The Transaction Bottom: Deal Volume is Recovering

The hotel transaction market is improving, but the numbers require careful context. According to MSCI Real Capital Analytics, hotel deal volume grew to approximately $27.9 billion in 2025, up from the 2024 trough of $24.7 billion.Critically, price declines are narrowing sharply, from -4.5% in 2023 to just -1.3% in 2025. CoStar projects a return to positive price appreciation (+0.5%) in 2026, suggesting the market has found its floor.

However, this recovery is not uniform. Individual assets are outperforming portfolio trades, with single-asset deal activity rising approximately 16.0%, a signal that institutional buyers are willing to pay premium prices for the right property.

The Great Bifurcation: A Deepening Two-Tier Market

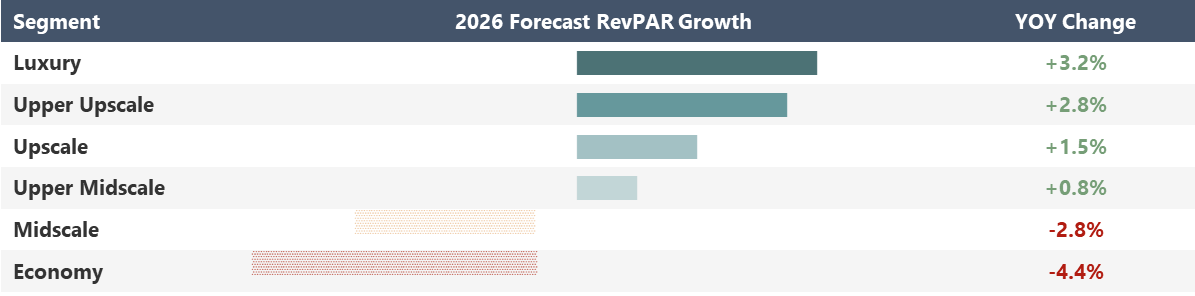

The Great Bifurcation remains the central investment theme of 2026. We expect U.S. RevPAR growth of about 2.2% this year, as published in the HVS U.S. Market Pulse for February 2026. That headline figure, however, conceals a massive divide in performance between the higher and lower segments.

The STR/CoStar February 2026 forecast is lower, at 0.6% blended RevPAR growth, yet the segmented forecast aligns with what is evident in the market. Performance gains are concentrated in luxury and upper-upscale hotels, while select-service and economy assets continue to face ADR pressure and flat-to-negative RevPAR trends.

The divide is likely to persist and is tied to income-based demand strength. Higher income travelers remain resilient, supported by wage gains and household wealth. Owners in middle and lower chain scales should stress-test 2026 hold and exit assumptions.

2026 Projected RevPAR Growth by Segment Illustrates the Bifurcation

Investor Implications

Institutional capital is running a clear barbell strategy in 2026. Buyers are aggressively pursuing trophy luxury assets as long-term inflation hedges. They are also selectively acquiring economy assets where pricing already reflects the RevPAR pressure and includes a discount for it.For owners, the key point is this: Transaction values in the economy segment have not fallen as sharply as RevPAR because buyers are underwriting to a stabilized floor rather than the current trough.

If you own a midscale or economy asset with a deteriorating RevPAR index, buyers have not disappeared. They are pricing accordingly, and the window to sell above a distressed basis is narrowing as more supply enters the market.

The Renovation Imperative: PIP as a Transaction Catalyst

The era of deferring brand-mandated property improvement plans (PIPs) is ending, hard. With construction costs still elevated and interest rates squeezing returns, the PIP decision has become the most consequential transaction lever of 2026.The math is unforgiving: the hotel sector faces a $48-billion CMBS maturity wave for 2025 and 2026. Roughly $23 billion of this amount was refinanced from 2020–2022 at 3.0–4.5% rates, but today’s borrowers face debt costs of 6.25–7.0% or higher, a 40.0% increase in carrying cost. When you layer a $2M–$8M PIP obligation on top of a refinancing that costs 300 basis points more than expected, many owners are forced to sell.

For buyers, this dynamic creates two distinct deal types:

- “Turnkey” assets where the owner has recently completed the PIP; these command a premium from the marketplace.

- “Value-add” plays where a buyer acquires at a discount to replacement cost, executes the PIP, and repositions the asset within 18 to 24 months.

The Critical Question for Every Owner

Buyers do not take a deferred PIP at face value. They underwrite it at a premium and add costs for contractor uncertainty, revenue disruption during construction, brand compliance risk, and the cost of capital during a renovation hold period. The result is that a deferred PIP obligation usually reduces the offer price by more than the stated renovation budget. Get your brand-mandated estimate in hand before you list. It is better to control the narrative upfront than to let a buyer define it during due diligence.The 2026 FIFA World Cup: A Narrow but Real Opportunity

The 2026 World Cup, hosted across eleven U.S. cities, Canada, and Mexico, is forecasted to contribute a full-year 0.6% RevPAR lift for U.S. hotels, according to STR. For host markets, the math is more compelling: STR projects that World Cup host markets will see June/July RevPAR rise +12.7% year-over-year. The host cities are projected to realize a +3.8% growth in RevPAR for the year, outperforming the national average by more than 300 basis points, compared to just +2.0% annual growth if the tournament weren't played.Critically for transaction purposes: the World Cup creates a specific pricing window. Assets in host markets can present demonstrably higher trailing-twelve-month (TTM) income during World Cup months, which sophisticated buyers will normalize, but which still creates a higher “peak earnings” marketing narrative.

2026 FIFA World Cup Host Markets (U.S.)

The Debt Maturity Wave: Sell Before the Crowd Does

Debt maturity is the most underappreciated seller urgency signal of 2026. According to S&P Global Market Intelligence, approximately $936 billion in CRE loans mature in 2026 alone, a 19% increase over 2025’s revised estimate. A significant portion involves hotel CMBS debt originated in 2020–2022 at historically low rates.Hotel-specific CMBS delinquency hit 7.29% as of August 2025, nearly six times the traditional bank loan delinquency rate. Hotel mortgage spreads widened to 375 basis points over comparable Treasuries by Q4 2025, compared to 225–250 bps for multifamily and industrial.

For owners with maturities in the next 12–18 months, the choice between “refinance and hold” and “sell now” has rarely been this consequential. Owners who wait for full loan maturity before beginning a sale process often find themselves in a compressed timeline with reduced buyer leverage.

Debt Maturity Pressure: Key Statistics

- $936B in CRE loans mature in 2026

- Hotel CMBS delinquency: 7.29% as of August 2025

- Hotel mortgage spreads: 375 bps over Treasuries (vs. 225–250 bps for multifamily)

- 39% of hotels with low debt service coverage ratios already facing cash flow strain

- Refinancing today’s spreads can increase annual debt service by $300K to $1M+ per year

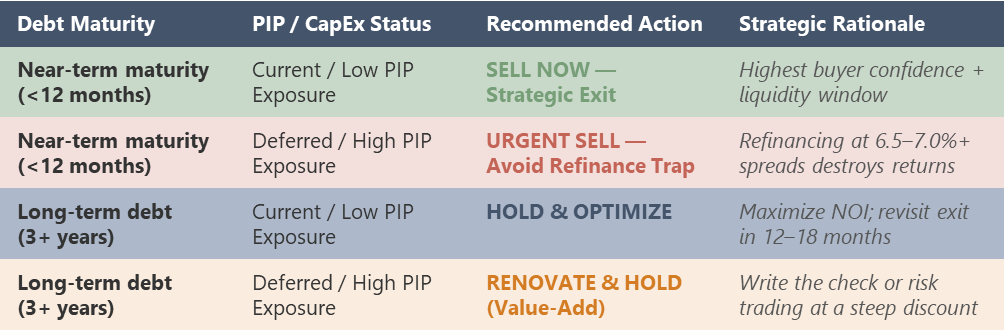

Seller Readiness: The Decision Framework

The two primary variables, debt-maturity timeline and PIP exposure, determine your urgency and optimal transaction strategy. Use this matrix to quickly position your asset and identify the right action for 2026.

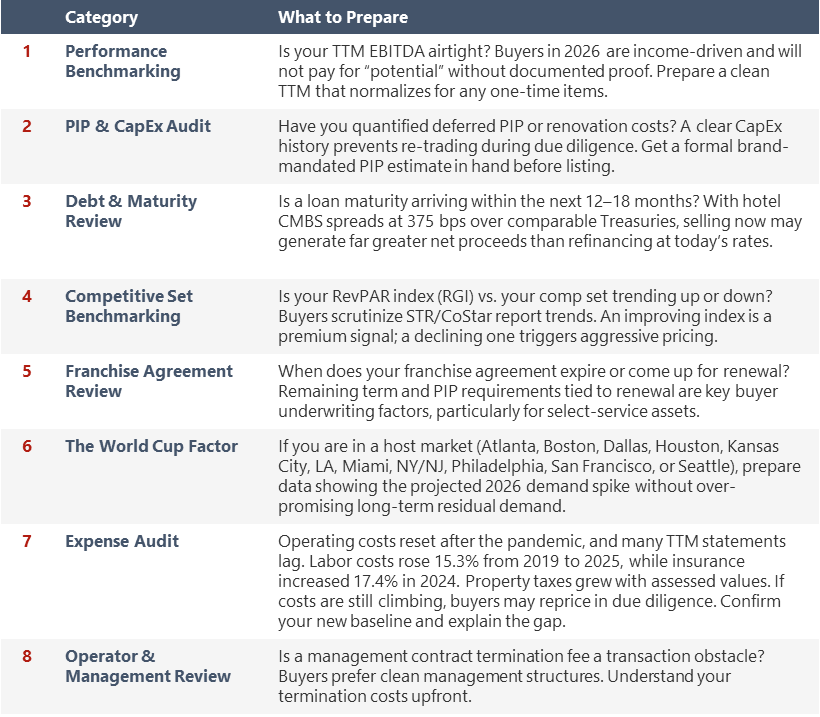

The 2026 Pre-Sale Readiness Checklist

Before engaging a broker or preparing for a marketing process, examine your asset through this eight-point audit. Buyers in 2026 perform deep due diligence, and surprises discovered after the letter of intent (LOI) are the primary driver of “re-trading” (post-LOI price reductions) and deal failure.

Data Source: Hotel Dive

What Buyers Want in 2026

Understanding buyer psychology is as important as understanding your asset’s financials. Here is what the active capital sources are prioritizing:- Institutional Capital: Income certainty over projection-based growth. Buyers are underwriting to in-place NOI, not upside pro formas. A clean, defensible TTM with normalized expenses is worth more than an optimistic five-year forecast.

- Value-Add Investors: Assets priced at or below replacement cost. With construction costs still elevated, buyers’ “build vs. buy” analysis often favors acquisition of existing assets at $150K–$250K per key vs. building at $350K–$500K+ per key.

- All Buyer Types: Markets with limited new supply pipeline. CoStar data shows 767,000 rooms in the national pipeline, but only 19% are under construction. Markets where new supply is constrained realize cap rate compression.

The Bottom Line

Ultimately, 2026 will not be a boom year. The HVS Americas February 2026 forecast projects just +2.2% overall RevPAR growth, below the long-term average of +3.0%. But it is a year of strategic opportunity for owners who move with clarity and preparation.The owners who will maximize value in 2026 are those who:

- understand the bifurcation dynamic and position their asset accurately within it,

- confront PIP and debt maturity realities head-on rather than kicking them down the road, and

- enter the market with a clean, well-documented asset before the debt-maturity wave forces others to do the same.

Is Your Hotel Ready to Trade in 2026? Request a complimentary Broker Opinion of Value (BOV) and learn exactly where your asset sits in today’s market before your competition does.