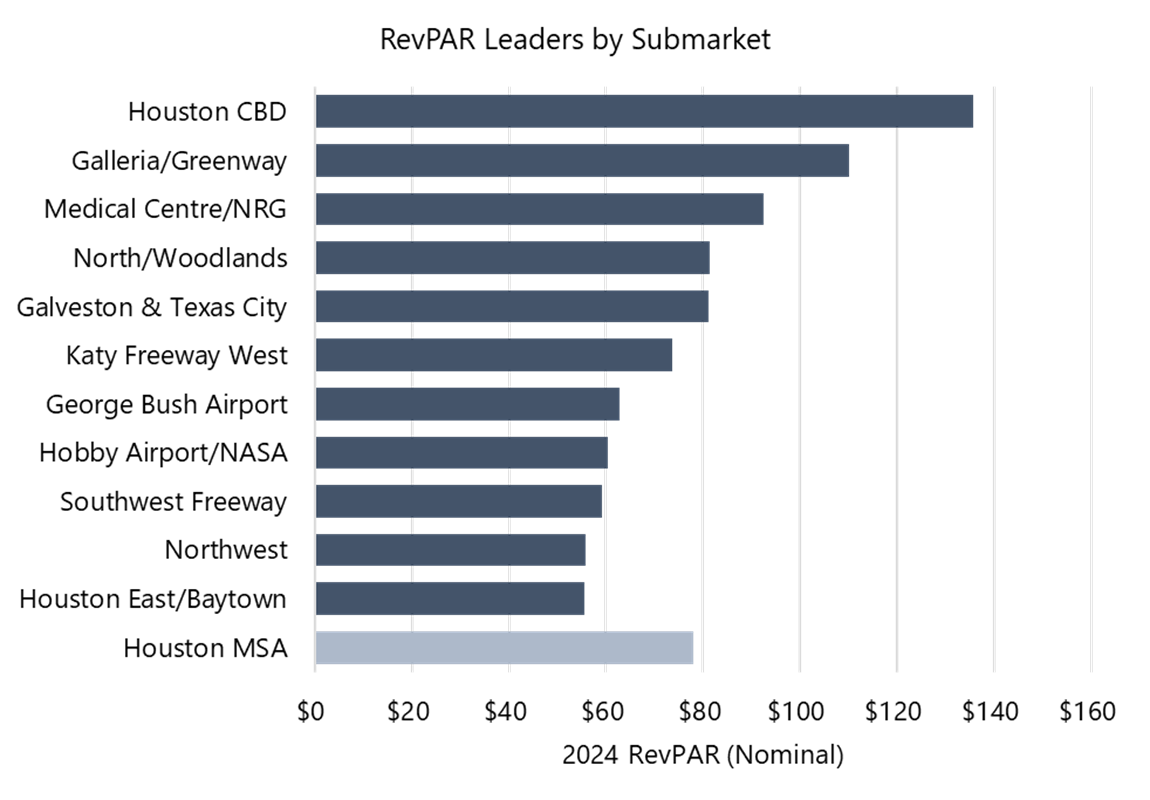

Event-Driven Lift and RevPAR Leaders

Market-wide results in 2024 were shaped by several concentrated demand drivers, including the College Football Playoffs in January, the May derecho storm, Hurricane Beryl in July, and stronger group and event activity during the year. These catalysts contributed to a RevPAR increase of roughly 15% compared with 2023 and about 21% from 2019.As shown in the chart below, Houston CBD recorded the highest revenues in the market in 2024, followed by Galleria/Greenway and the Medical Center/NRG. These submarkets benefited from steady corporate, convention, medical, and institutional demand, which supported their position at the top of the metropolitan performance range. The remaining submarkets trailed by varying margins in 2024 depending on their mix of transient, leisure, and price-sensitive demand.

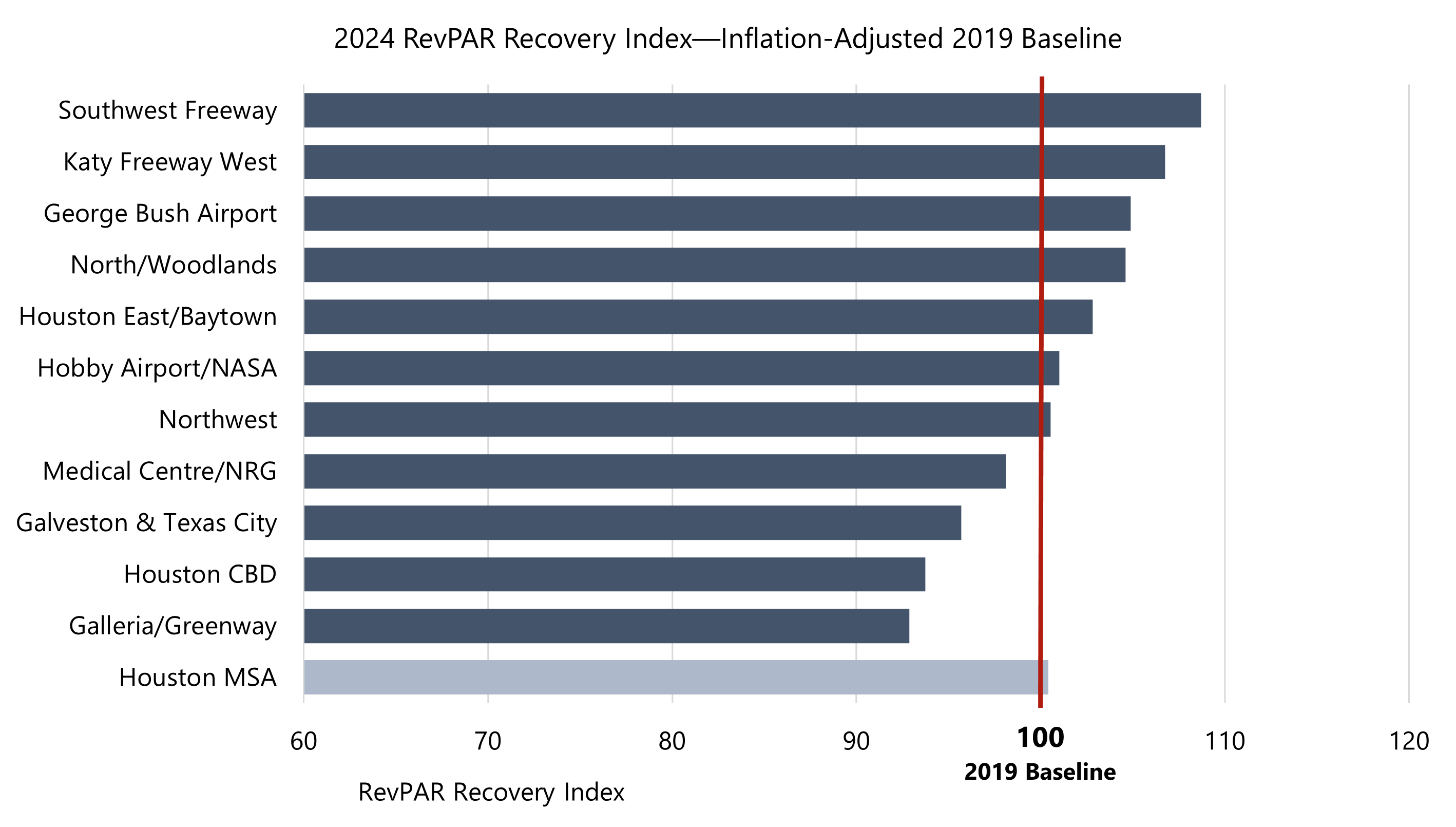

Inflation-Adjusted Recovery and Modest Variation

However, Houston MSA’s inflation-adjusted results show that most submarkets are only slightly above their 2019 RevPAR levels (as expressed in 2024 dollars), reflecting steady but modest real-dollar improvement across the region. As the recovery index shows, several submarkets recorded notable gains in their index scores, led by Southwest Freeway, Katy Freeway West, and George Bush Airport. A smaller group of submarkets, including Houston CBD, Galleria/Greenway, and Medical Center/NRG, remain below their 2019 baseline; although these areas lead the market in nominal RevPAR, they still fall short of prior-cycle levels in real-dollar terms. While 2024 was boosted by several short-term demand surges, these influences produced only limited improvement once adjusted for inflation.The inflation-adjusted indices reflect a range of 93 to 109, indicating moderate variation across the city and MSA submarkets. The real-dollar perspective highlights a market that has made steady progress since 2019, but not dramatic improvement, particularly after temporary 2024 factors are removed.

2024 RevPAR Levels Relative to 2019 Performance Show Different Submarket Leaders

Source: HVS, CoStar

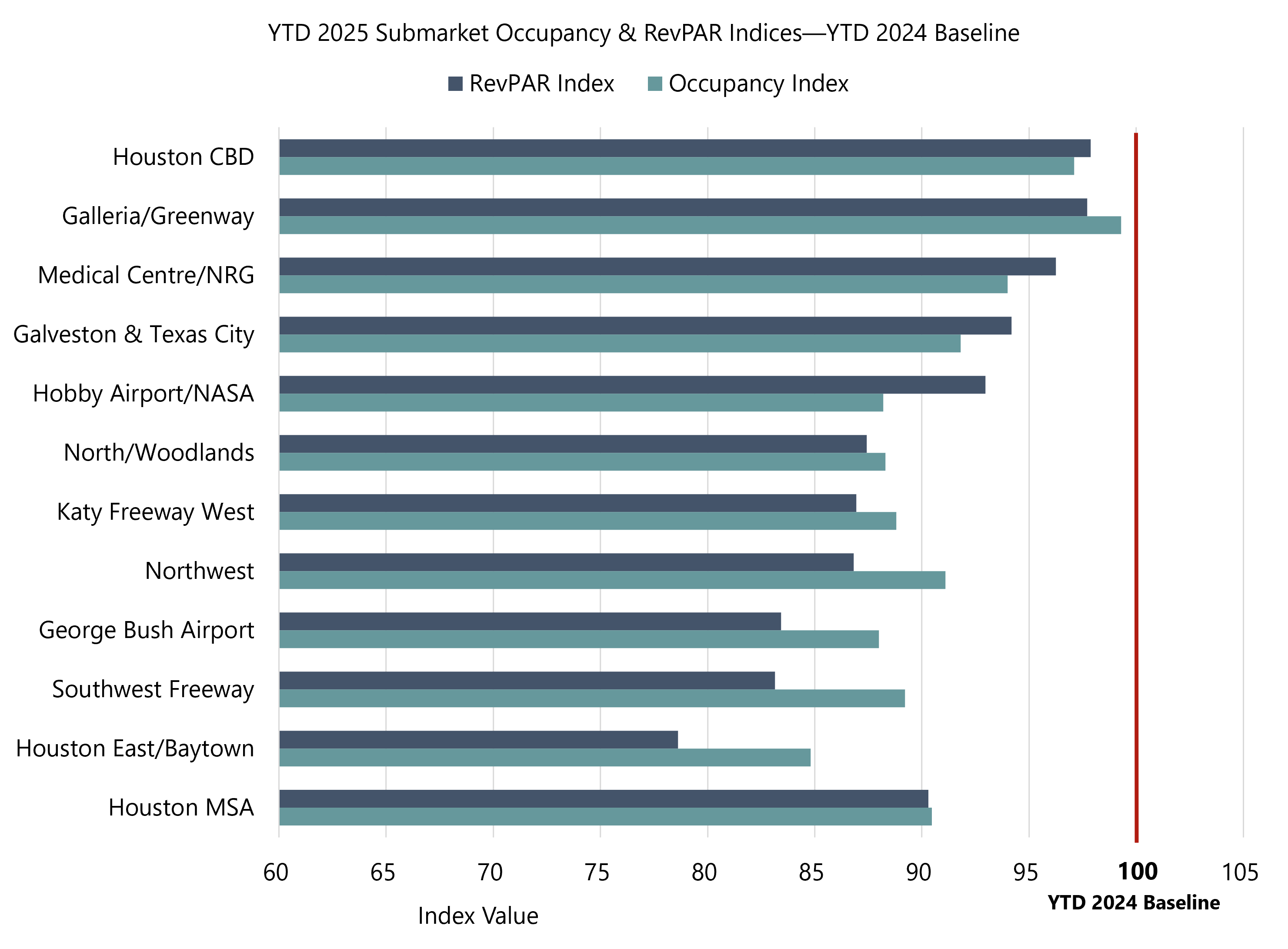

Normalization Across Submarkets

Houston entered late 2025 with steadier fundamentals as the temporary influences that lifted 2024 performance recede. Occupancy and RevPAR indices across most submarkets now reflect moderated operating ranges, with year-to-date results showing modest declines from last year’s peaks and a tighter clustering of outcomes across the metropolitan area. This pattern reflects both the normalization from 2024’s one-time catalysts and a more cautious travel environment that has slowed the pace of near-term improvement without shifting the market’s underlying growth trajectory.The submarkets have adjusted after last year’s surges but still have room for further improvement as overall demand is expected to strengthen. Core submarkets continue to post the highest nominal rates, while outlying submarkets have returned to more typical pricing levels.

Normalized YTD 2025 Submarket Performance Falls Below YTD 2024 Performance

From Cyclical Surge to Sustainable Base

Entering 2026, the hotel market is positioned for further improvement, supported by a broad mix of business, institutional, event, and leisure activity across both city and metropolitan submarkets. With volatility receding, performance is expected to be driven more by recurring demand than by short-term displacement or compression effects. The region’s ongoing economic diversification and continued corporate expansion help sustain a wider base of hotel demand. Group and convention activity is expected to reinforce this baseline, while Houston’s role as a host city for the 2026 FIFA World Cup will generate a temporary increase in visitation during the tournament period. Together, these factors provide a foundation for progress in 2026.At HVS, our strategic presence within the Houston market enables us to engage directly with key industry stakeholders and decision-makers. This hands-on approach ensures access to real-time insights and the most current data shaping local hotel performance. To learn more about Houston’s evolving hospitality landscape and market opportunities, contact Bunmi Oyinloye, your local HVS Houston and Gulf Coast hospitality expert.

Sources

CoStarSTR