The COVID-19 pandemic has transformed the climate for hotel lending in Canada. At the start of the year, the hotel sector was preparing for a down cycle in 2020 because the market had been riding high for the past 11 years, since the end of the Great Recession in 2009. Nevertheless, cautious optimism was the general sentiment heading into the New Year—the national lodging market remained healthy, and RevPAR levels were at a record high at the beginning of 2020. No one was expecting a pandemic that would bring economic activity to a grinding halt and cause an unprecedented decline in lodging demand around the globe, but that is what the world received in March 2020. The widespread restrictions on travel, the cancellation of major events and conferences, and the implementation of social-distancing measures to slow the spread of COVID-19 caused the sudden evaporation of lodging demand, resulting in a substantial drop in hotel revenue and profitability that has put a chill on hotel lending across Canada.

In each year since 1993, HVS has tracked the hotel lending market by surveying hotel lenders active in the ten provinces and three territories of Canada. Our most recent survey in November 2020 is of particular importance because it captures current lender sentiments in this time of upheaval within the hotel sector. Instead of discussing the typical lending parametres, this year’s survey emphasizes on the effects of COVID-19 on hotel financing and lender’s responses to the pandemic. The focus of this survey will be on the following aspects: the availability of new loan origination, the types of borrower’s aid available, and the outlook on hotel value, foreclosure proceedings, and hotel interest rates as the pandemic takes course.

With the unprecedented changes in the industry, this year’s survey brings much-needed insight into the current lending environment and the overall health of the hotel finance sector in Canada.

Loan Originations are Expected to Dry Up

Loan origination is a key indicator of the general health of a market. Issuing loans is a way for lenders to enter or gain presence in a booming market or a market with opportunities. Conversely, lenders are more cautious in granting loans when market conditions are not ideal.

The economic fallout from the pandemic has restricted lending activity. Nonetheless, two types of lenders have shown a greater willingness to originate loans during the pandemic despite the unfavourable market conditions: lenders that are active in major markets where performance was healthy before COVID-19, and larger institutional lenders that issue loans across a greater geographic area. For the former group, this willingness is due to optimism that the formerly healthy hotel market will eventually recover to pre-COVID-19 levels. For large institutional lenders, the willingness to lend stems from a perceived opportunity to act bullishly and increase their presence in the hotel space. In contrast, regional lenders, especially those that are active in resource markets that have faced challenges since late 2014, have become even more prudent.

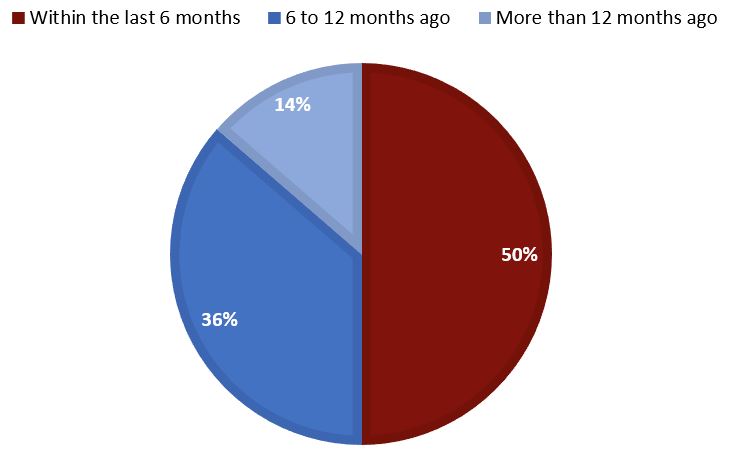

Compared to previous years when hotel financing was readily available for borrowers, loan origination has significantly decreased due to the pandemic. In our survey of lenders, 50% of respondents had originated a loan within the last six months, 36% had last originated a loan 6 to 12 months ago, and 14% had not originated a loan in the last year.

Figure 1: Time of Last Loan Origination

Since the recovery of the Canadian lodging industry is tied to the COVID-19 pandemic coming to an end, there is a high level of uncertainty in the hotel lending space at this time. Although half of the participating lenders originated loans when the COVID-19 pandemic was in full swing, lenders are generally taking a more cautious approach in loan origination moving forward. Most survey participants stated that their respective lending institutions are currently on pause and will be concerned solely with assessing their current loans and helping their existing clients. Additionally, some lenders are looking for ways to exit the hotel sector altogether. Notably, more than 77% responded that they will not be issuing new loans in the near term.

Nevertheless, select lenders perceive the current environment as an opportunity to continue growing in the hotel space, and they anticipate reaping the benefits as the sector recovers once again. For those lenders that are looking to expand, assets in primary markets with strong sponsorship are preferred.

Lenders are Offering COVID-19 Relief Programs to Support Borrowers

Many lenders have made accommodations to help their clients through this challenging time. For 95% of respondents, their lending institutions are offering lending support to borrowers to mitigate the impacts of COVID-19. Most lenders offer more than one type of borrower’s aid, particularly large institutions such as national banks and major credit unions, which are generally better positioned to offer a wider range of support services. The most common aid programs are interest-only payments and principal and interest holidays.

Figure 2: Types of Borrower's Aid Offered

.JPG)

Other types of relief include liquidity facilitation and co-lending applications. From the survey responses, the most commonly used co-lending support program is Export Development Canada’s Business Credit Availability Program (BCAP) Guarantee, which is a new term loan provided to private business owners to sustain operations in response to COVID-19. Additionally, 55% of lenders have advanced loans to cover operational losses.

Lenders will typically examine a list of criteria before granting support to a borrower. The survey results show that the most important prerequisite is that the borrower have an already established relationship with the lending institution. In terms of the duration of borrower’s support, 70% of respondents currently offer support for a 3- to 6-month period. Given the high level of uncertainty in the market, a short term period is preferred because it necessitates a frequent review of market conditions, allowing lenders to update their support programs in response to changes in the market.

.JPG) Source: HVS

Source: HVS

Figure 3: Lending Aid Prerequisites

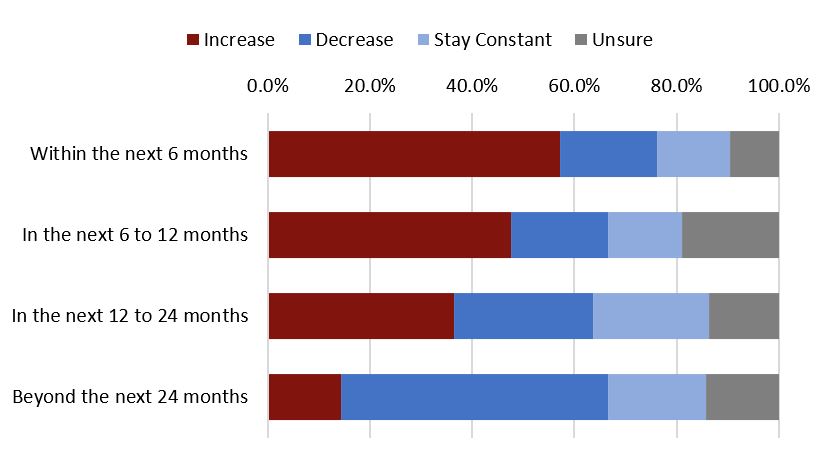

Internal Loan-To-Value on Hotel Books are Expected to Increase

The loan-to-value (LTV) ratio is a measure that lenders often examen when granting a loan. A high LTV is associated with greater risk for the lender, as it is an indication of leveraging less equity with more debt. Under normal circumstances, a lender’s LTV requirements will reflect its sentiment on a certain market, product type, or borrower. Lenders are more likely to grant a high LTV ratio to borrowers with a good track record and/or quality assets in promising hotel markets. Conversely, in periods of economic uncertainty and hardship, LTV requirement for borrowers would decrease to mitigate the risk of a loan default.

For this survey, however, we are not concerned with the LTV requirements for a borrower. Instead, we are considering the current level of outstanding debt in a lender’s hotel portfolio relative to the hotel values in that portfolio. LTV ratio could also be used as a metric for borrowers to understand the level or risk within their own hotel books. Given that loans are typically granted on 5-year terms, changes in the percentage of debt and equity relative to each other reflects a portfolio’s revenue-generating power and changes in value.

A large percentage of respondents expect to see an increase in the LTV ratio of their own hotel portfolio in the immediate future. As revenue-generating real estate, lodging establishments are valued based on their profitability and cashflows. With the severe impact of the COVID-19 pandemic on hotel performance, hotel assets in Canada have suffered a sharp decline in value. A decline in value like this increases the percentage of debt in a lender’s portfolio.

Nevertheless, as the pandemic recedes and travel restrictions are lifted, hotel income should slowly return to normal levels, resulting in an increase of hotel values. This is reflected in the survey responses: lenders generally expect LTV ratios in their hotel books to decrease over time.

Figure 4: Outlook on Internal Loan-To-Value (LTV)

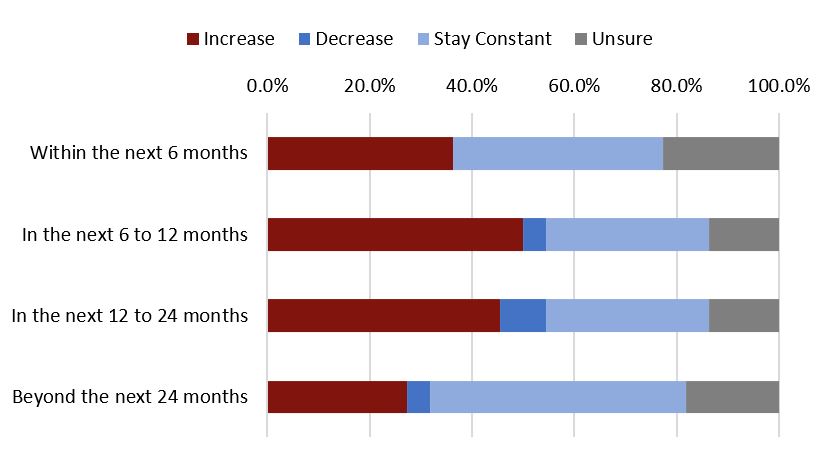

Foreclosures are Expected to Increase

With the persistence of travel restrictions, social-distancing mandates, and a general fear of travel, many hotels continue to operate with unsustainably low occupancy levels. These hotels face the serious problem of not generating a sufficient level of EBITDA Less Replacement Reserve or Net Operating Income (NOI) to service their debt obligations. Although lenders and government bodies are extending different types of support programs to hotel owners to keep properties afloat, true hotel profitability will ultimately depend on the successful rollout of a vaccine, the return of business and leisure travel, and the resumption of group gatherings. With relief programs likely to wind down in the near term, the number of hotel foreclosures and forced sales will increase. Without additional support, many owners will struggle to come up with the capital to make mortgage payments while their hotels fight to break even.

Many respondents are expecting an increase in distressed sales, particularly between 6 and 24 months from now. Hotels appear to be positioned for survival in the near term, but borrowers will run out of capital reserves as depressed market conditions persist. For hotel assets in resource markets that have already suffered for several years because of the oil and gas downturn, the challenge is even greater, because the low or even negative profitability from previous years means that capital reserves are already thin, making a distressed sale more likely.

A significant number of lenders actually expect the number of foreclosures to stay constant through the next two years. This sentiment could be from lenders that are active in markets that are prospering during pre-COVID times, as they may be confident that formerly well-performing hotel assets will be resilient enough to survive until the recovery takes hold. Alternatively, and less optimistically, this expectation could be from lenders that are active in resource markets in Alberta, the Prairies, and the Maritime provinces where hotel performance has been soft since 2015. Several foreclosures and distressed sales had already occurred in these markets before COVID-19. For these markets, the number of foreclosures staying constant would mean that foreclosures continue at the same steady pace.

Source: HVS

Source: HVS

Figure 5: Outlook on Foreclosure Proceedings

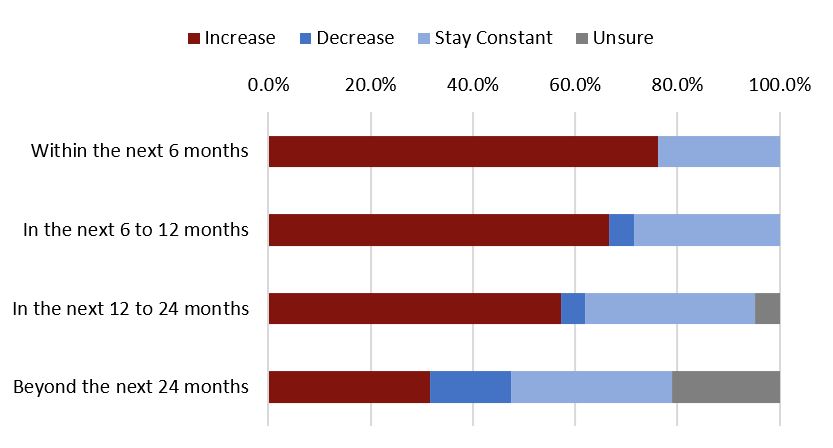

Interest Rates are Expected to Rise

The profitability of a hotel is determined by a multitude of factors. The competency of the management team, the branding, the condition of the property, the location, and overall economic conditions all contribute to a hotel’s revenue-generating potential. Also, unlike other commercial real estate classes, hotels have nightly leases, making this asset type more susceptible to volatility. Given the higher level of risk, hotels generally have an interest rate premium over other types of income-generating real estate assets.

Here, we are concerned with the anticipated trajectory of hotel interest rates, not actual interest rate levels. Given the pandemic-related contraction in demand, hotel investments are viewed as riskier in today’s environment compared to the risk sentiment of pre-COVID-19 times. Given this higher perception of risk, there is a fairly strong expectation that interest rates will rise. In our survey, 76% of respondents predict an increase in interest rates within the next 6 months, and 67% of respondents anticipate an increase in the next 6 to 12 months.

Source: HVS

Source: HVS

Figure 6: Outlook on Interest Rates

There Will Be a Chill On Hotel Lending Until The Pandemic Is Over

Lender sentiment toward the hotel sector is unfavourable at this time given the high level of uncertainty as to how the recovery of the hotel industry will unfold. Most hotel lenders expect only a minimal level of lending activity in the lodging sector over the next 24 months, until liquidity returns to the market. Nevertheless, lenders are exercising patience and, where possible, working to help hotel owners make it through the pandemic.

HVS regularly collects sentiments on hotel lending, as well as other aspects of the Canadian lodging market. If you are an industry professional in need of additional insight or assistance, we are happy to help. Please contact the HVS office nearest to you.