Serviced apartments have become an increasingly prominent part of Europe’s accommodation landscape. Previously seen as a niche alternative to hotels, they are now drawing interest from both investors and developers. However, serviced apartments sit in-between the residential and hotel models, behaving differently to both. This is most apparent when comparing development costs, where the inclusion of kitchenettes and higher-specification FF&E sets serviced apartments apart from the typical hotel guest room, a distinction that is well understood by specialists but still often underestimated by newcomers to the sector.

In this year’s report, we look at these dynamics in more detail. Drawing on a dataset of around 13,000 units across Europe, we begin with a review of how the sector performed over the past year, before turning to the central question our survey respondents were asked to opine on: how do development costs for serviced apartments really compare to equivalent hotel schemes, and what does that mean for margins once the doors open?

Performance Review

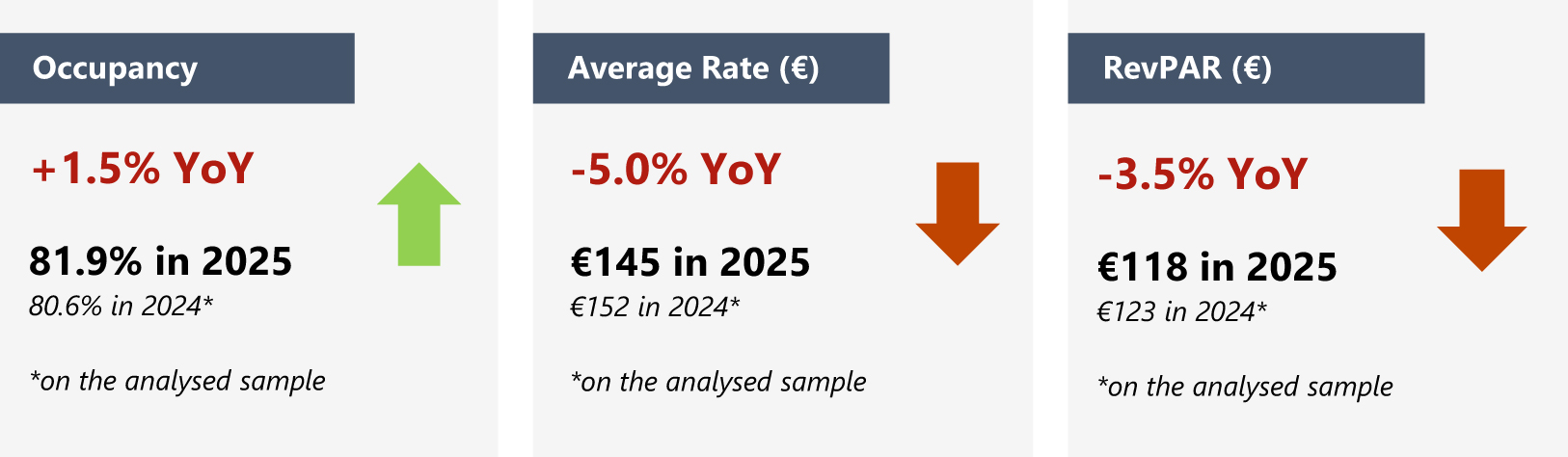

The responses to our Serviced Apartment Operators’ Survey point to a more subdued performance picture in 2025 than the broadly positive trends recorded a year earlier, with occupancy increasing modestly or remaining stable across most European locations and average rates softening almost universally. Occupancy remained steady, sitting at around 80% across all markets, while average rate softened, leading to an overall RevPAR decline.

Chart 1: 2025 Serviced Apartment Performance Led by Occupancy Rates (%)

Source: HVS Research

Serviced apartments’ performance across the UK varied greatly between London and the rest of the country, but with largely the same result. London properties built further on the momentum from the previous year, pushing occupancy up modestly, but average rates declined, a reversal of last year’s inflationary rate growth. Performance trends continued to vary regionally. Areas outside of London saw a sharper pull-back in occupancy, albeit with a comparatively more contained rate decline. These dynamics led to similar RevPAR declines in and outside of London.

In Paris, occupancy increased in 2025, as corporate demand recovered after the 2024 summer Olympics and Paralympics. However, average rates in the capital corrected sharply from the effect of the 2024 games. Areas outside of Paris saw occupancy plateau and this, coupled with a softening of average rates, led to a stronger RevPAR decline.

Cost per Key: Hotels vs Serviced Apartments

For our report this year, we surveyed several operators and chartered surveyors to gauge their impression on the central question of how serviced apartment development costs per key compare to equivalent hotel schemes, which produced a mixed response. At the upscale end, responses ranged from costs per key running 10-20% below a comparable full-service hotel to 10-20% above, depending on asset type and geography. At the midscale level the picture converges somewhat, with costs broadly comparable to a midscale select-service hotel in most scenarios, though with a moderate premium flagged in countries such as France. Others’ views ranged from similar costs to more than 20% above equivalent hotel developments, a spread that reflects genuine variation by asset type, conversion strategy, location and operator ambition rather than simple disagreement.

What the survey makes clear is that the direction of the cost differential depends heavily on context. Quantity surveyors noted that serviced apartments can show a clear cost advantage in office conversion schemes, particularly where the existing structure, grid, façade and core arrangement support efficient apartment layouts without major structural alteration. Conversely, heritage buildings, constrained floor plates and hotel-to-serviced-apartment conversions were cited as scenarios where costs can escalate materially. Older buildings with small floor footprints and smaller internal compartments were noted to incur considerable costs associated with structural alterations and adaptations to existing building services infrastructure, while existing high-end residential buildings were identified as among the easiest conversion candidates.

Regardless of the overall cost outcome, there is strong consensus across both surveys on where the cost complexity in serviced apartment development is concentrated. Kitchen and utility infrastructure emerged as the most frequently cited pressure point: the need to install kitchens at scale, with the associated drainage, ventilation, MEP uplift, acoustic separation and fire compartmentation, introduces a layer of in-unit complexity that has no direct equivalent in traditional hotel rooms. This is partially offset by the reduced public space that serviced apartments require relative to hotels, though that trade-off does not always balance cleanly, particularly in conversion projects where the structural envelope was not designed with these requirements in mind.

FF&E costs were consistently highlighted by multiple operators as a significant pressure, with several noting that the level of furnishing, fixtures, equipment and operational setup required to meet guest expectations can be higher than initially budgeted, including IT systems, access control, Wi-Fi infrastructure and back-of-the-house facilities. Planning permission and regulations were also flagged as challenges in particular countries such as France, where navigating the permitting process for serviced apartment projects is not straightforward and represents a source of noticeable cost disparity between the two product types.

Profitability

While the cost comparison with hotels is genuinely mixed, the margin story is more consistently favourable. GOP trajectories were broadly in line with or better than hotels over the past three years, and several operators reported outperforming hotels significantly. The underlying logic is that, although achieved room rates tend to run below those of comparable full-service hotels, the significant savings available on staffing and food and beverage operations mean that GOP margins can comfortably exceed those of equivalent hotel assets, in some cases by a meaningful margin. The ability to deliver a quality guest experience with a structurally leaner cost base represents the sector’s most compelling investment proposition.

The corollary, raised by several operators, is that competing on RevPAR against hotels is misconceived. Several cautioned against positioning serviced apartments simply as more space for less money, arguing that this framing understates the model’s broader value proposition. The aparthotel model’s operational rationale lies in its ability to increase average length of stay, thereby reducing the three largest cost drivers of operations: marketing, cleaning and staffing. An inherent tension was nonetheless identified: without the supporting facilities of a full-service hotel such as F&B, spa and concierge, it remains structurally difficult to command a rate premium over hotels, even where the product quality warrants one.

Pipeline

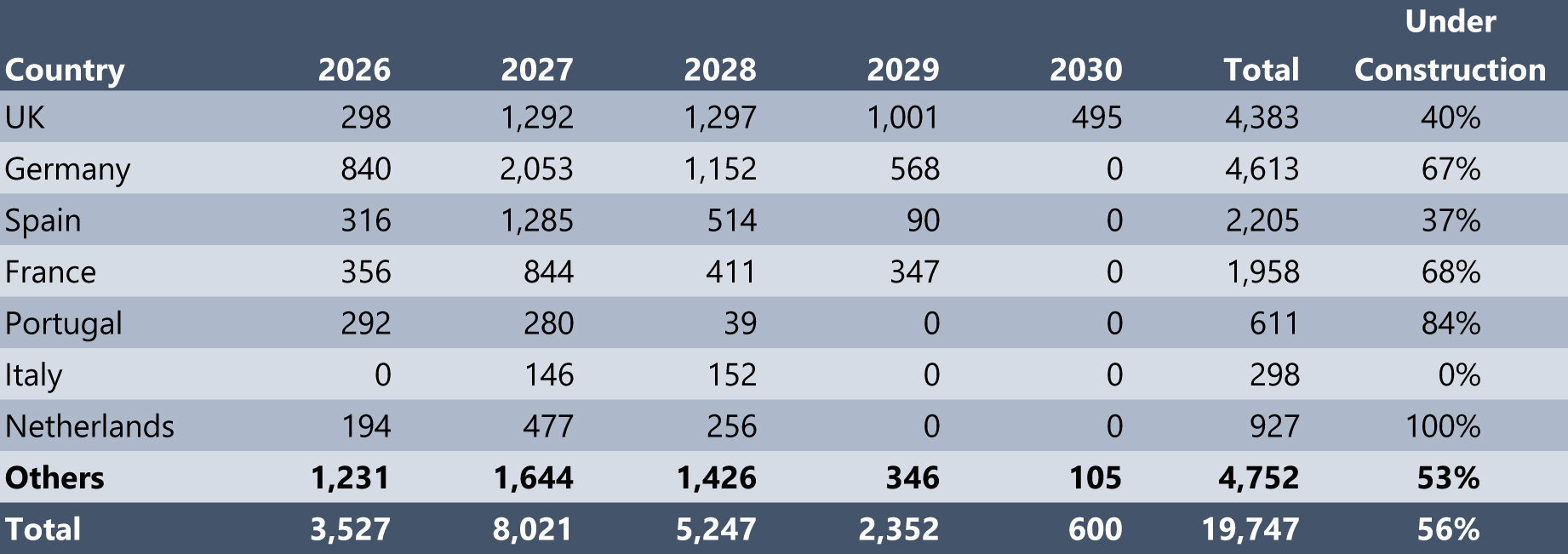

This report considers branded developments that have either been confirmed by the surveyed operators or announced publicly as at the end of June 2026.

Around 19,800 rooms are expected to enter operation in the next five years. Germany accounts for 23% of supply, followed by the UK with 22%. Unsurprisingly, the majority of activity in the UK is concentrated in London, which represents 57% of new supply within the country. In Germany, the new supply is mainly concentrated in Berlin, Munich and Hamburg.

Chart 2: European Branded Serviced Apartments Pipeline (Units)

Source: HVS Research

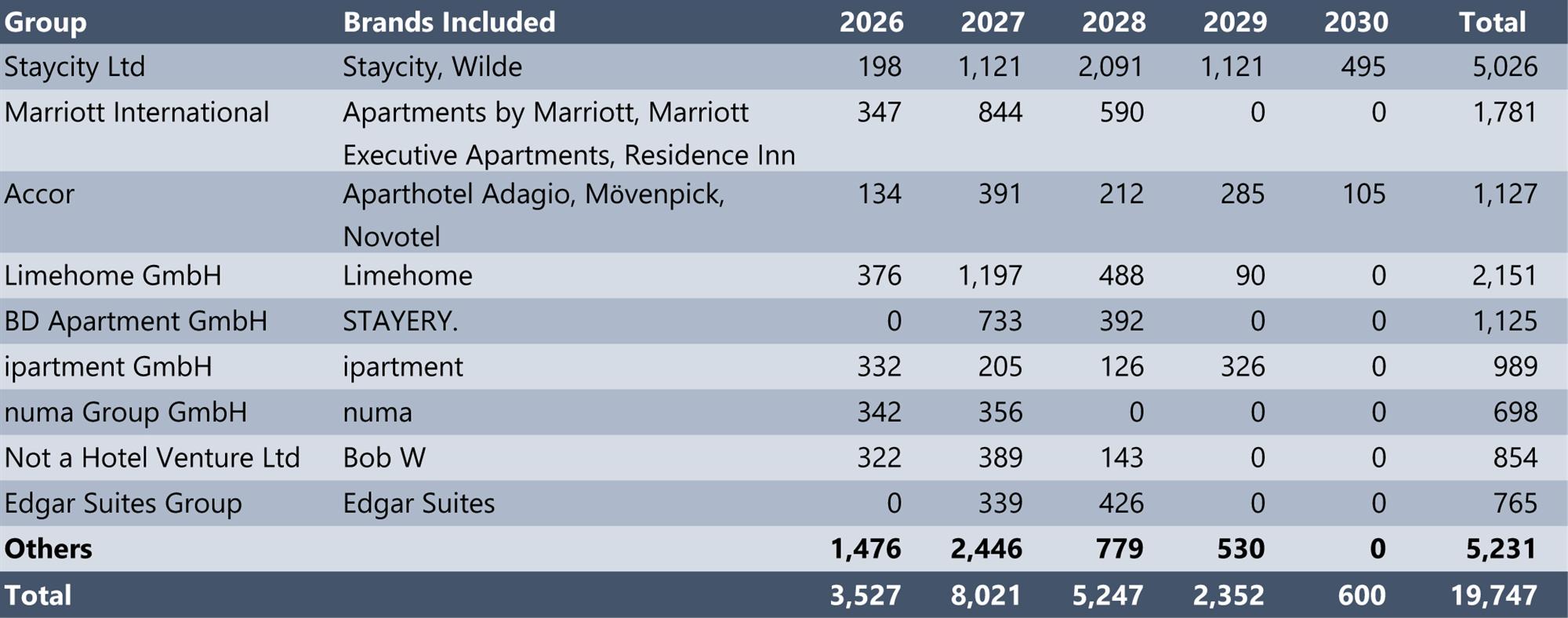

Of the new supply, according to our survey respondents, 25% of new units will be branded. Staycity Ltd has the largest pipeline with around 5,000 units expected to open over the next five years. 50% of the new Staycity developments will be located in the UK and a further 16% within Ireland; the remaining pipeline is spread across France, Italy, Spain, Germany, The Netherlands, Austria and Poland. Around 70% of these openings will be opened under the Wilde brand, with the remainder under the Staycity brand.

Limehome GmbH is the second most active group within the sector, with a 43-property pipeline comprising around 2,200 units. The group has a strong focus on Spain with more than 70% of its serviced apartments due to open in the country; Germany also has a number of openings from the brand.

Chart 3: Branded Serviced Apartments European Pipeline by Group (Units)

Source: HVS Research

Marriott International holds the third largest pipeline in Europe. The pipeline is concentrated across key European markets, with Residence Inn accounting for many openings, complemented by a smaller number of StudioRes, Apartments by Marriott Bonvoy and other extended-stay concepts.

Home2 Suites by Hilton is also continuing its European expansion. Following the brand’s first opening in Europe in Dublin in May 2026, a second property is planned for 2028: a 128-unit hotel is currently under construction at Schiphol Airport in Amsterdam.

The size of the aparthotels varies considerably, ranging from approximately ten units at several Limehome properties in Spain to 463 at the Wilde Aparthotel London Royal Mint. This wide variation in inventory demonstrates the flexibility of the serviced apartment model, which can be successfully adapted to a range of locations, demand profiles and investment strategies, from smaller conversion projects to large-scale purpose-built developments.

Transactions

Between July 2025 and June 2026, 12 serviced apartment transactions were recorded across Europe, comprising a total of approximately 900 units across seven markets with portfolio activity being a recurring theme during the period. In December 2025, CBRE Investment Management sold the 132-unit Staybridge Suites Liverpool and 128-unit Staybridge Suites Newcastle to ECE Work & Live (now ParkProperty Europe) and Maya Capital LLP. A similar dynamic played out in Finland in October 2025, when Aberdeen Property Income Trust and Ailon Group sold the 105-room Unity Helsinki and 148-room Unity Tampere to Brookfield AM and The Mesh Group GmbH, marking a notable entry by Brookfield into the European extended-stay market.

The UK and Spain were the most active markets in transactions recorded. UK transactions included the two Staybridge properties mentioned above and the 21-unit Beaufort House. In Spain, the highest price per key across the period was achieved by the March 2026 sale of the 21-unit Be Mate Paseo de Gracia in Barcelona. The transaction included two ground-floor retail units and is estimated to have cost AX Partners a total of €30 million for both the acquisition and refurbishment.

Chart 4: Number of Units Transacted in H2 2025 and H1 2026 per Country

Source: HVS Research

Conclusion

The picture that emerges from this year’s report is of a sector maturing in operational sophistication faster than gaining recognition from the broader investment market. Trading conditions in 2025 were softer than the previous year, with rate compression a near-universal feature across European markets, yet the underlying demand story remains structurally sound.

On development costs, the evidence points clearly to kitchen infrastructure, MEP uplift and FF&E as the primary drivers of complexity and costs, concentrated at the unit level rather than in public space, a trade-off that can favour the serviced apartment format in the right building type, and particularly in office conversion schemes. However, once operational, serviced apartments have the ability to generate margins that outperform comparable hotels through leaner operating structures creating a structural advantage.