Fort Worth, Texas, the western anchor city of the Dallas/Fort Worth Metroplex, offers one of the most diverse metropolitan landscapes in the West. The city extends from skyscraping commercial office buildings to renovated historic districts such as the Fort Worth Stockyards National Historic District and Sundance Square. Fort Worth has grown from a dusty town along the famed Chisholm Trail to the nation's sixteenth-largest city and the fifth-largest city in Texas, with an economy that ranges across the services, trade, manufacturing, transportation, communication, and construction industries.

In addition to several cities located outside the western half of Interstate Loop 820, the Mid-Cities area occupies a large share of the greater Fort Worth market, including the cities of Arlington, Grapevine, Southlake, Colleyville, HEB (Hurst, Euless, and Bedford), NRH (North Richland Hills and Richland Hills), Haltom City, Watauga, and Keller, as well as smaller towns such as Trophy Club and Roanoke.

Economy Update

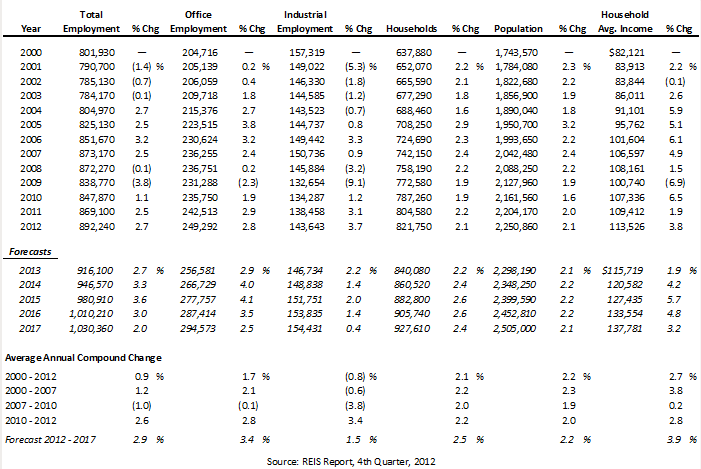

The following table illustrates historical and projected employment, population, and income data for the overall Fort Worth market.

HISTORICAL & PROJECTED EMPLOYMENT, HOUSEHOLDS,

POPULATION, AND HOUSEHOLD INCOME STATISTICS

The greater Fort Worth area workforce grew by 23,140 between 2011 and 2012, a 2.7% increase from the prior year and the third consecutive year of growth following the economic recession of 2009.

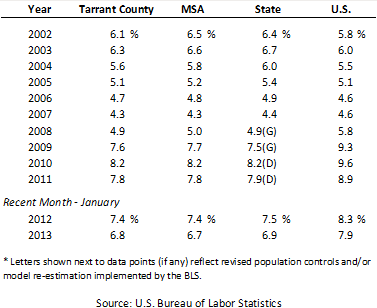

The following table illustrates unemployment statistics for Tarrant County, the MSA, the state of Texas, and the U.S. from 2002 to 2011.

UNEMPLOYMENT STATISTICS

Unemployment in the Fort Worth area began to rise in 2008, concurrent with the national economic slowdown, and continued rising through 2010; however, an improvement in the unemployment rate was realized in 2011. As of January of 2013, the unemployment rate for Tarrant County registered 6.8%, compared with 7.9% for the nation. Nearly 24,000 new jobs are forecast for 2013, with stronger growth anticipated for 2014 and 2015.

Fort Worth's diversity of businesses and revenue generators is contributing to the area’s economic rebound. AMR Corporation (parent company of American Airlines and American Eagle Airlines), Pier 1 Imports, RadioShack, Alcon, the BNSF Railway, and Lockheed Martin are some of the larger corporations based in Fort Worth; in addition, General Motors (GM) operates an assembly plant in Arlington. Fort Worth is also home to the Naval Air Station Fort Worth Joint Reserve Base. The Barnett Shale, a deposit of up to 30 trillion cubic feet of natural gas, is located in the Bend Arch-Fort Worth Basin, and energy exploration contributes heavily to the area's economy.

Major leisure demand generators in the area include Downtown Fort Worth, Fort Worth Stockyards, Will Rogers Memorial Center, Texas Motor Speedway, Six Flags Over Texas, Six Flags Hurricane Harbor, and the Grapevine Mills Mall. Events such as the Fort Worth Stock Show & Rodeo, the Main Street Fort Worth Arts Festival, Texas Christian University events, the Crowne Plaza Invitational at Colonial, Dallas Cowboys games and other events at Cowboys Stadium, and Texas Rangers games also prove major tourism draws throughout the year.

Although activity in the oil and gas industry continues to fluctuate with changing oil prices, the breadth of employers and companies in the Forth Worth area, as well as the city's growing reputation as a convention destination following the opening of the Omni Convention Center Hotel in January of 2009, should bolster the local economy and continue to fuel its rebound from the recent recession. The variety of tourism attractions and well-developed transportation infrastructure of the Dallas/Fort Worth Metroplex, including an international airport and a favorable interstate and highway system, should also contribute to the greater market's continued strength and expansion.

Office Space Market Update

The following table details Fort Worth’s office space statistics, which are important indicators of the market’s propensity to attract commercial hotel demand.

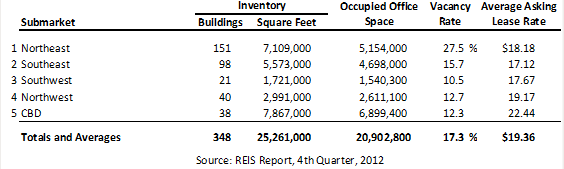

OFFICE SPACE STATISTICS – MARKET OVERVIEW

The change in office space occupancy levels in the greater Fort Worth market for the fourth quarter of 2012 varied greatly among the classes. Class A vacancy decreased roughly 70 basis points to 13.9%, while the Class B/C vacancy rate registered 21.1%, which represents an increase of approximately 90 basis points. Overall, occupancy among all classes remained relatively stagnant compared with occupancy in the previous quarter. Average rents increased minimally.

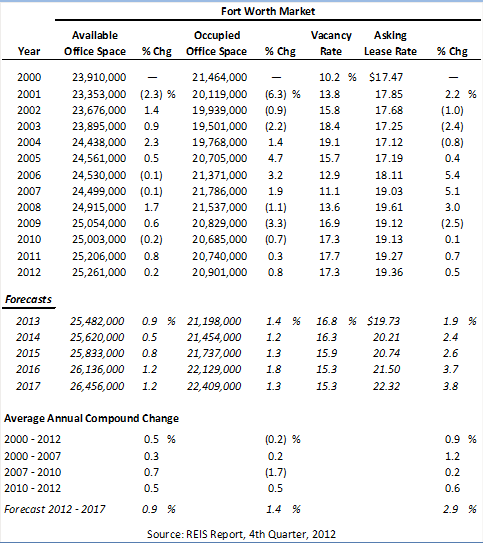

The following table illustrates a trend of office space statistics for the overall Fort Worth market.

HISTORICAL AND PROJECTED OFFICE SPACE STATISTICS – GREATER MARKET

The above-average asking lease within Fort Worth’s CBD reflects the desirability of this submarket. Notable office projects under construction in Downtown Fort Worth include two Class A buildings, the Westbrook and the Commerce Building; these projects are located in the popular Sundance Square and are scheduled to open by the end of 2013. Positive absorption is expected in the overall Fort Worth office market, but the addition of new supply will result in only a modest improvement in vacancy levels.

Hotel Construction Update

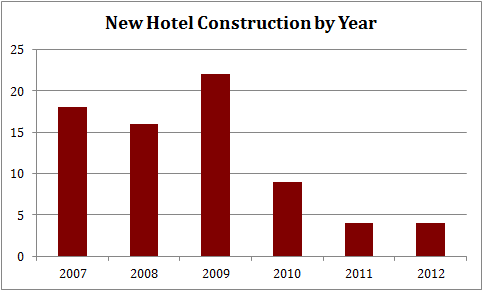

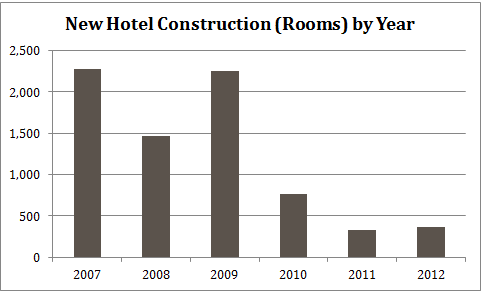

The economic boom in the years prior to the recent recession spurred significant hotel construction in the Fort Worth area. The following charts depict the new supply additions realized in the greater Fort Worth market from 2007 to 2012.

In 2007, the large increase in rooms was enhanced by the opening of the 605-unit Great Wolf Lodge in Grapevine, while the opening of the 619-unit Omni Fort Worth Hotel helped push the number of new rooms to just over 2,250 in 2009. Hotel projects with openings planned for 2008 and 2009 were already in the pipeline when the recession took hold, leading to significant supply increases in those years. Developers were also encouraged to move ahead with hotel projects in Fort Worth largely on the strength of the area’s economy and increased energy exploration activity; however, new construction was limited to fewer than ten properties in 2010, and fewer than five projects were recorded for both 2011 and 2012.

According to HVS research, three new hotels are under construction:

- A 122-unit Homewood Suites is under construction at 2200 Charlie Lane, within The Raymond Group’s Midtown mixed-use development. The hotel is expected to open in June of 2013 and will be located adjacent to the newly constructed Hilton Garden Inn Fort Worth Medical Center (opened April 2012).

- A dual-branded hotel development in Grapevine's Silver Lake Crossings will include a 180-unit Courtyard by Marriott and a 120-unit TownePlace Suites by Marriott. The project is estimated to open in the fall of 2013, and the developer is Newcrest Development.

Two hotel projects are currently proposed:

- A 210-unit Hampton Inn & Suites is proposed for 210 E. Ninth Street, at the site of the former United Way building. The Raymond Group is developing the project, which is expected to open in the fall of 2014; construction is likely to begin in late 2013.

- A 140-room Hyatt Place is a planned part of the WestBend mixed-use development located near the intersection of South University Drive and River Run, to the east of University Park Village. Commencement of construction and potential opening dates remain speculative at this time.

While lenders have somewhat loosened the reins on construction loans as the economy has improved, the pickup in hotel construction is expected to be modest in the near term, with a larger pipeline expected in 2014.

Outlook on Market Occupancy and Average Rate

The Fort Worth market appears to be trending similarly to the broader national patterns of economic recovery. HVS forecasts the lodging market in Fort Worth to realize modest increases in occupancies in 2013, with average rate growth of 1% to 2%. Occupancy increases are expected to continue in the near term and will be supported by demand growth associated with the area’s diverse economic mix, revamped and expanding downtown and entertainment areas in Fort Worth and surrounding cities, and the increased appeal of Fort Worth as a convention destination. Hoteliers are anticipated to focus on recovering room rates over the longer term, with occupancy taking precedence in the near term. Important development aspects influencing lodging trends in Fort Worth’s submarkets are as follows:

Downtown Fort Worth: One of the fastest growing parts of Fort Worth is the West Seventh Street corridor. This area has been transformed over the past five years, spurred by the redevelopment of Montgomery Plaza. The area includes new apartments, bars, restaurants, and retail outlets. Currently, the rebuilding of the West Seventh Street Bridge, which connects the Cultural District, is underway; the $24.1-million project is scheduled for completion by the end of 2013. In March of 2013, Centergy Retail of Dallas purchased a 30-acre plot; plans for the site are reported to include a mixed-use development featuring retail, residential, office, and hotel buildings.

Northeast: The LEGOLAND Discovery Center, a $12-million children's attraction, opened at Grapevine Mills in March of 2011, and the $15-million SEA LIFE aquarium opened in July of 2011. Great Wolf Lodge and the Gaylord Texan Resort & Convention Center are also popular attractions; the Gaylord unveiled a ten-acre water park in 2011. The $2.5-billion North Tarrant Express project, which will improve travel and connectivity in the Mid-Cities area, is underway and includes the significant redevelopment of Interstate 820 and the State Highway 121/183 corridor between Interstate 35W and Industrial Boulevard in North Tarrant County.

Northwest: In November of 2012, NGC Renewables finalized its purchase of 18.6 acres in the Alliance development in Fort Worth; NGC Renewables, a subsidiary of China-based NGC Transmission Equipment, makes wind turbine transmission equipment and plans to build a new North American headquarters.

Southwest: Texas Christian University’s (TCU) football stadium underwent a $164-million renovation project that was completed just before the 2012 season. A $45-million renovation project is expected at TCU’s Daniel-Meyer Coliseum.

Southeast: From restaurants and retail to cultural and entertainment activities, increased development in Downtown Arlington and at The University of Texas at Arlington has occurred in recent years. College Park District is a primary component of the redevelopment in Downtown Arlington and includes College Park (an $80-million residential and retail development) and a $78-million on-campus special events center named College Park Center. Retail developments have also flourished along the Interstate 20 corridor. The Arlington Highlands lifestyle center was completed in 2011; this 80-acre, mixed-use development houses over 800,000 square feet of office, retail, restaurant, and entertainment space. In addition, Traders Village Flea Market is located just east of Arlington in Grand Prairie and is the largest weekend flea market in Texas. Furthermore, Paragon Outlets in neighboring Grand Prairie opened in August of 2012 and features more than 100 leading retailers.

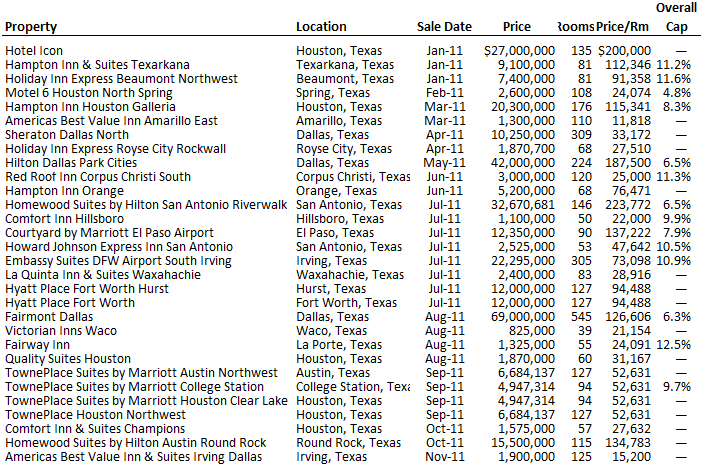

Recent Hotel Transactions

Hotel transactions that have occurred in the state since January 1, 2011, are summarized in the following table. Transactions within the Dallas/Fort Worth Metroplex are highlighted.

REVIEW OF HOTEL TRANSACTIONS

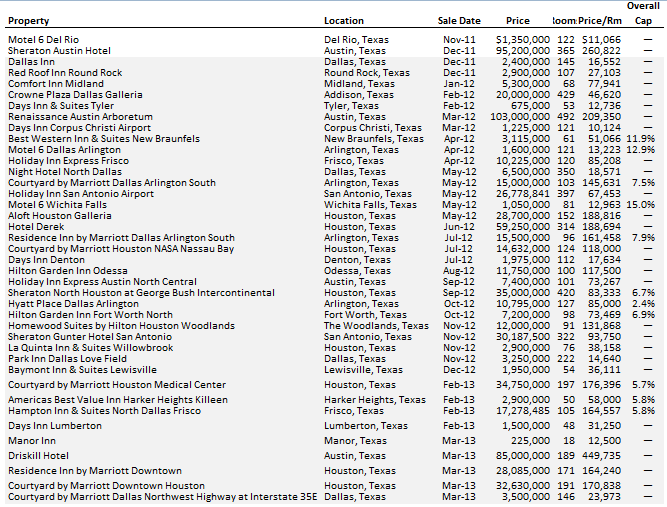

REVIEW OF HOTEL TRANSACTIONS - CONTINUED

The summary of hotel transactions illustrates a steady pace of deals during the last few years, across a variety of market segments and acquisition opportunities. The sales represent acquisitions of stabilized assets by institutional investors, as well as repositioning opportunities for entrepreneurial owner operators.

The summary of hotel transactions illustrates a steady pace of deals during the last few years, across a variety of market segments and acquisition opportunities. The sales represent acquisitions of stabilized assets by institutional investors, as well as repositioning opportunities for entrepreneurial owner operators.

Brokers’ Outlook

According to interviews with hotel brokers active in the Dallas/Fort Worth Metroplex, hotel transaction volume is likely to increase in 2013, albeit at a gradual pace. Transaction demand was centered on strongly flagged hotels throughout the first quarter of 2013. While the number of REIT purchases has seemed to slow, many individual buyers are looking to purchase assets at a price that allows them to take advantage of future growth in the market. Owners also want to take advantage of the upswing in revenues and need to decide on the right time to sell. According to several brokers, most potential buyers still struggle in finding a willing lender and closing a deal that satisfies both the buyer and the seller. As the banking sector continues to strengthen within the Metroplex and region, lending opportunities should continue to improve and the bid/ask gap should narrow. The emphasis on new development seems to be focused on mixed-use properties that feature retail, office, and multi-family residential components.

Conclusion

Fort Worth’s economy has strengthened and expanded in recent years, with growth stemming from the diversity of key drivers and industries in the market. Healthy improvements in hotel demand were realized in 2010 and 2011, and this growth outpaced supply additions, resulting in occupancy improvements for area hotels. Rate has been slower to recover, but hoteliers are anticipated to regain pricing power once occupancies approach prior peaks. A handful of hotel projects are planned to come online in 2013; however, demand is expected to continue to outpace supply additions, keeping Fort Worth’s lodging industry on a track toward full recovery in the near term.