Much has been said and written about the negativity around stressed hotel assets and delinquent term loans for the hospitality sector in India. Hindsight has made developers reduce exposure to hotels as an investment class while lenders are careful to the point of being comatose. But what about existing hotel investors who have already weathered the turmoil of construction and now have operating hotels with delinquency? This article suggests ways in which re-financing of existing debt can help an investor manage the systemic issues of hotel debt-capital structure in India.

• Supply glut – Over the last ten years, branded hotel supply in India grew from 39,285 rooms in 2006/07 to 1,13,622 rooms in 2015/16; at a CAGR of 12.5%;

• Weak demand patterns – For the same period, RevPAR saw a de-growth from Rs.5,049 in 2006/07 to Rs.3,512 in 2015/16; at a CAGR of -3.95%;

• Project cost overruns – while the first two are macro factors, there are a significant number of loans that have turned bad because of internal issues like inadequate planning and inefficient project execution, leading to project delays and cost overruns.

• Business risk has replaced construction risk;

• Muted supply growth in most markets;

• Perceived upcycle for hotel industry.

Essentially, what this means is that selected lenders do share the general optimism surrounding hotels in India and are willing to listen to your point of view and win your business.

• It is a standard loan on the books of the bank;

• 50% or more of the loan has been taken over by a new financial institution;

• The repayment period is in congruence with the project life cycle.

Clearly, this means that the promoter/ borrower must approach a new bank to refinance the transaction and the existing lender cannot be of much assistance.

• Funds could be used for general corporate purposes, as permitted by the lender;

• There might be bullet payments due and the hotel might not have sufficient cash flows to honour those;

• The borrower might be looking for a cash-out refinance to free up some funds for repair or renovation.

The key is to put together a case which presents to the lender a transaction with high financial potential and relatively lower investment risk.

Tenure: 15 years

ROI = Prime Lending Rate (PLR) + Applicable Spread

ROI = 10.0% + 3.5% = 13.5%

If we assume that the hotel became operational in 2015 and the PLR also dropped to 9.0%, the new RoI would be set to 12.5%. The borrower requests the existing lender to reduce the RoI by lowering the spread. On being denied that advantage, the borrower may approach another bank which might be more than willing to refinance the loan at PLR + 2.0%, i.e. at 11.0%.

.png)

A stable hotel is a superior candidate for refinancing loans for a longer tenure. The dynamics of lending to an operational hotel are different because of its proven track record, which in turn reduces the risk outlook and makes the entire refinancing exercise possible. A twelve-to-fifteen-year refinance programme along with an additional disbursement (at higher LTV) can be procured at a reasonable rate of interest. This exercise may provide huge relief to the promoters who are not keen to infuse more equity to service shortfall in repayment.

The following exhibit illustrates two scenarios for a 300-room hotel. This is the actual example of a refinance assignment recently undertaken by us. In the first case, the hotel may service the debt for the balance five years (from the original ten-year sanction) but, with a gross deficit of INR 176 crore, would need equity infusion by the promoter. In the second case, the promoter opted for a refinancing scenario with a longer tenure (15 years). We have illustrated the impact of this exercise without changing RoI or any key commercial term. Though the net outflow is higher to the bank, it frees up equity for the promoter and makes the asset debt-free in a reasonable time frame.

Existing relationships with banks are a huge support system. Yet your regular banking network with years of relationships might be falling short of your expectations. They may be unable to lend enough or offer satisfactory terms. At the same time, many hotel projects are vying for the attention of a few willing lenders. In this rather unique credit market, three factors are essential to get ahead in the queue:

• A worthy project with rational cash flow projections;

• Excellent relationship with banks, based on mutual respect;

• High quality data presented proficiently.

We believe that hotel development and acquisition financing needs specialised solutions and good projects certainly benefit from expert guidance. Over the next two years, we anticipate laws related to bankruptcy getting strengthened to penalise the laggards. If you are still deciding on the ‘hows’ and ‘whens’ of refinancing your existing loans, you are leaving money on the table and also treading on thin ice.

The Imperfect Past

Hotels today are associated with unmanageable levels of debt, often leading to an NPA (non-performing asset) classification. The following causes stand out:• Supply glut – Over the last ten years, branded hotel supply in India grew from 39,285 rooms in 2006/07 to 1,13,622 rooms in 2015/16; at a CAGR of 12.5%;

• Weak demand patterns – For the same period, RevPAR saw a de-growth from Rs.5,049 in 2006/07 to Rs.3,512 in 2015/16; at a CAGR of -3.95%;

• Project cost overruns – while the first two are macro factors, there are a significant number of loans that have turned bad because of internal issues like inadequate planning and inefficient project execution, leading to project delays and cost overruns.

The Future: A Perfect Antidote

Increased scrutiny and tighter lending norms have brought the focus to merit-based lending for hotel projects. Our interaction with investors and lenders that are currently active in the hospitality space points to the following factors fueling their interest:• Business risk has replaced construction risk;

• Muted supply growth in most markets;

• Perceived upcycle for hotel industry.

Essentially, what this means is that selected lenders do share the general optimism surrounding hotels in India and are willing to listen to your point of view and win your business.

Why Should One Refinance Existing Loans?

Simply put, refinancing can help correct the dichotomy of financing a high capital, high gestation business (like hotels) with a short loan term. The refinancing exercise can improve cash flows and push back the cost of capital as well as principal repayment to a time when the business has stabilised. It can also free up valuable equity for investors who want to deploy funds into other uses rather than filling up the gap in debt service.I. To claim benefits without re-structuring:

According to the circular released by RBI in 2014 on ‘Framework for Revitalising Distressed Assets in the Economy - Refinancing of Project Loans, Sale of NPA and Other Regulatory Measures’, the holder of an existing loan can apply for seeking a longer repayment tenure with certain caveats. However, the exercise will be termed as refinancing and not as a restructuring exercise only if:• It is a standard loan on the books of the bank;

• 50% or more of the loan has been taken over by a new financial institution;

• The repayment period is in congruence with the project life cycle.

Clearly, this means that the promoter/ borrower must approach a new bank to refinance the transaction and the existing lender cannot be of much assistance.

II. For additional leveraging of assets:

As explained above, reduced risk on existing hotel brings in additional bargaining power for the borrower. Based on the payment history, the borrower can enhance her/his existing loan. The reasons to seek this additional leveraging might be numerous:• Funds could be used for general corporate purposes, as permitted by the lender;

• There might be bullet payments due and the hotel might not have sufficient cash flows to honour those;

• The borrower might be looking for a cash-out refinance to free up some funds for repair or renovation.

The key is to put together a case which presents to the lender a transaction with high financial potential and relatively lower investment risk.

III. For reduction in the cost of borrowing:

The existing lender may not be willing to reduce the Rate of Interest (RoI) by lowering the spread on the Prime Lending Rate (PLR). However, another lender might value the diminished risk on the asset and offer a reduced RoI.Case Study

A project loan was sanctioned in the year 2012 on the following basis:Tenure: 15 years

ROI = Prime Lending Rate (PLR) + Applicable Spread

ROI = 10.0% + 3.5% = 13.5%

If we assume that the hotel became operational in 2015 and the PLR also dropped to 9.0%, the new RoI would be set to 12.5%. The borrower requests the existing lender to reduce the RoI by lowering the spread. On being denied that advantage, the borrower may approach another bank which might be more than willing to refinance the loan at PLR + 2.0%, i.e. at 11.0%.

IV. For increasing the loan tenure:

A stabilised hotel with consistent cash-flows may also be in the risk of defaulting on existing loan repayment. The key issue here is the relatively shorter amortisation tenure for an industry that is characterised by high capital stock and the cyclicality of business. Hotels in India have historically seen a door-to-door lending period of 10-12 years. Of this time period, 30% is typically spent in construction and another 30% in the ramping-up phase. A balance of 5-6 years is just not sufficient for interest and principal repayment.A stable hotel is a superior candidate for refinancing loans for a longer tenure. The dynamics of lending to an operational hotel are different because of its proven track record, which in turn reduces the risk outlook and makes the entire refinancing exercise possible. A twelve-to-fifteen-year refinance programme along with an additional disbursement (at higher LTV) can be procured at a reasonable rate of interest. This exercise may provide huge relief to the promoters who are not keen to infuse more equity to service shortfall in repayment.

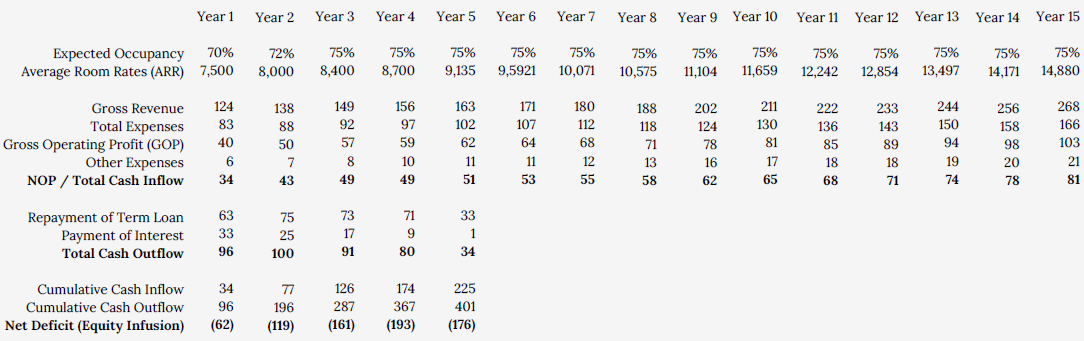

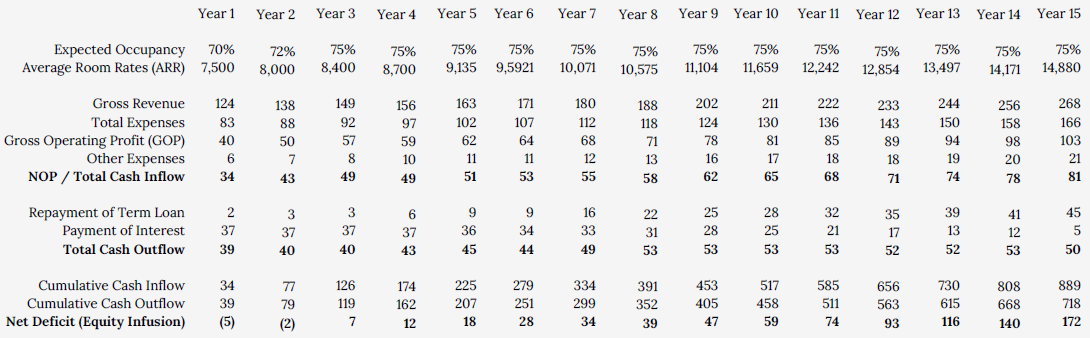

The following exhibit illustrates two scenarios for a 300-room hotel. This is the actual example of a refinance assignment recently undertaken by us. In the first case, the hotel may service the debt for the balance five years (from the original ten-year sanction) but, with a gross deficit of INR 176 crore, would need equity infusion by the promoter. In the second case, the promoter opted for a refinancing scenario with a longer tenure (15 years). We have illustrated the impact of this exercise without changing RoI or any key commercial term. Though the net outflow is higher to the bank, it frees up equity for the promoter and makes the asset debt-free in a reasonable time frame.

Scenario 1: Revenue Projections As Per Existing Repayment Schedule (in INR cr.)

Original Term - 10 Years

Balance Term - 5 Years

Scenario 2: Revenue Projections As Per Revised Repayment Schedule (in INR cr.)

Tenure for Refinance - 15 Years

V. Changes in the scope or specification of the project:

There are cases when, after receiving debt capital, the scale or quality of the hotel project had to be altered. Clearly, a higher project cost will most often necessitate a larger debt capital outlay. In most cases, existing lenders are averse to enhancing loan amounts and, therefore, the need to approach a new lender for take-over and enhancement of the loan amount.Existing relationships with banks are a huge support system. Yet your regular banking network with years of relationships might be falling short of your expectations. They may be unable to lend enough or offer satisfactory terms. At the same time, many hotel projects are vying for the attention of a few willing lenders. In this rather unique credit market, three factors are essential to get ahead in the queue:

• A worthy project with rational cash flow projections;

• Excellent relationship with banks, based on mutual respect;

• High quality data presented proficiently.

We believe that hotel development and acquisition financing needs specialised solutions and good projects certainly benefit from expert guidance. Over the next two years, we anticipate laws related to bankruptcy getting strengthened to penalise the laggards. If you are still deciding on the ‘hows’ and ‘whens’ of refinancing your existing loans, you are leaving money on the table and also treading on thin ice.

0 Comments

Success

It will be displayed once approved by an administrator.

Thank you.

Error