Now, with renewed geopolitical tensions in the Middle East creating uncertainty for global travel, the local industry is once again maintaining a calm, business-as-usual approach. According to Wesgro, airlines such as Emirates and Qatar Airways account for around 10% of weekly flight capacity into Cape Town. While disruptions to these routes have raised concerns, other airlines are stepping in to help fill the gap:

- Lufthansa has added additional frequencies on its Frankfurt route;

- KLM is deploying larger aircraft, adding around 100 extra seats per flight; and

- Ethiopian Airlines has upgraded to larger aircraft, adding approximately 150 additional seats per flight.

- While these changes will not fully offset lost capacity, they will help ease pressure during peak travel periods.

Why Flights Matter More Than You Think

For a long-haul destination like Cape Town, flights are more than just transport, they are a critical enabler of the tourism economy. Without sufficient seat capacity, even strong travel demand cannot translate into increased visitor numbers or spending.That’s why initiatives like the Cape Town Air Access programme, led by Wesgro, play such a vital role. By securing new routes and increasing airline capacity, they continue to strengthen Cape Town’s position as a competitive global destination.

This momentum was further reinforced in April 2026 through a Memorandum of Understanding signed between Wesgro and Emirates focused on strengthening inbound tourism and air access into the Western Cape.

A Look Back: When Connectivity Constrained Growth

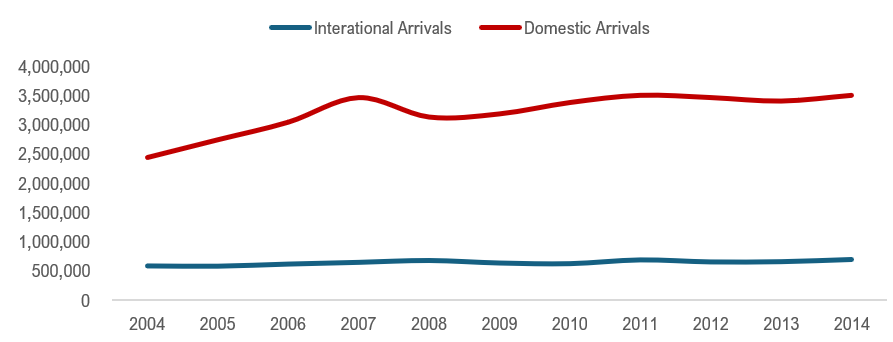

Historically, growth hasn’t always been smooth. Between 2004 and 2014, international arrivals into Cape Town International Airport (CTIA) remained relatively flat, with domestic travel driving much of the activity. A large proportion of international travellers accessed Cape Town via Johannesburg and were therefore captured within domestic passenger counts.Domestic and International Arrivals CTIA (2004 – 2014)

Source: Airports Company South Africa

Direct international air capacity to Cape Town was a key constraint. International flights were highly seasonal, with European carriers such as Virgin Atlantic, KLM, Air France and Lufthansa operating primarily during the European winter concentrating the bulk of international travel between November and March. Emirates and Qatar Airways were among the few airlines offering year-round services.

A major turning point came in 2012, when South African Airways reduced its direct international services to and from Cape Town. Combined with the lingering effects of the global financial crisis, this resulted in a 5% decline in international arrivals, reflected in a similar decline in overnight foreign visitors. Even the boost from the 2010 FIFA World Cup was not enough to sustain long-term growth.

Air Access - Unlocking Growth

Through a public–private partnership, the Cape Town Air Access Initiative (CTAA) was established to increase seat capacity and stimulate the tourism economy. A decade on - despite a severe drought and a global pandemic - the results have been significant. Two-way passenger traffic at CTIA has grown by 92% since 2015, while overnight foreign visitors have also increased by 92%.

Correlation between foreign air Arrivals and foreigners overnighting in Cape Town (2009 – 2025)

/Screenshot%202026-06-17%20160553.png)

Source: HVS Research

Traditional overseas source markets - Germany, the United States, and the United Kingdom - have been major drivers of growth. As air connectivity between these countries and Cape Town has improved, demand has risen steadily, as illustrated below. By the end of 2024, a significant share of travellers from these key markets were using direct flights: Germany (36%) and the United States (46%). Data for the United Kingdom segment is not available.

Impact of air capacity growth for arrivals at CTIA (2004 – 2025)

/Screenshot%202026-05-14%20164214.png)

Source: HVS, CTAA, Stats SA

Growth from these and other key markets have had a significant ripple effect on the hotel sector. Between 2015 and 2025, available room nights in Cape Town increased by approximately 720,000 while room nights sold rose by around 560,000.

/Screenshot%202026-05-14%20164408(1).png)

Source: CoStar

The observed growth likely understates the true impact of expanded air capacity. The reason being a 173% increase in hotel revenue compared to the previous decade. Rising rates, particularly within the luxury and upper-scale segments, have likely displaced a portion of demand into alternative accommodation options.

As CoStar data captures only hotel performance, the reported growth in room nights appears relatively moderate. In reality, total accommodation demand in Cape Town has almost certainly expanded far more significantly than hotel-only data suggests. An overview of accommodation preferences among foreign visitors indicates a diverse mix of options, with hotels and stays with friends and relatives remaining the most prominent choices.

Bednights by accommodation type used by foreign guests in the Western Cape (2025)

/Screenshot%202026-05-25%20180105.png)

Source: South African Tourism

Rooms revenue from the luxury and upper-scale segments accounted for 54% of total revenue growth, underscoring their outsized influence on the market. These segments have been central to pricing dynamics, with average daily rates (ADR) in the luxury category increasing from approximately USD 125 in 2015 to USD 288 in 2025 - equating to a compound annual growth rate (CAGR) of 8.7%. Importantly, this increase has occurred despite the continued depreciation of the South African Rand, further enhancing the relative purchasing power of international travellers.

In 2025, the United States (152,000 CTIA arrivals), Germany (159,000 arrivals), and the United Kingdom (179,000 arrivals) emerged as not only the primary drivers of international demand, but also spend in Cape Town. While the United States generated comparatively lower visitor volumes, its economic contribution was significantly higher. YOCO transaction trends over the 2025 festive season indicate that, despite Germany and the United Kingdom recording visitor volumes 5% and 18% higher than the United States respectively, American travellers accounted for 40% of total international card transactions on YOCO devices. This is nearly double the combined contribution of the other top four markets, underscoring the disproportionate economic value of U.S. visitors.

Top 5 countries by contribution to international spend (2025 festive season)

/Screenshot%202026-05-14%20164941.png)

Source: YOCO

This concentration of high-value demand is further reflected in transaction patterns. Notably, 62% of international card transactions recorded by YOCO took place in Cape Town, compared to just 3.1% in Johannesburg, 2.7% in Stellenbosch, and 2.0% in Plettenberg Bay. This underscores Cape Town’s dominant position as the primary hub for international visitor spend in South Africa.

Top 5 South African cities by international card transactions (2025 festive season)

/Screenshot%202026-05-25%20175910.png)

Source: YOCO

Regional Spillover Effects

It is noteworthy that Stellenbosch and Plettenberg Bay now rank ahead of Pretoria and are approaching Johannesburg in terms of international visitor spend. This reflects how improved air access to Cape Town is increasingly unlocking tourism opportunities beyond the primary metropolitan hub.

Room-night demand in the Cape Winelands and along the Garden Route has increased by 17% between 2015 and 2025. Over the same period, revenue (in dollar terms) has grown by 127% and 59% respectively, driven by rising international and domestic demand, as well as constrained supply, particularly during peak periods.

At the same time, George Airport - the primary air gateway to the Garden Route - has reached capacity. The terminal is designed to accommodate approximately 900,000 passengers annually; however, passenger volumes exceeded this level in 2025. This has prompted Airports Company South Africa to announce plans for an expansion, which is expected to effectively double capacity.

In parallel, a proposed international convention centre in the George area, currently in the feasibility phase, is expected to further stimulate demand. Together, these developments are likely to support continued growth in visitor volumes and drive increased investment in the regional hotel sector.

Room-night demand in the Cape Winelands and along the Garden Route has increased by 17% between 2015 and 2025. Over the same period, revenue (in dollar terms) has grown by 127% and 59% respectively, driven by rising international and domestic demand, as well as constrained supply, particularly during peak periods.

At the same time, George Airport - the primary air gateway to the Garden Route - has reached capacity. The terminal is designed to accommodate approximately 900,000 passengers annually; however, passenger volumes exceeded this level in 2025. This has prompted Airports Company South Africa to announce plans for an expansion, which is expected to effectively double capacity.

In parallel, a proposed international convention centre in the George area, currently in the feasibility phase, is expected to further stimulate demand. Together, these developments are likely to support continued growth in visitor volumes and drive increased investment in the regional hotel sector.

Seasonality

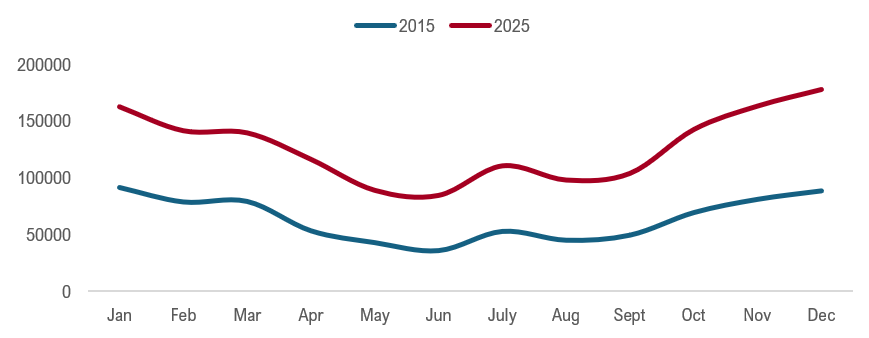

While the majority of CTIA’s additional air access remains concentrated in peak periods, Wesgro notes that the April to September period is expected to see a 20% increase in capacity in 2026, reflecting growing demand outside traditional peak months. The graph below illustrates the strengthening of demand across both peak and off-peak periods.

International overnight visitors to CTIA

This trend is also evident in regional markets, where room-night demand between May and September has increased significantly. Between 2015 and 2025, off-peak demand grew by 22% in the Cape Winelands and by 31% along the Garden Route.

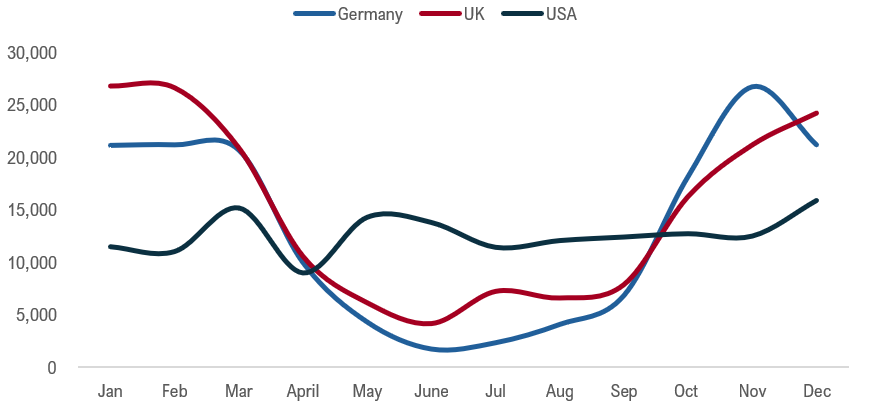

The United States plays a key role in shaping a more consistent, year-round demand pattern, with 2025 showing notable peaks in March, May, and June. In contrast, the United Kingdom and Germany continue to exhibit more traditional, seasonally driven travel patterns.

The United States plays a key role in shaping a more consistent, year-round demand pattern, with 2025 showing notable peaks in March, May, and June. In contrast, the United Kingdom and Germany continue to exhibit more traditional, seasonally driven travel patterns.

Source market seasonal trends – arrivals to CTIA in 2025

The increase in demand during Cape Town’s winter period aligns with the peak safari season, reflecting coordinated travel patterns across South Africa’s key tourism regions.

A Destination On The Rise

CTIA is approaching capacity as demand continues to grow, with infrastructure upgrades already in planning. These improvements are expected to increase throughput from 30 to 45 flights per hour by 2030, supporting the next phase of expansion. Importantly, enhanced air access into Cape Town is not only supporting growth within the city itself but is increasingly acting as a catalyst for tourism demand across the broader Western Cape, including the Cape Winelands and Garden Route.

Cape Town continues to strengthen its position as a leading global destination, with peak-period demand increasingly testing existing capacity. Encouragingly, rising winter capacity signals a more balanced distribution of visitors throughout the year, reducing reliance on traditional high-season peaks and supporting more consistent demand in regional markets.

With its combination of natural beauty, cultural richness, and global appeal, the region presents strong long-term growth potential. However, as with any long-haul destination, sustained growth remains closely tied to air connectivity and the ability to efficiently disperse visitors beyond the primary gateway.

The CTAA has played a pivotal role in driving this expansion, and its continued momentum—despite ongoing global uncertainty—positions both Cape Town and its surrounding regions strongly for the future.

Recent collaborations between destination stakeholders and international carriers, including the newly announced Wesgro–Emirates partnership, continue to signal long-term confidence in Cape Town’s tourism growth trajectory.

Cape Town continues to strengthen its position as a leading global destination, with peak-period demand increasingly testing existing capacity. Encouragingly, rising winter capacity signals a more balanced distribution of visitors throughout the year, reducing reliance on traditional high-season peaks and supporting more consistent demand in regional markets.

With its combination of natural beauty, cultural richness, and global appeal, the region presents strong long-term growth potential. However, as with any long-haul destination, sustained growth remains closely tied to air connectivity and the ability to efficiently disperse visitors beyond the primary gateway.

The CTAA has played a pivotal role in driving this expansion, and its continued momentum—despite ongoing global uncertainty—positions both Cape Town and its surrounding regions strongly for the future.

Recent collaborations between destination stakeholders and international carriers, including the newly announced Wesgro–Emirates partnership, continue to signal long-term confidence in Cape Town’s tourism growth trajectory.