight % Change vs 2019

Source: Central Bureau of Statistics

Has The Government’s Focus Shifted?

As previously mentioned, throughout most of the pandemic Israel has kept its skies closed, to the detriment of the tourism industry, effectively blocking incoming tourism. The 'Green Pass' and 'Purple Badge' guidance were introduced in an effort to curb the soaring infection wave. 'Purple Badge' procedures required hotels to comply with set operating guidance to limit the spread of the virus and the 'Green Pass' scheme required hotel and restaurant guests to prove their vaccination status in order to access the venues. Additionally, all local authorities across Israel are subject to a traffic light model which ranks them according to the rate of new cases, the percentage of positive test results and the infection rate, in order to determine the required COVID-19 restrictions.

These restrictions, alongside the pandemic, in effect resulted in severely inhibited operations for the tourism industry. To tackle this, the government has provided economic stimulus packages of approximately NIS300 million (US$86 million) towards the tourism industry since the onset of the pandemic. However, with the ongoing increase in foreign investment, the government’s focus has shifted elsewhere and away from the tourism industry, which accounts for only 2.5% of the Israeli economy and is therefore not seen as a sufficiently critical industry for the country's economic recovery. In addition, the country faces an imbalanced labour market which could impact the tourism industry's short-term ability to fully reopen.

Tourism has been unable to supply work for large numbers of employees, owing to strict COVID regulations, and as a result many travel agents and tour guides never returned to work. A new plan was recently agreed, which offers tourism industry employees the chance to receive training in a different industry of their choosing.

Overall, the economy has been recovering with help from government stimulus packages; however, there currently is limited focus on the tourism industry, which could impact the long-term recovery potential.

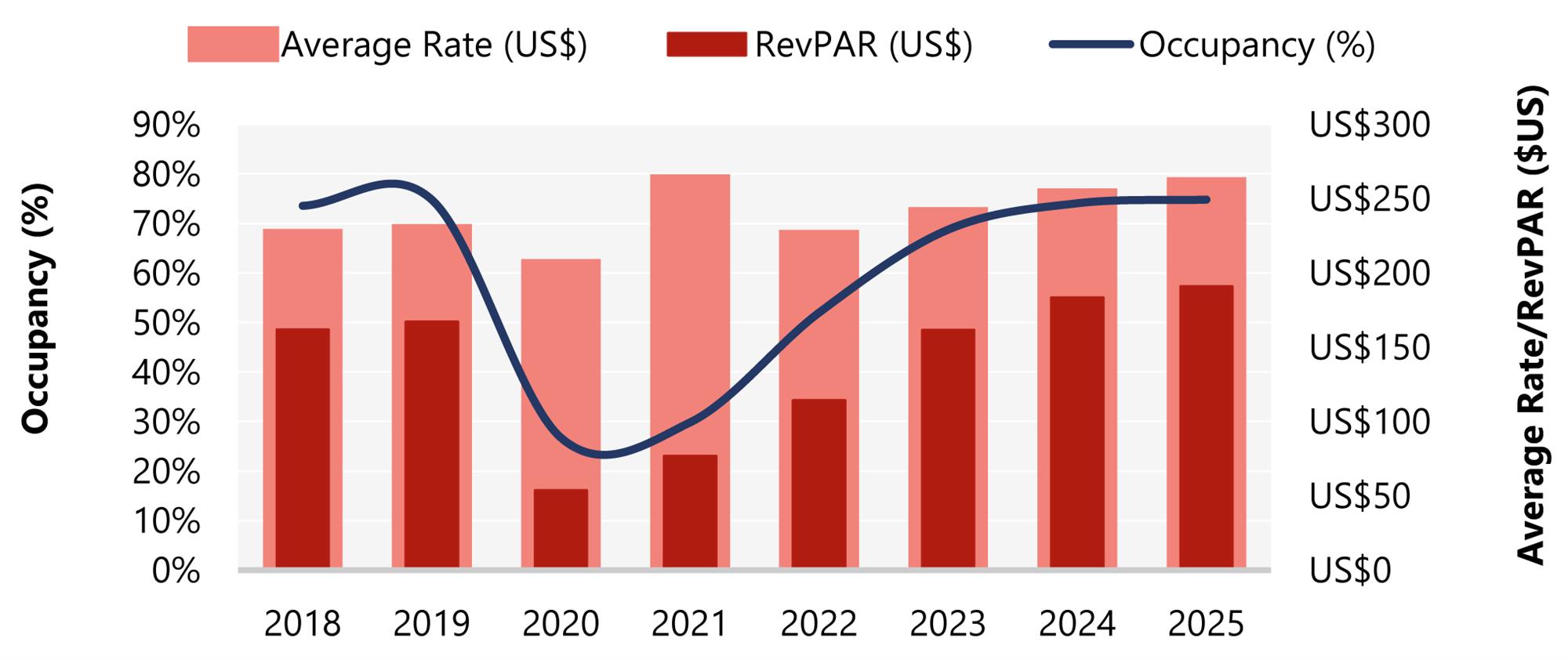

RevPAR Forecast

Recovery Expected by 2025

On account of the factors mentioned throughout this report, taking into consideration the noticeable recovery seen across Israel and European markets towards the third quarter of 2021, we present our current expectation for Israel's hotel market recovery in Figure 7. The impact of the current crisis in Ukraine will potentially affect this.

Owing to the current fluid situation as a result of the Omicron variant, HVS's forecast for Israel anticipates a slow start throughout the first quarter of 2022. However, for the duration of the rest of the year, on account of the successfully progressing vaccine booster roll-out across the world and the recovery potential seen throughout Q3 of 2021, along with the gradual reopening of air travel routes, we expect occupancy levels to pick up again, resulting in a RevPAR increase of 49% in 2022. Occupancy is expected to recover by 2024, while the average rate is expected to soften in the next two years as lower-rated segments return to the market, before stabilising in 2025.

We expect this recovery to continue to be driven by domestic demand in the short term, before international leisure travel resumes once more restrictions are lifted. After all, it was not an economic problem that caused the retraction of tourism & travel demand, and we therefore foresee the bounce back to come somewhat easier than after previous downturns caused by events such as 9/11 and the Global Financial Crisis.

Reflected in the 2021 monthly performance for the majority of markets, there is plenty of pent-up demand, which needs an outlet. As governments eased restrictions and travel corridors were put into place, occupancy rates picked up rapidly, proving the hotel industry’s resilience and ability to recover.

Figure 7: Performance Outlook for Israel’s Hotel Market

Source: HVS Research

Hotel Development

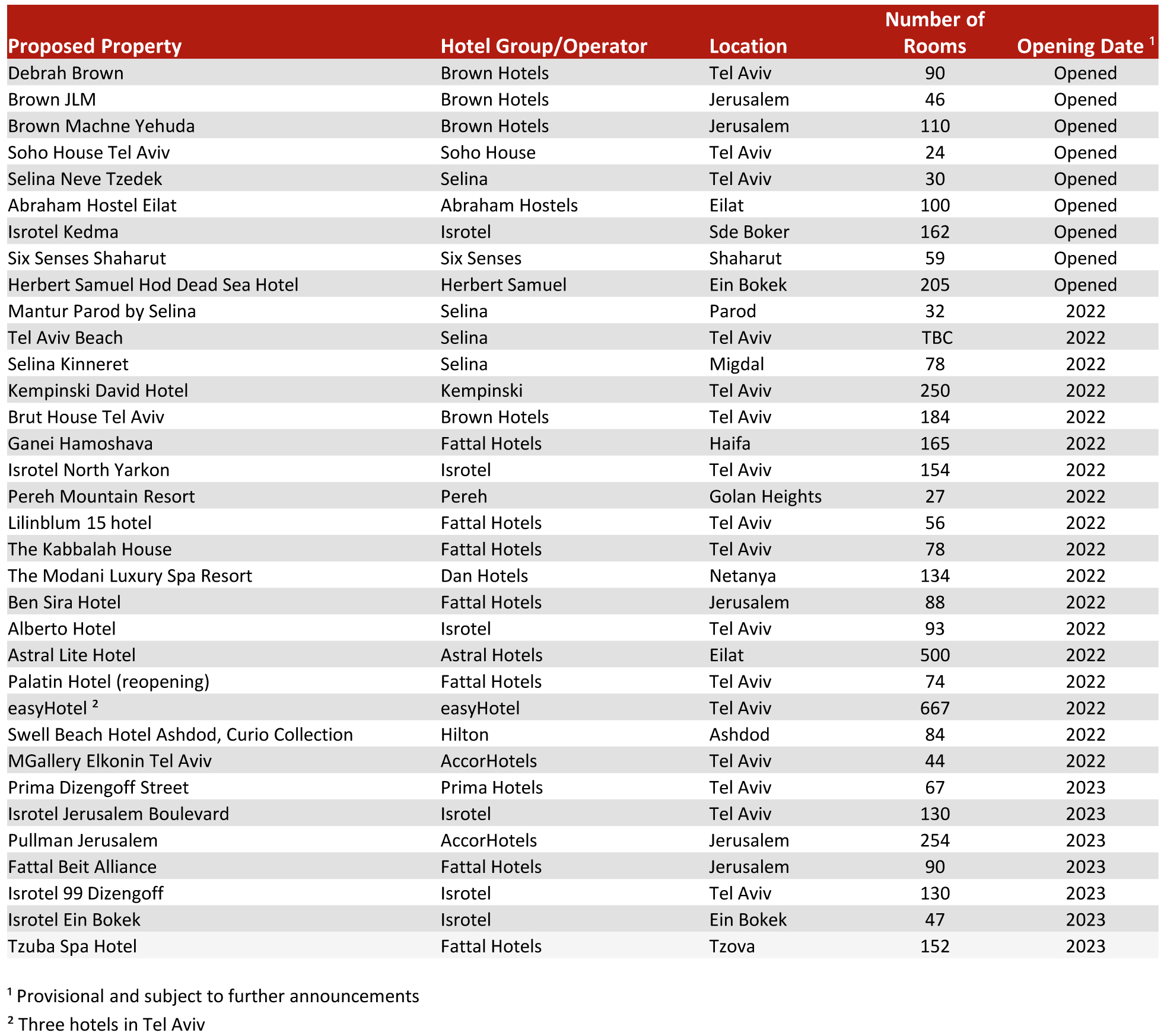

Although Israel's hotel industry was adversely affected by the COVID-19 pandemic over the last two years, Israeli hotel entrepreneurship remains strong and hotel investment levels are up. Prior to the pandemic, the Israel hotel pipeline stood at record levels and, despite the recent struggles, has not come to a halt but rather the majority of planned projects continued to move forward, albeit with some delays. With support from government grants, the number of hotels currently in the planning stage or under construction totals many hundreds of new rooms.

The pipeline is led by several familiar, and international, operators, with a large share of developments due to enter the Tel-Aviv market, supporting the hoteliers’ belief that tourism growth there will soon resume.

Figure 8 provides an overview of recently opened properties and new supply in Israel. The opening dates exclude possible further delays caused by the current situation, and we expect more certainty around those projects over the next 12 months.

Figure 8: Recently Opened Properties and New Supply

Source: HVS Research

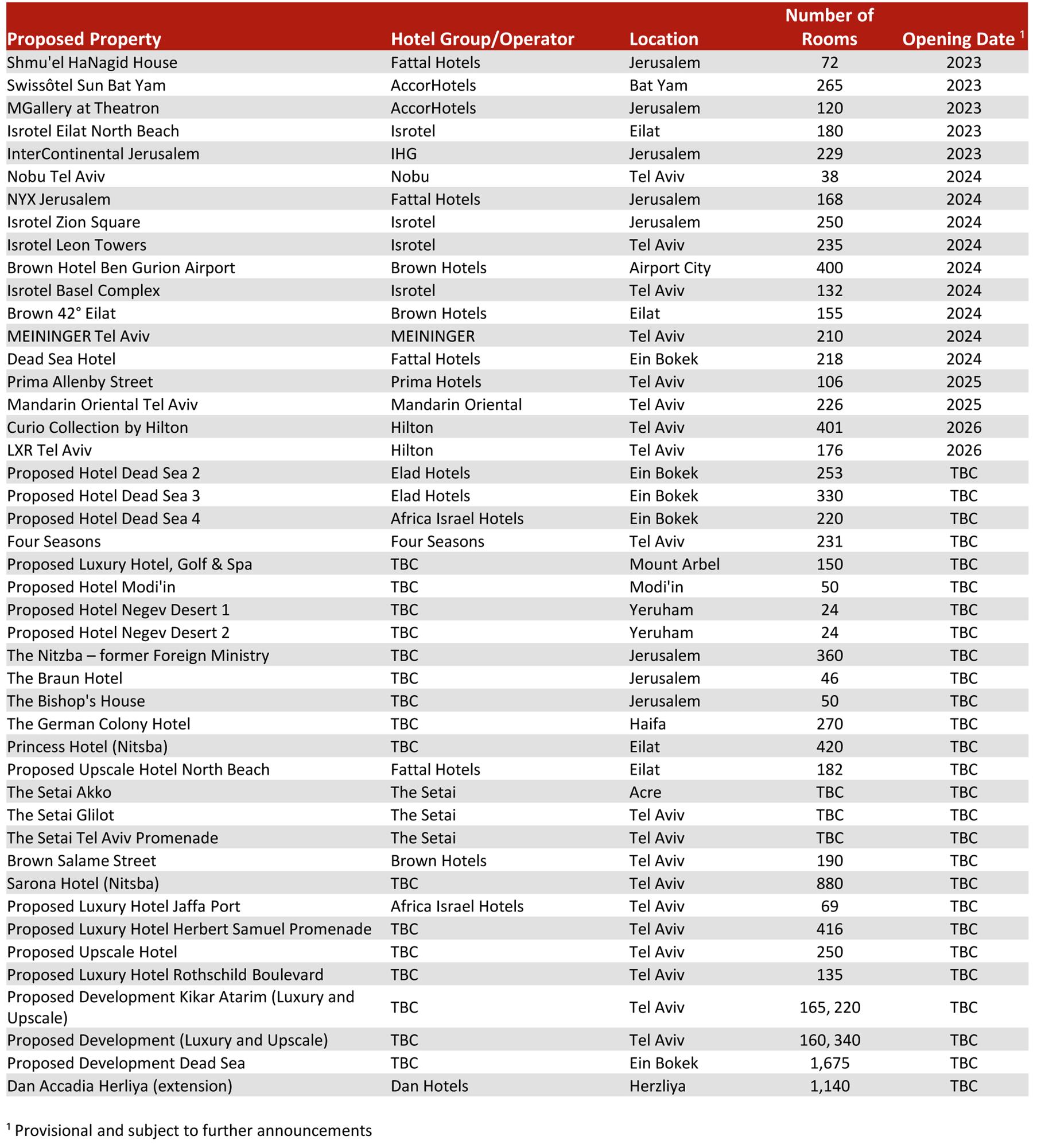

Figure 9: New Supply (continued)

Source: HVS Research

Hotel Values and Investment

Hotel Value Recovery to Accelerate

Prior to the pandemic, our indications for changes in average hotel values across Israel evidenced an increase across most sub-markets since 2017, with 2019 proving to be a particularly strong year with growth recorded across all markets.

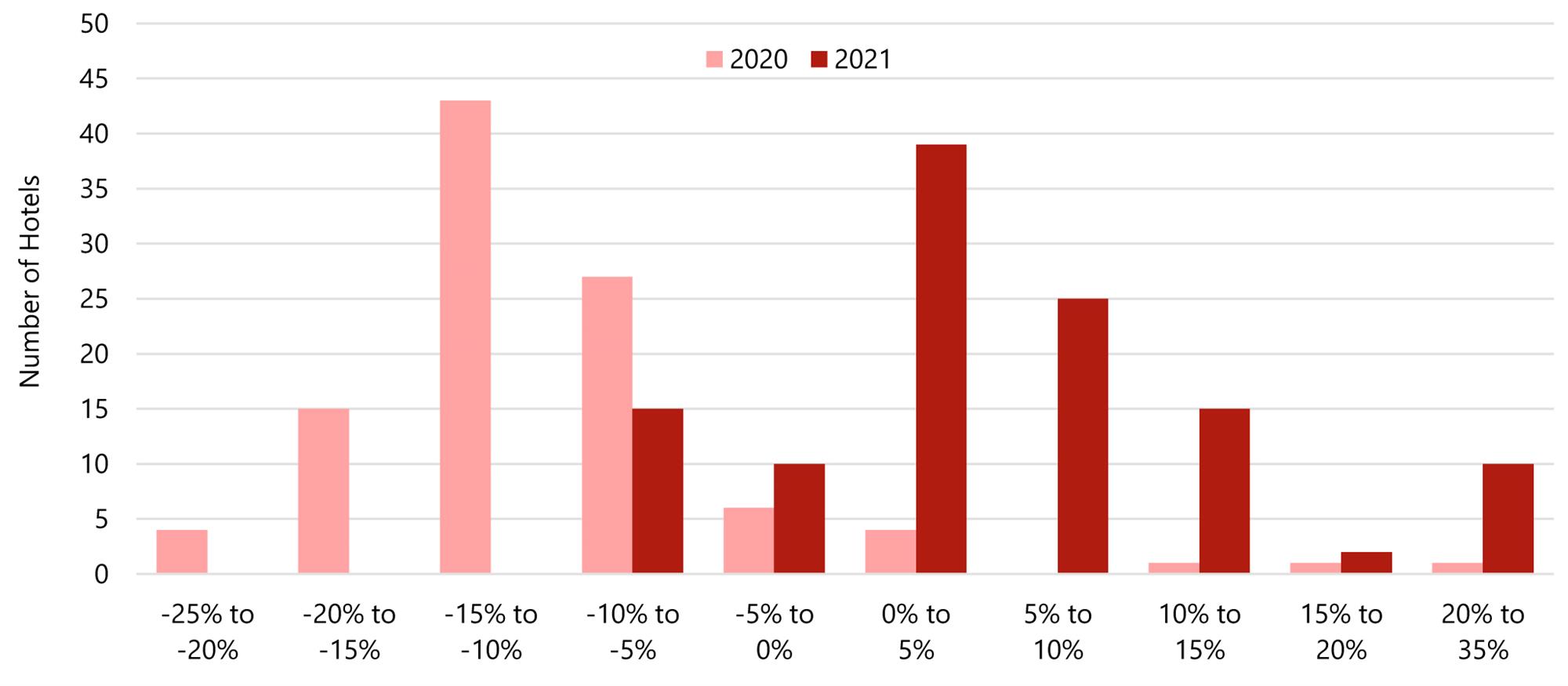

Unsurprisingly, in 2020 and 2021, plummeting occupancy, average rate and RevPAR impacted EBITDA, as owners and operators struggled with decisions regarding staffing, and whether to continue or suspend the hotel operation. Low EBITDA margins are expected for the next few years; however, this is only in the near term and assuming the property is positioned to resume normalised operations, there should be no other material impact on value. As illustrated in Figure 9, our experience of hotel values in Europe (based on 116 hotels which HVS valued both in 2020 and in 2021) shows that most hotels’ values increased by up to 10% in 2021. This compares favourably to the majority which declined by between 5% and 15% year-on-year in 2020. Hotel performance data for hotels in Israel suggest that hotel performance for some has bottomed out, implying that hotel EBITDA has nowhere to go but up and others should follow. Such performance improvements, combined with increasing optimism concerning the outlook for the sector, should enable the value of hotels in Israel to pick up in due course. (Please see our 2022 European Hotel Valuation Index for more detail on hotel value progression across Europe.)

Nevertheless, the discussion on value changes is dependent on the current investment landscape, projected performance and market characteristics, and also on property-specific factors such as the physical condition of an asset, its location and management competence. It is therefore also important to consider that the recovery of hotel values back to 2019 levels will heavily depend on the progression of COVID-19 restrictions, the ability for tourism to return and the ability of owners and operators to capitalise on pent-up demand – as well as how the current crisis in the Ukraine unfurls.

Figure 10: Percentage Change in European Hotel Values 2021 vs 2020 vs 2019 (based on a sample of 116 hotels)

Source: HVS Research

Conclusions

The Israel Hotel Market, much like any other, lost the larger share of its rooms revenue in 2020. The following year, 2021, enjoyed some recovery throughout several months, fuelled by returning leisure and transient demand stemming from an increase in the domestic ‘staycation’ trend.

While there has been some increased uncertainty throughout the last two years – specifically in regard to the most recent COVID-19 variant (Omicron), the labour market and cost inflationary pressures – the hospitality industry has proven to be resilient. Demand will return in the long run, albeit at a different pace for different markets, partly depending on the historical reliance and exposure to group and international demand.

The crisis seems to be becoming increasingly under control, and business and consumer confidence has been improving – albeit that this will need to be reassessed in light of the current crisis in the Ukraine. With a focus on bringing back international demand, through measures such as keeping its skies open, Israel should be able to aid the tourism industry’s recovery and return to levels of growth experienced pre-pandemic.

With an expected uplift in performance and the return of investor confidence, hotel values in Israel should have the worst behind them. Hoteliers need to focus on encouraging international travellers to return as well as retaining domestic visitors and putting the right strategies in place to keep costs in check. In return, full recovery should ensue.

Russian Invasion of Ukraine

The recent military invasion into Ukraine by Russia, which started on 24 February, is creating much uncertainty across Europe and globally, with no clear understanding of Putin’s further intentions. Many countries are heavily reliant on energy sources from Russia and, as sanctions by the western world are being implemented, there is an anticipation of rising energy costs and potential shortages. Further developments of this war in the heart of Europe are likely to have an economic impact across Europe and further afield. At the time of writing, it is still too early to quantify this impact with any degree of certainty, and our report only considers what was known at the time of writing. Further developments may adversely affect the operation of hotels in Israel and could ultimately have an impact on their value.