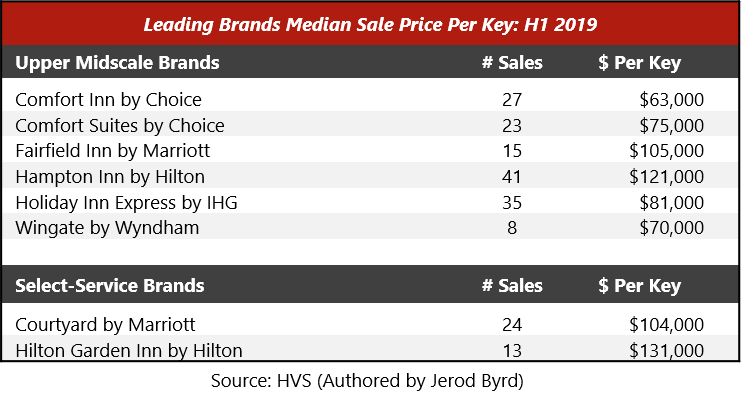

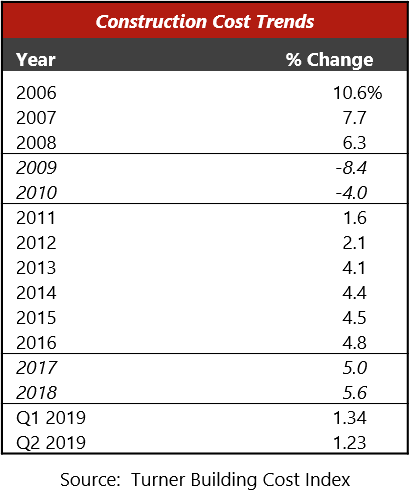

Despite a deceleration in demand growth, supply increases remain at around 2.0%, with Hilton and Marriott franchising roughly 58% of the overall new supply in the pipeline, with the remaining of the “Big 6” (Choice, IHG, Wyndham, and Hyatt, according to STR) at 25%. Construction costs have continued to climb over the years, with an average annual increase of 5.0% since 2015; the increase is a primary contributor to the constrained supply growth, which may not necessarily be a bad thing considering hotel metrics are stabilizing. From a sales perspective, Marriott and Hilton led the median price per key among the more popular upper-midscale brands for the first half of 2019; the select-service flags were also analyzed, but limited sales comparable data for the first six months of 2019 were available for flags such as Hyatt Place and Hotel Indigo, among others, to formulate a credible comparison to the more widely sold Courtyard by Marriott and Hilton Garden Inn hotels.

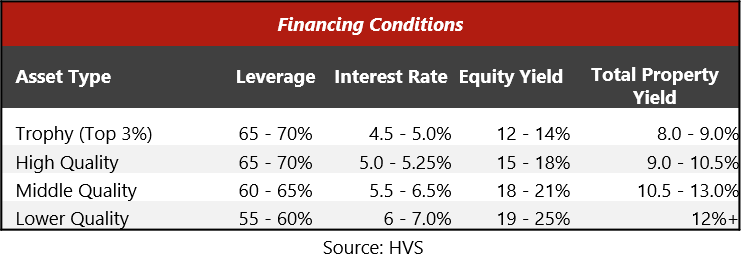

The lending appetite for hotels continues to remain strong, although transaction activity was down through the first half of 2019 because of waning RevPAR growth; the decelerating growth, in conjunction with rising labor costs, should result in hotel values remaining generally stable through 2020. For the near term, hotel owners should assume value appreciation to come in the form of asset operating efficiencies and not necessarily from market growth.

Investment Opportunities

HVS Americas re-launched its Brokerage and Advisory division in 2018. View our current listings.Contact Rod Clough, MAI if you are interested.