Philadelphia’s remarkable place in U.S. history dates back to 1682, when English entrepreneur William Penn founded the province that would come to be known as the “City of Brotherly Love.” A century later, delegates from 13 colonies convened in Philadelphia for a series of congresses that would ultimately lead to the Declaration of Independence and the U.S. Constitution. Today, known as a seat of commerce, education, and culture, Philadelphia is the second-largest city on the East Coast and the sixth-largest metropolitan area in the U.S. Philadelphia’s hotel industry has realized improvement in the years since the recent recession and appears to be heading in a positive direction over the next several years.

Economy Update

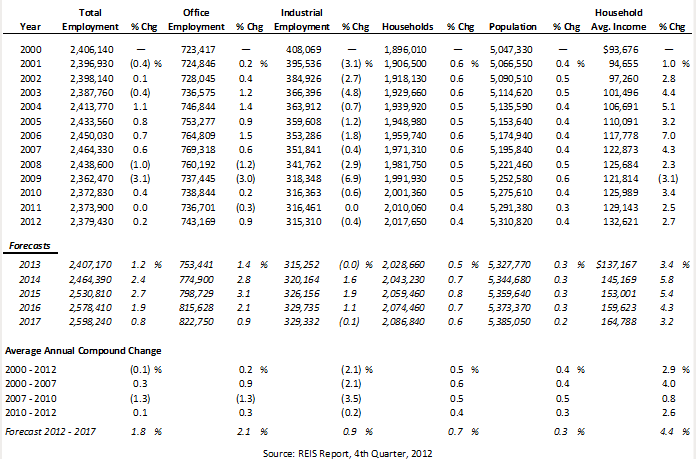

The following table illustrates historical and projected employment, population, and income data for the overall Philadelphia market.

HISTORICAL & PROJECTED EMPLOYMENT, HOUSEHOLDS, POPULATION,

AND HOUSEHOLD INCOME STATISTICS

For the Philadelphia market, of the roughly 2,400,000 persons employed, 31% work in offices and are categorized as office employees, while 13% are categorized as industrial employees. Total employment decreased by an average annual compound rate of -1.3% during the recession of 2007 to 2010, followed by an improvement of 0.1% from 2010 to 2012. By comparison, office employment reflected compound change rates of -1.3% and 0.3% during the same respective periods. Total employment is expected to expand by 1.2% in 2013, while office employment is forecast to expand by 1.4% in 2013. Forecasts for the 2012 through 2017 period anticipate total employment will improve at an average annual compound rate of 1.8%, and office employment is forecast to improve by 2.1% on average annually during the same time frame.

The number of households is forecast to improve by 0.7% on average annually between 2012 and 2017. Population is forecast to expand during this same period at an average annual compounded rate of 0.3%. Household average income is forecast to grow by 4.4% on average annually between 2012 and 2017.

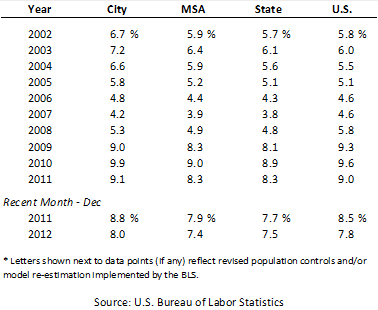

The following table illustrates unemployment statistics for Philadelphia, the MSA, the state of Pennsylvania, and the U.S. from 2002 to 2011.

UNEMPLOYMENT STATISTICS

The economic base of Philadelphia is largely supported by the education and healthcare sectors. The School District of Philadelphia is the area's largest employer, and the University of Pennsylvania has an undergraduate body of nearly 10,000 students from around the nation and the globe. Admissions are among the most rigorous in the country, and the university consistently ranks among the top-ten nationwide in the annual U.S. News & World Report survey.

The healthcare industry also serves as a major economic force and hotel demand generator for Philadelphia. In 1995, Thomas Jefferson University and the Main Line Health System signed an agreement establishing a new non-profit entity known as the Jefferson Health System (JHS). Since then, other established networks have joined JHS as founding members, including the Einstein Healthcare Network, Frankford Health Care Systems, and Magee Rehabilitation Hospital. Other healthcare cornerstones include the University of Pennsylvania Health System, the Children's Hospital of Philadelphia, and Independence Blue Cross, which is the region’s largest health insurer. The breadth of economic anchors in Philadelphia and the city's growing population are expected to bolster the area's economy and buoy its rebound from the recent downturn.

Office Space Market Update

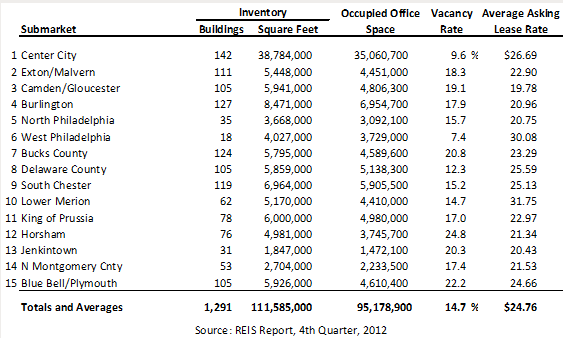

The following table illustrates office space statistics across Philadelphia’s major submarkets; these statistics are among the best indicators of a market’s propensity to attract commercial hotel demand.

OFFICE SPACE STATISTICS – MARKET OVERVIEW

The greater Philadelphia market comprises a total of 111.6 million square feet of office space. For the fourth quarter of 2012, the market reported an average vacancy rate of 14.7% and an average asking rent of $24.76. Vacancy rates in the submarkets of Center City and West Philadelphia fell well below the market-wide average; average asking rents in these two submarkets were also higher than the average asking lease rates of the other Philadelphia submarkets, aside from Lower Merion.

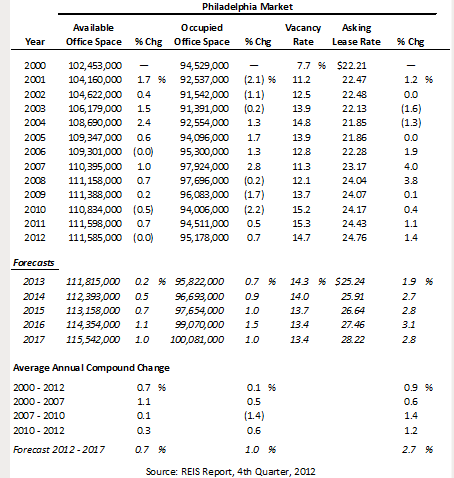

The following table illustrates historical and projected office space statistics for the overall Philadelphia market.

HISTORICAL AND PROJECTED OFFICE SPACE STATISTICS – GREATER MARKET

The inventory of office space in the Philadelphia market increased at an average annual compound rate of 0.7% from 2000 through 2012, while occupied office space remained relatively stable at an average annual rate of 0.1% over the same period. During the period of 2000 through 2007, occupied office space expanded at an average annual compound rate of 0.5%. From 2007 through 2010, occupied office space contracted at an average annual compound rate of -1.4%, reflecting the impact of the recession. The onset of the recovery is evident in the 0.6% average annual change in occupied office space from 2010 to 2012. From 2012 through 2017, the inventory of occupied office space is forecast to increase at an average annual compound rate of 1.0%, with available office space expected to increase 0.7%; this would result in an anticipated vacancy rate of 13.4% as of 2017.

Hotel Construction Update

HVS research revealed nine new hotels in the pipeline for the Philadelphia market:

- W Hotel

- Element by Westin Hotel

- Marriott Hotel at the Navy Yard

- Homewood Suites University City Philadelphia

- Homewood Suites at Liberty Plaza

- Home2 Suites by Hilton

- Xfinity Live Hotel

- Franklin Place

- Hotel Monaco

The addition of the hotels listed above, as well as several other hotel projects now in the early stages of development in the greater Philadelphia market, should have only a minimal impact on the area’s overall supply.

Outlook on Market Occupancy and Average Rate

Occupancy levels in the Philadelphia region are anticipated to strengthen moderately going forward, reflecting levels similar to pre-recession numbers over the course of the next several years as demand outpaces the additional room supply. Average rate is also forecast to strengthen year-over-year as hoteliers are continuing to renegotiate rates with corporate accounts; rates for groups and leisure visitors should also realize increases as the local and national economies continue to recover.

Conclusion

RevPAR levels for Philadelphia hotels should strengthen in the near term, particularly as existing hotels continue to drive room rate. HVS expects RevPAR to achieve a level around 5.0% over the course of the next two years, but then moderately drop off as economic conditions begin to normalize. The strengthening of Philadelphia’s diverse businesses and demand base, coupled with its historical significance and an array of attractions, should allow for continued growth going forward.