Paris has long commanded a unique position in the global hotel landscape, a city where the convergence of world-class leisure appeal and robust corporate demand creates a market of rare depth and breadth. Yet for much of the past decade, a series of external shocks, from terrorist attacks and periods of social unrest to the once-in-a-century disruption of the pandemic, repeatedly prevented the market from fully realising its underlying potential. In 2025, that ceiling was finally broken. Occupancy levels surpassed any previously recorded figure in at least ten years, validating what investors and operators had long recognised: Paris’s structural fundamentals are as compelling as ever.

The legacy of the 2024 Olympic and Paralympic Games has proven far more enduring than a temporary demand surge. Rather than generating only short-term uplift, the event materially enhanced Paris’s global positioning and accelerated long-planned urban improvements. Investments tied to the Games, including enhanced transport connectivity, upgraded public realm infrastructure and visible improvements to urban cleanliness, have meaningfully elevated the overall visitor experience. Further strengthening the city’s momentum, the reopening of Notre-Dame de Paris in December 2024, following five years of painstaking restoration, has already demonstrated its power as a renewed magnet for global tourism, adding fresh impetus heading into 2026 and beyond.

Sources: INSEE; Aéroports de Paris; HVS Research

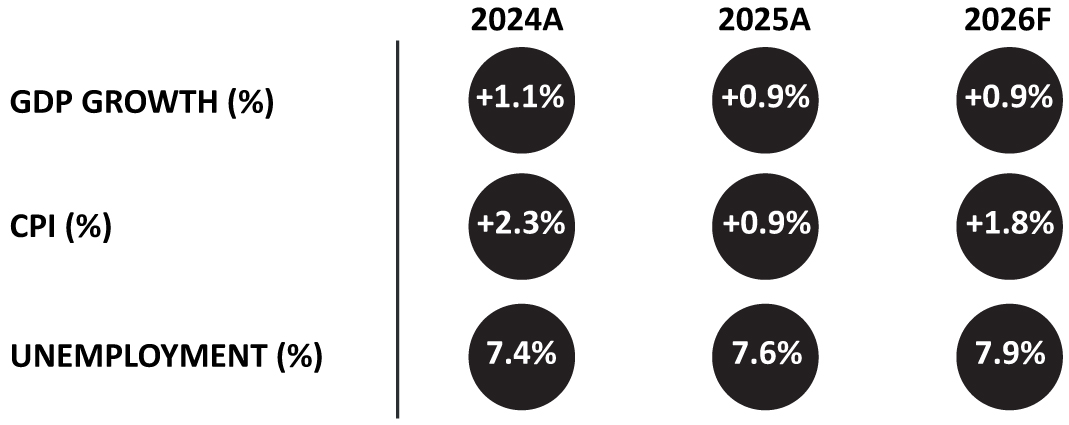

Economic Indicators – France

Source: IMF

Tourism Demand

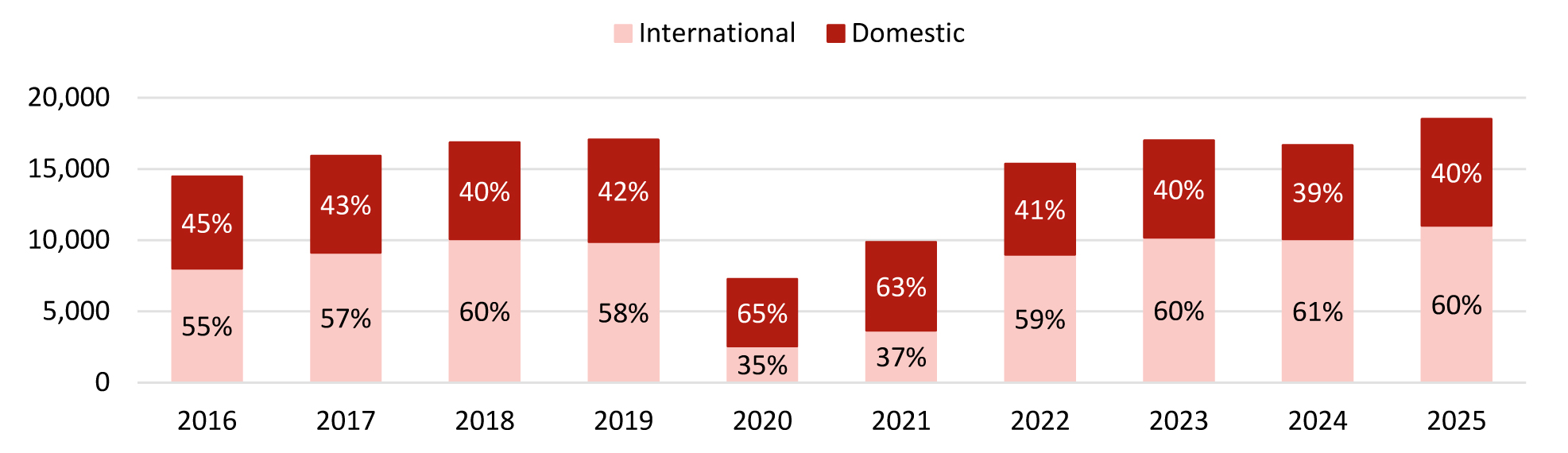

Visitor volumes to Paris in 2025 built materially upon the Olympic momentum of the prior year. Airport traffic at Orly and Charles de Gaulle reached approximately 107 million passengers, a further 3.4% increase on 2024’s already record 103.4 million, signalling that the city’s accessibility and appeal have entered a new chapter. International arrivals accounted for approximately 60% of the visitor mix, supported by Asian and US demand, with American visitors responding strongly to Paris’s post-Olympic global media exposure and the cultural draw of the reopening of Notre-Dame de Paris

Airport trends are closely mirrored in visitor numbers in Paris. INSEE data confirm that 2025 set a new high-water mark, surpassing even the record levels reached at the end of 2023. Domestic demand remained a stable foundation, representing around 40% of visitors, while international visitors, led by a strong US performance, drove occupancy to unprecedented levels.

The meetings and events segment presents a more nuanced picture. According to ICCA data, Paris hosted 174 internationally ranked association meetings in 2025, a strong rebound from the temporary dip to 124 meetings in 2024, when the Olympic Games prompted many event organisers to defer or relocate events. Despite this significant recovery, conference activity in Paris remains below pre-pandemic levels, with the city still trailing the 237 meetings recorded in 2019. While leisure and transient corporate demand have already surpassed prior peaks, the meeting and conference segment continues to recover at a more gradual pace. Given this dynamic, we expect a rebound in conventions and large-scale corporate gatherings to materialise progressively through 2026 and 2027.

Visitor Numbers – Paris (000s)

Source: INSEE

Hotel Performance

The 2025 performance data mark a significant milestone for the Parisian hotel market. Average occupancy reached 78%, matching the strongest level recorded in the past ten years and effectively equalling the 2018 peak, a figure that had long stood as the market’s benchmark through a turbulent intervening period of social unrest, pandemic disruption, and the operational complexities of hosting the Olympic Games. That 2025 has returned to this level, against a backdrop of normalising demand rather than a single exceptional catalyst, speaks volumes about the durability of Paris’s recovery.

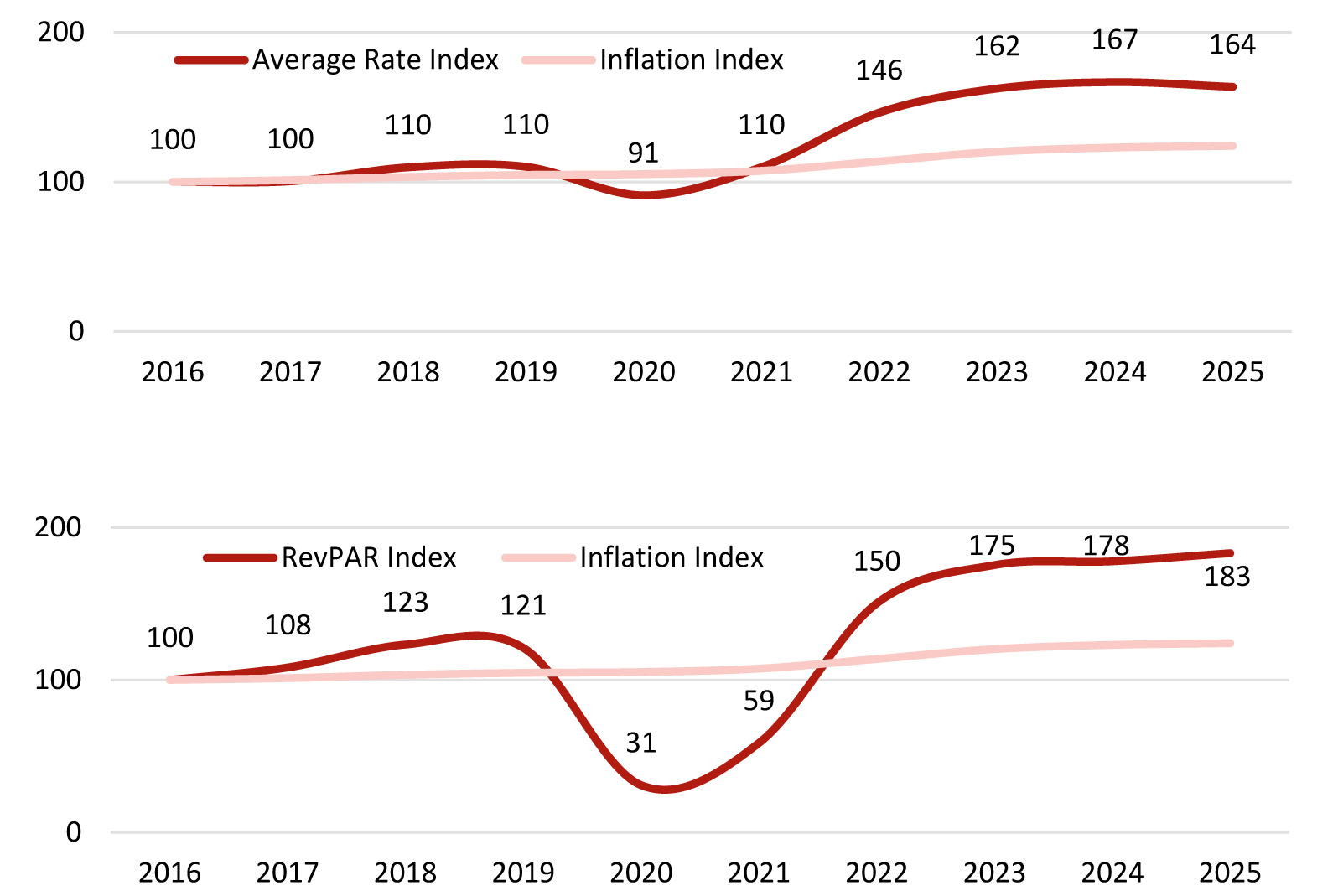

Average rate reached close to €350 in 2025, a modest 2% decline against 2024, reflecting a natural recalibration following the exceptional pricing environment of the Olympics period. Over a ten-year horizon, however, the rate trajectory remains compelling: average rate has grown by 64% since 2016, materially outpacing inflation over the same period and underlining the market’s sustained pricing power. The luxury and palace segments have been key drivers of this growth, with a wave of notable new openings over the last ten years increasing their share of the Paris hotel inventory. Together with significant refurbishments across this segment, this has been a key contributor to average rate growth in the market. That said, broader market segments have also demonstrated meaningful rate progression.

RevPAR increased 3% year on year, and is now 83% above 2016 levels, underscoring the extent of the market’s structural recovery. This performance reflects a period of more stable operating conditions, which has supported occupancy, alongside more efficient room night compression, a strengthened and more diversified hotel supply, and a higher share of international demand driving overall yield growth.

Performance Index – Average Rate and RevPAR

Sources: HVS Research

Hotel Supply

Paris ended 2025 with approximately 1,790 hotels and around 97,000 rooms, a supply base that has remained deliberately constrained relative to demand growth. The city’s historic built environment and stringent planning framework continue to act as natural barriers to speculative development, a structural feature that has served the market’s rate integrity well over time.

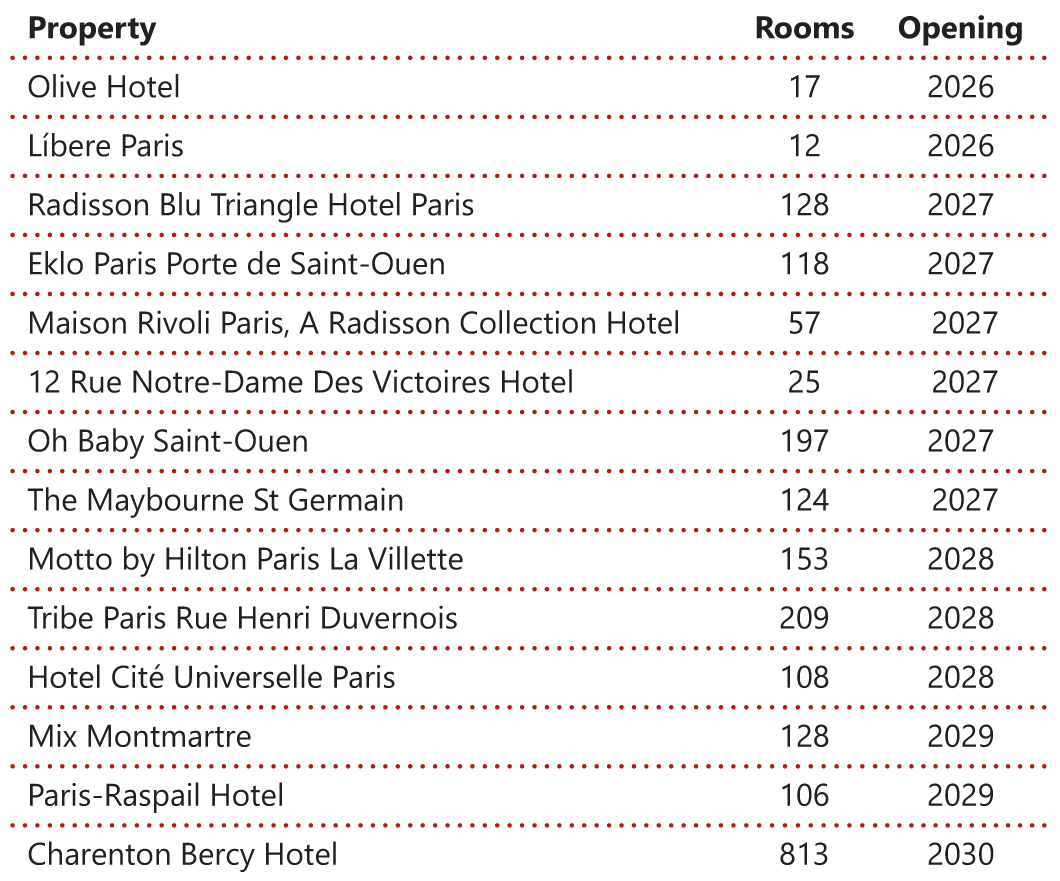

The forward pipeline includes some 3,300 rooms across 27 projects scheduled to enter the market through 2030. This pipeline represents about 3.4% of existing supply, a modest increment by any measure. The near-term outlook through 2027 is therefore one of continued supply discipline, with only incremental additions across a spread of concepts and submarkets.

The composition of the pipeline reflects both investor appetite and the city’s premium positioning. Lifestyle and upscale concepts dominate, with notable additions including the 128-room Radisson Blu Triangle Hotel, and the 124-room Maybourne Saint Germain which will add further ultra-luxury depth to the Left Bank. At the same time, the 197-room Oh Baby Saint-Ouen and the 153-room Motto by Hilton Paris La Villette speak to the growing appeal of outer arrondissements as viable hotel locations, supported by improved connectivity and the urban regeneration legacy of the Olympic Games.

Independent operators retain majority representation across the existing stock, a balance that has remained broadly stable despite the continued expansion of branded concepts in the market. This diversity of ownership and positioning remains a defining characteristic of Paris hospitality, sustaining its ability to appeal across a wide spectrum of traveller segments and price points.

Hotel Pipeline

Sources: HVS Research

Investment Market

Transaction activity in the Paris hotel market has remained robust across the 18 months to the end of 2025, with a notably broad spread of deals spanning budget conversions through to trophy luxury assets. This breadth is itself a signal of market maturity: investor conviction in Paris is no longer confined to the palace and ultra-luxury segments, but extends across the full risk spectrum, reflecting confidence in the city’s underlying demand fundamentals at every price point.

At the luxury end, the Mandarin Oriental Paris transacted in April 2024 at €1,486,000 per room, one of the highest per-key figures recorded in the French capital in recent years. The Saint James & Albany (144 rooms, €1,354,000 per room) and the Pullman Paris Tour Eiffel (430 rooms, €767,000 per room) further demonstrate sustained investor appetite for established full-service assets in prime locations. More recently, the Banke Hotel changed hands in July 2025 at €1,078,000 per room, and the Chateau des Fleurs achieved €1,351,000 per room in October 2025, underscoring that pricing at the upper end of the market has remained firmly anchored through the post-Olympic period.

At greater scale, the Pullman Hotel Montparnasse disposal at approximately €313,000 per room in September 2025 highlights that institutional demand extends well beyond the luxury niche. Meanwhile, smaller transactions such as the ibis Styles Paris Crimée La Villette at €150,000 per room and Hotel Maubeuge at €310,000 per room reflect active repositioning interest in the economy and budget segments, a market dynamic that broadens the overall buyer pool and reinforces liquidity across cycles.

Our Hotel Valuation Index continues to place Paris at the top of European hotel markets by value per room, and the margin by which the city leads its continental peers has widened further in the past 12 months. With capitalisation rates remaining broadly stable and the RevPAR outlook positive, the conditions for sustained asset value growth remain firmly in place.

Hotel Transactions

Sources: HVS Research

Outlook

The Paris hotel market enters 2026 on a strong operational footing. Occupancy has returned to its ten-year peak, RevPAR is at record levels in both nominal and real terms, and investment appetite, spanning budget conversions through to trophy luxury assets, has rarely been more broadly distributed across the market.

The macroeconomic backdrop calls for measured attention. France’s GDP growth is forecast at 0.9% for both 2026 and 2027, reflecting a subdued European economic environment. Inflation has eased at around 2%, removing a key headwind for consumer spending. Unemployment ticked up marginally to 7.6% in 2025 and is projected to edge modestly higher, though this has not yet manifested in any softening of leisure or corporate travel demand. International demand from certain source countries is starting to be affected by the current conflicts in the Middle East which, together with cancelled flights and the fuel price crisis, may dent demand. However, if Paris has proven one thing in the last decade, it is its resilience against various headwinds.

On balance, however, the structural pillars underpinning Paris’s hotel performance remain firmly intact. Supply discipline, exceptional brand recognition, recovering conference activity, and the sustained afterglow of the Olympic legacy point convincingly towards continued strength. For investors, operators and the city alike, the light at the end of the tunnel has become the dawn of a new chapter.

Value Trends 2025 vs 2024

Sources: HVS Research