Equity yield is the rate of return that an equity investor expects over a ten-year holding period. It specifically considers annual inflation-adjusted cash flows, property appreciation, mortgage amortization, and proceeds from a sale at the end of the holding period. Notably in today's environment, the equity yield rate also reflects the effect of debt financing on the cash flow available to the equity investor.

The total property yields (discount rates) presented reflect the "free and clear" internal rate of return to an all-cash purchaser, or a blended rate of debt and equity return requirements. The discount rate takes into consideration the degree of perceived risk, anticipated income growth, market attitudes, and rates of return on other investment alternatives, as well as the availability and cost of financing.

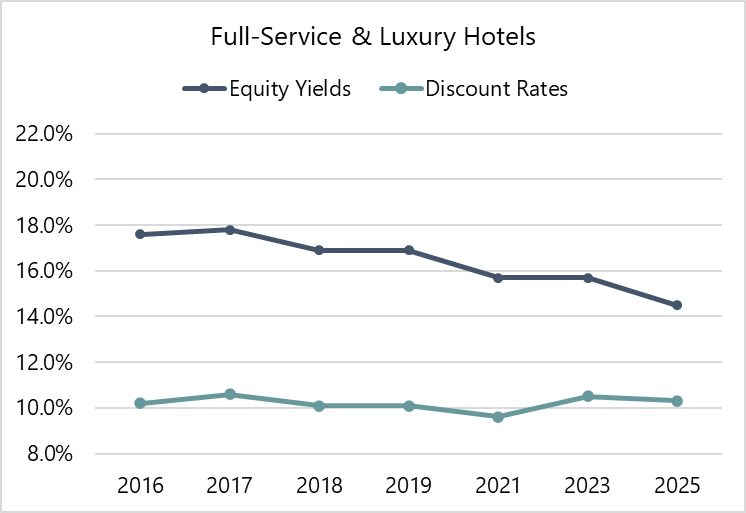

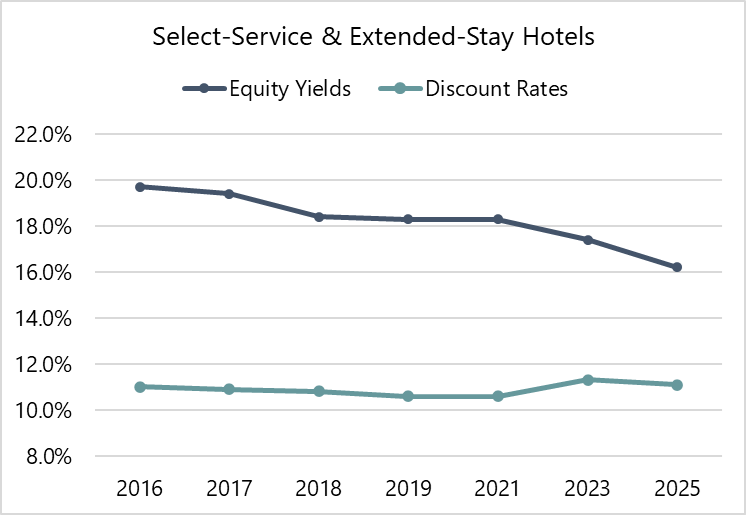

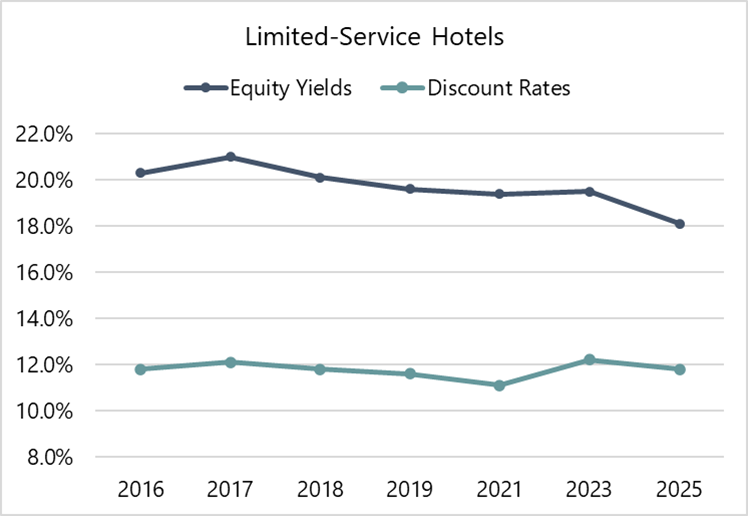

The charts below illustrate historical trends for both equity yields and discount rates for three main hotel segments. We note that there tends to be a lag between the sales data and current market conditions; thus, the full effect of the changes in the economy and capital markets may not yet be reflected.

All Segments Show Steady Decline in Equity Yields but Stability in Discount Rates

Source: HVS Data

Source: HVS Data

Source: HVS Data

Source: HVS Data

Source: HVS Data

Source: HVS Data

The data illustrates a clear and consistent trend: equity yields have declined steadily across all three hotel segments over the past decade. Full-Service & Luxury hotels saw the most significant compression, with equity yields falling from 17.6% in 2016 to 14.5% in 2025, a decline of 310 basis points. Select-Service & Extended-Stay hotels followed a similar path, with equity yields for this segment declining from 19.7% to 16.2% over the same period. Limited-Service hotels, which have historically achieved the highest equity yields due to their greater perceived risk, declined from 20.3% to 18.1%. Collectively, this trend suggests that investors have grown increasingly comfortable with hotel assets and have been willing to accept lower returns as a result.

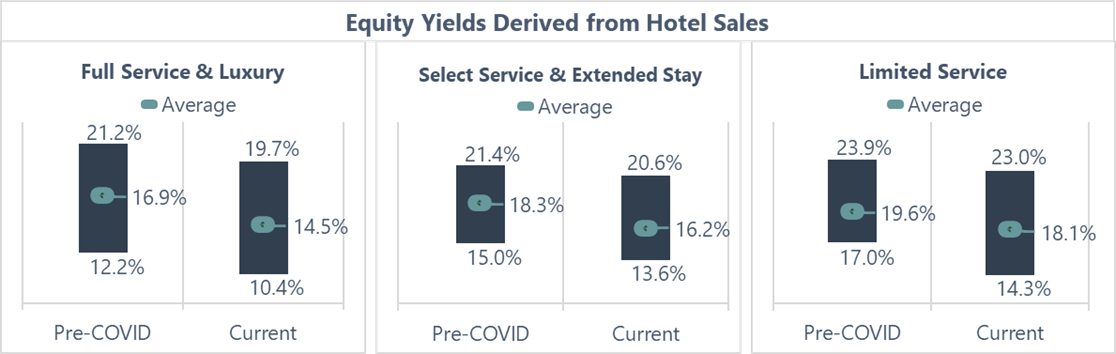

Current Equity Yields Show Declines Compared to Pre-COVID Levels

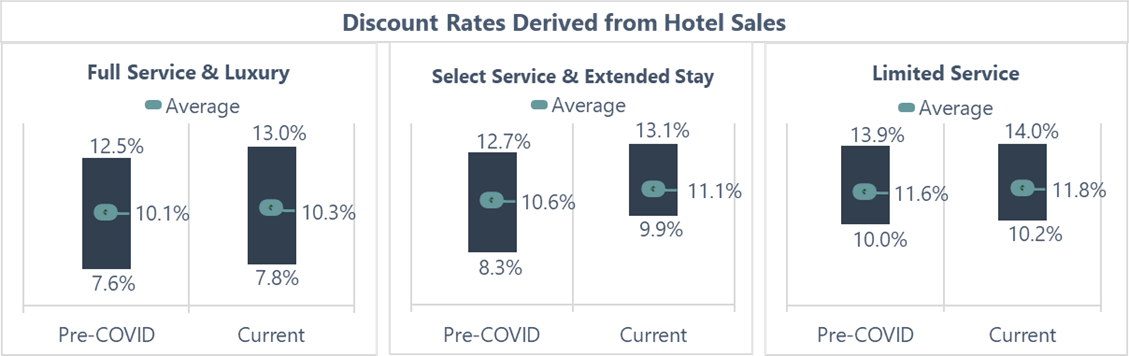

Current Discount Rates Show General Stability Compared to Pre-COVID Levels

Source: HVS Data

The divergence between these two metrics is significant. While discount rates have remained largely tied to broader economic conditions and interest rate cycles, equity yield expectations have shifted in a more structural way.

The steady decline in equity yields, even as discount rates fluctuated with broader economic conditions, points to a lasting increase in investor confidence in the hotel sector. In our view, current equity yield levels are approaching a natural floor. Should interest rates ease further and financing conditions improve, discount rates would likely respond. Equity yields, however, have shown a decade-long resilience to those forces, suggesting the decline is caused by a genuine shift in the way investors value hotels, rather than a response to financing conditions alone.

That said, a meaningful rise in transaction volume could bring more investment alternatives into focus, giving equity investors less reason to accept lower returns. Broader economic uncertainty, the long-term commitment that hotel ownership demands, and the inherent operational complexity of the asset class all reinforce why return requirements are unlikely to fall much further. Balancing these forces, stability is likely the most reasonable expectation for equity yields in the near term.

At HVS, we turn data into powerful insights that drive your success. For help making informed investment decisions that align with your goals and risk tolerance, please contact Katy Black, MAI.