Whether the setting is sun-and-sand, snow-and-ski, or an indoor water park, today’s destination resorts commonly feature real estate ownership programs. Structured as whole ownership, fractional ownership, or timeshare, these “residential” condominiums typically feature fully equipped kitchens and multiple bedrooms. This article provides a brief overview of this concept, using a turnaround case study to demonstrate methodology for evaluating ownership component economics.

Why is the Real-Estate Ownership Component So Necessary?

In the universe of real estate developments, high-end destination resorts are among the most costly. These projects typically require extensive acreage in strategic locations. They often demand major infrastructural investments. They can be complicated by issues concerning topography and utilities. Zoning and other governmental oversight hurdles tend to draw out the pre-construction phase.

Once open, most full-service resorts face a long ramp-up period. The prospect of selling off pieces of the resort right after its completion is often the only way to realize the project, as initial sales proceeds are commonly used to immediately de-leverage the property’s debt-heavy balance sheet. Real estate ownership programs are especially common in highly seasonal markets.

What’s in it for the Unit Owner?

Although the condominium units are referred to as “residences,” most unit owners only occasionally reside at the resort. Most unit owners forego occupancy on any given night and instead return the unit to the resort operator’s rental pool. If the room is rented, the tariff is split (typically in the range of 50/50) between the resort owner and the unit owner.

Rates of participation in the rental management program (RMP) vary from resort to resort, depending on the incentives used to motivate participation. Participating owners essentially become investment partners in the resort. Even if they don’t participate in the resort operator’s RMP, owners can still realize benefits beyond the pleasure of occupying their units. The investments often provide second-home ownership tax benefits (depending on rental frequency), and capital gains may be realized if the unit’s value appreciates significantly.

What Could Go Right? The Ideal Scenario for Resort Sales and Disposition

If all goes as planned, the residences will sell at the anticipated pace or faster, and the sales prices will align with or exceed expectations. The portion of the resort retained by the developer (including dedicated guestrooms, food and beverage outlets, and meeting space) will stabilize with cash flows sufficient to cover the resort’s debt and equity return requirements over the anticipated holding period. At disposition, the ongoing resort operation will have demonstrated its stability and health, and the developer-retained property will sell for a substantial premium to outstanding debt (which has been reduced through the residential sales). Meanwhile, a healthy resale market for the residential units will have formed, and the original owners will have realized significant capital gains.

What Could Go Wrong? Potential Challenges

Perhaps the most common challenge facing resort-residential sales efforts is completing the sell-off before an economic downturn waylays the process. Second-home condominium sales depend on high levels of discretionary income in the target market. When the economic fortunes of the resort’s feeder markets turn down, the population of potential buyers can fall to prohibitively low levels.

Perhaps the most common challenge facing resort-residential sales efforts is completing the sell-off before an economic downturn waylays the process. Second-home condominium sales depend on high levels of discretionary income in the target market. When the economic fortunes of the resort’s feeder markets turn down, the population of potential buyers can fall to prohibitively low levels.

There is also the challenge of identifying and penetrating a viable population of candidate buyers. The cost of mounting a marketing program is a major commitment, and momentum must be generated quickly. This risk is somewhat mitigated for branded resorts. Particularly in the case of internationally recognized brands with well-established vacation-ownership programs, resort owners with branded products tend to enjoy reduced time and cost when it comes to establishing the product’s market niche. In return, the brand receives a licensing fee calculated as a percentage of the gross sales proceeds.

Another key concern is the ongoing profitability of the resort-retained property, post sell-off. Assuming the resort’s internal and external economic conditions allowed for the successful transfer of all or most of the residences, the resort still must be operationally viable in its reduced format. Profit margins on resort operations are often slim. Selling lodging inventory to third parties means losing approximately half of the units’ rooms revenue. In addition, owners may choose to occupy their units during the peak season, in which case all unit revenue is foregone during the resort’s highest yield periods, including the share the resort owner would have collected.

Resort owners mitigate the impact of the revenue displacement, partially, by distributing some portion of the resort’s operating expenses to the unit owners, including much of the burden of replacement reserves necessary to fund renovations at the residences. The expense-sharing structure is contractually built into the relationship upon sale, whereby the interests and responsibilities of the unit owners are typically represented by a homeowners’ association (HOA). The HOA is assigned some share of the resort’s operating expenses, usually based on the square footage associated with the residences versus that of the broader resort. The total HOA expense is then allocated to the individual unit owners on a pro-rata basis. Expenses that typically qualify for reimbursement through HOA assessments are usually in the maintenance, utilities, property tax, insurance, and reserves for replacement categories. In addition, unit owners are usually charged a housekeeping fee when they occupy their units, as well as a modest administrative and general charge.

At the beginning of the project, before the first residence is sold, the resort owner is the sole HOA constituent. As the sell-off progresses, the owner’s share of the HOA expense shrinks. This cost-saving action occurs simultaneous with, and partially offsets, the rooms revenue reductions attributable to the unit-owner splits.

Overall, the venture’s livelihood can be boiled down to two bare minimum hurdles. First and foremost, the broader resort must be able to cover its debt service. Second, the most influential HOA members must keep faith in the resort owner. The resort owner and the HOA are married in a sense, and the broader resort’s economic health is the only lasting measure of the parties’ trust in one another.

Turnaround Case Study: An Economic Evaluation

The following case study concerns a 150-room, luxury, full-service resort located at the base of a world-class ski mountain, offering guests ski-in/ski-out access. The resort opened in 2007 at a cost of approximately $1.5 million per unit, or a total of $225 million. Developed by a partnership of high-wealth individuals, the property has 50 dedicated hotel rooms and 100 units structured as whole-ownership condominiums. The 100 residential units have an average size of 2,500 square feet, for a total of 250,000 square feet available for third-party ownership. The resort was originally affiliated with an ultra-luxury operator based in the Far East, with a high pedigree but limited distribution. Public facilities include three food and beverage outlets, 10,000 square feet of meeting space, a full-service spa with ten treatment rooms, and a retail arcade.

The following case study concerns a 150-room, luxury, full-service resort located at the base of a world-class ski mountain, offering guests ski-in/ski-out access. The resort opened in 2007 at a cost of approximately $1.5 million per unit, or a total of $225 million. Developed by a partnership of high-wealth individuals, the property has 50 dedicated hotel rooms and 100 units structured as whole-ownership condominiums. The 100 residential units have an average size of 2,500 square feet, for a total of 250,000 square feet available for third-party ownership. The resort was originally affiliated with an ultra-luxury operator based in the Far East, with a high pedigree but limited distribution. Public facilities include three food and beverage outlets, 10,000 square feet of meeting space, a full-service spa with ten treatment rooms, and a retail arcade.

Note: In this case example, the subject property and its economic parameters are entirely fictitious. Although the various characteristics assigned to the resort are meant to read as realistic, any marked similarity to an actual existing resort perceived by the reader is strictly coincidental.

The resort was a modest success until the onset of the 2008/09 recession. The hotel component struggled to generate an operating profit, but 25 of the residences were sold at prices that represented the peak of the competitive market. The recession, coming on the heels of rapid supply growth in the region, had a devastating impact. A receiver was installed and the property was sold out of foreclosure in 2012. The new owner, a private investment firm with luxury holdings worldwide, acquired the resort for $90 million, or 40% of the construction cost, and devoted the next two years to stabilizing the hotel operation and completing the $10 million in renovations necessary to convert the property into an alternate ultra-luxury brand with broader distribution and market awareness, which took over management in late 2014.

The brand/management conversion was a game changer, and the resort’s average rate improved by 25%. Prospects for the sale of the residential units also improved. A highly regarded brokerage firm with extensive regional experience was hired to resume the sell-off. The marketing program commenced in the fall of 2015, continuing through the peak of the 2015/16 season. The strength of the brand and the quality of the product, combined with the fact that new supply remained in check during the post-recession up-cycle, allowed the sell-off program to gain sufficient traction. As of the evaluation date, July 1, 2016, ten units were closed over the past nine months, and another ten were under contract and scheduled to close within the next three months. The sales team expects the 65 unsold units to sell within three years.

The broker anticipates unit pricing levels to rise as units become scarcer. Five of the original buyers have put their units on the market for resale, at prices consistent with those of the unsold units. The HOA is especially enthusiastic about the brand conversion. The new operator has an exceptional vacation-ownership program, and the current sales prices reflect a premium of roughly 25% relative to the initial sell-off pricing. The following table identifies the sell-off projections and the valuation of the associated income stream.

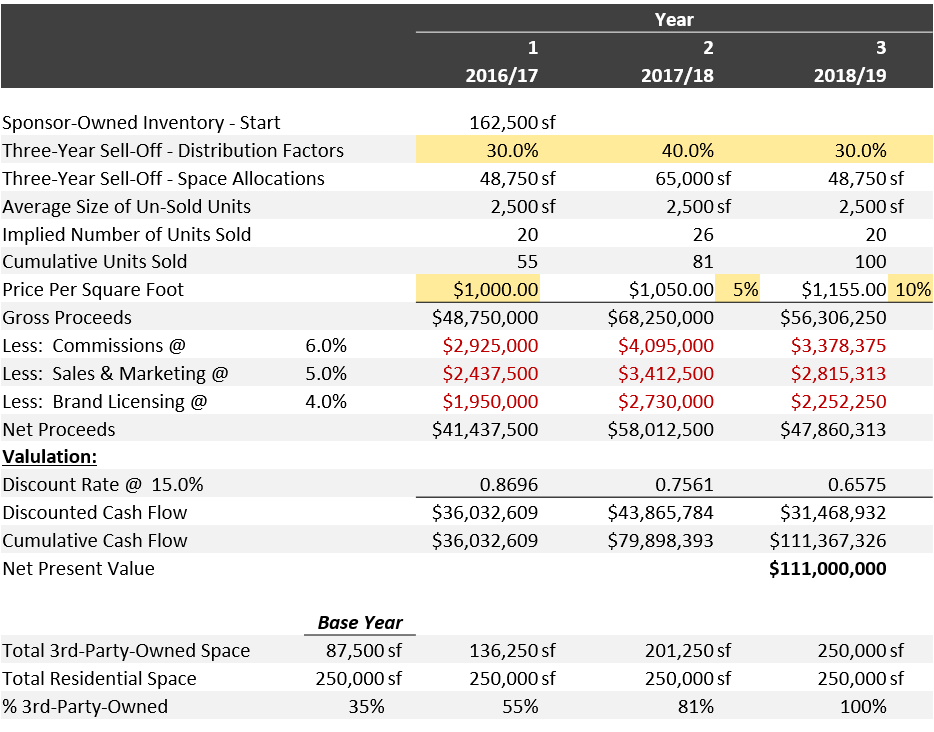

Net Present Value of Projected Sales Proceeds

Source: HVS

As of the evaluation date, the resort owner (also referred to as the Sponsor) controlled 65 of the 100 residences, or 162,500 square feet of the 250,000 square feet available for sale. The consultant hired to evaluate the project estimated that the remaining 65 units and 162,500 square feet would be sold off by the end of the third year, and that the weighted average unit price would accelerate as the sell-off process nears completion. Deductions are taken for commissions, sales and marketing, and licensing fees, all tied to gross proceeds. The net proceeds are then converted into an estimate of value using a discount rate of 15%, a figure intended to account for the risk and return factors. The figure is derived from discussions with investors active in the luxury resort category.

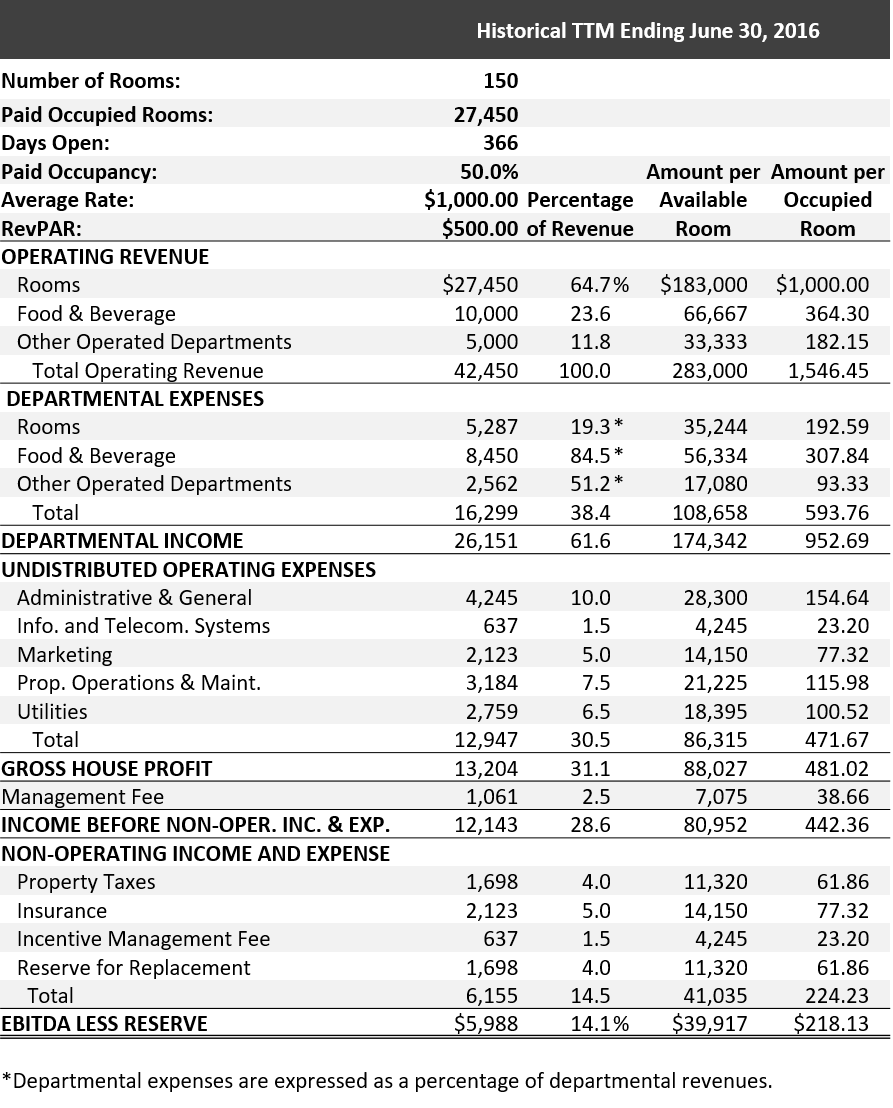

The evaluation of the ongoing resort operation is more complicated and begins with a review of the property’s operating history. The following table identifies the results for the year ending June 30, 2016, prior to the revenue- and expense-sharing distributions associated with the HOA and rental management programs.

Historical Income and Expense

Source: HVS

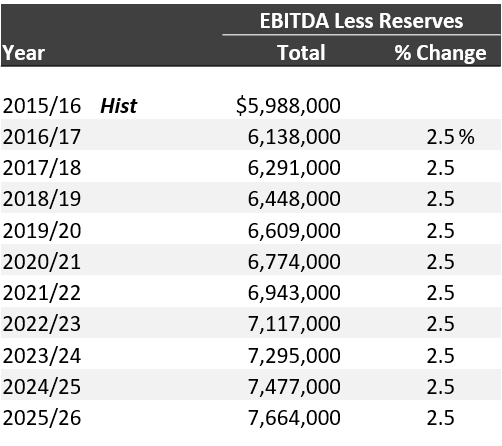

The operating history is a reasonable basis for projecting future unadjusted operating income levels, with inflationary gains of 2.5% per annum projected over a ten-year holding period. The net income forecast follows.

Forecast of EBITDA Less Reserves

Source: HVS

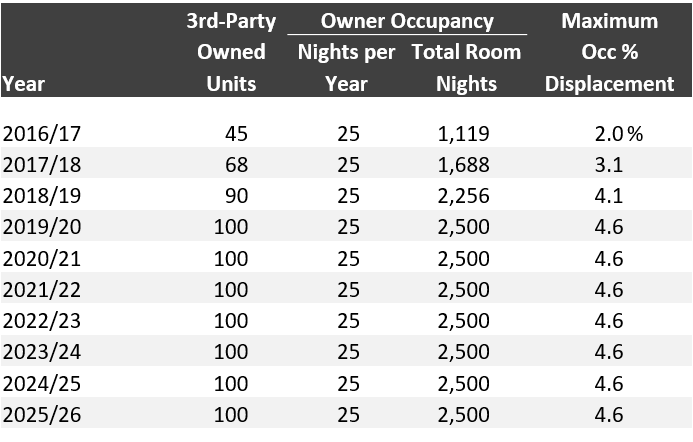

Adjustment for Unit-Owner Occupancy

The first adjustment is necessary to account for the impact of occupancy displaced by the unit owners’ occupancy. Assuming the unit owners continue to occupy their units at a rate of 25 nights per year, the following table calculates the maximum occupancy-point displacement level for the 150-room operation.

Maximum Occupancy Displacement Forecast

Source: HVS

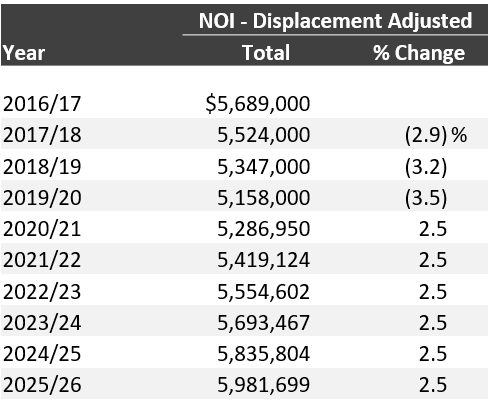

In order to realize the above-average returns available on their investment during peak demand periods, most unit owners occupy their units during shoulder and off seasons. As such, the downward adjustment to occupancy is somewhat moderated. Using the income-and-expense forecast structure associated with the actual performance for the trailing-twelve-month (TTM) period ending June 2016, we revised the forecast to account for a stabilized downward occupancy adjustment of three points. The following “displacement-adjusted” income forecast reflects the results.

Displacement-Adjusted Income Forecast

Source: HVS

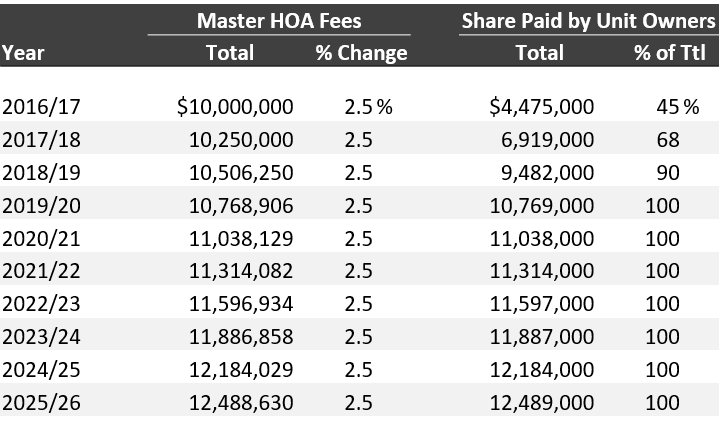

HOA Expenses

The next adjustment pertains to the HOA expense reimbursement. The HOA expense allocated to the residential units is budgeted at $10.0 million for 2016/17, with inflationary gains projected each year thereafter. The portion of this expense that is paid back to the resort depends on the amount of the residential space owned by third parties, expressed as a ratio to the total residential building space. As of the start of the forecast period, the ratio is 35%, but this is projected to increase to 55% by year’s end; thus, the average is 45%. The allocation is 100% in the fourth projection year, the first year in which all residential space is owned by third parties. The HOA reimbursements are calculated as follows.

HOA Reimbursement Forecast

Source: HVS

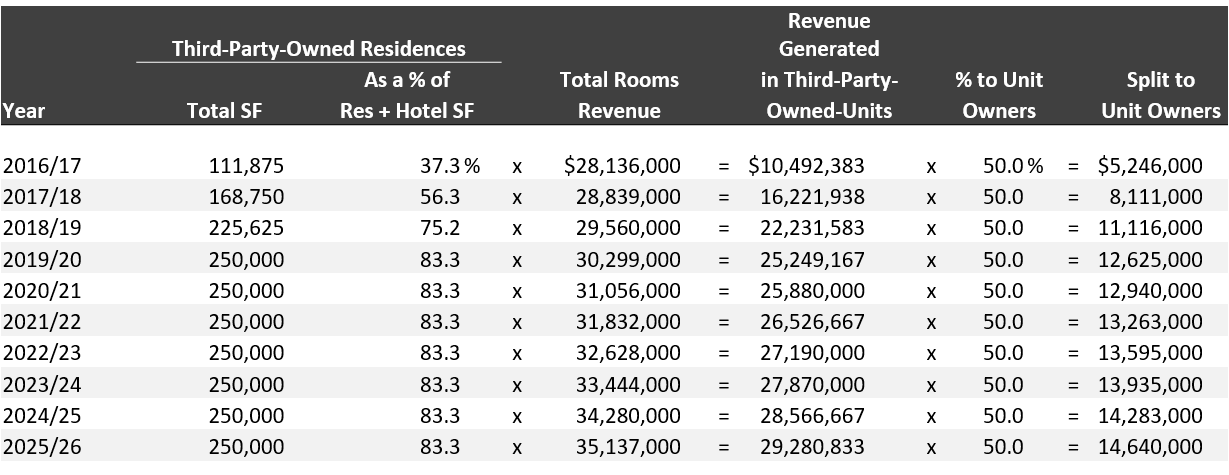

Rooms Revenue Split

The following table details the basis for the rooms revenue allocation payable to the unit owners. The first step requires a calculation of the portion of the rooms revenue that is generated in the third-party-owned units. The ratio is calculated as a percentage of the total building space located in the 250,000 square feet of residential units, plus another 50,000 square feet located in the 50 hotel rooms. Thus, this ratio is maxed out at 83.3% (250,000 ÷ 300,000). Once we derive the rooms revenue generated in the owned units, we can calculate the contractually stipulated share payable to the unit owners.

The following table details the process.

Forecast of Rooms Revenue Split to Unit Owners

Source: HVS

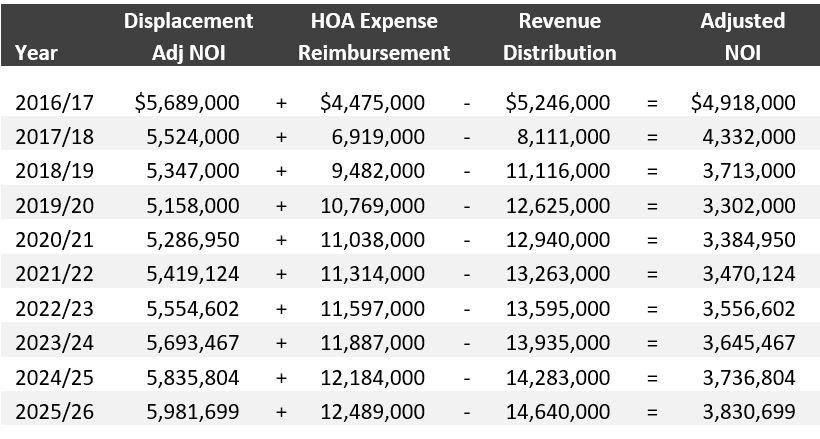

Net Operating Income

In the following table, the initial net operating income (NOI) forecast is adjusted to reflect two things: first, the addition of the expense reimbursement, and second, the deduction of the revenue split payable to the unit owners.

Adjusted NOI Forecast

Source: HVS

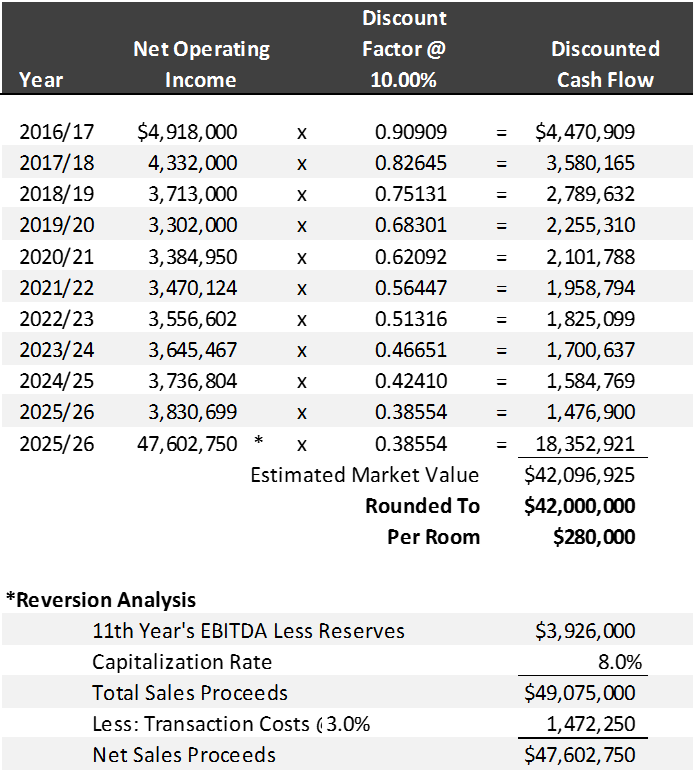

Next, we convert the adjusted net income into an estimate of value using a discounted-cash-flow analysis. The discount rate and terminal capitalization rate are intended to account for the risks and return factors. The selected discount rate needs to reflect the risk of the rental program and the durability of the income stream. Moreover, investors often apply different discount rates to the income generated by the real estate that they own and control versus the RMP income they earn from the real estate that others own, which can be removed from a rental pool. For simplicity in this presentation, we have used a single discount rate.

Discounted Cash Flow for the Ongoing Resort Operation

Source: HVS

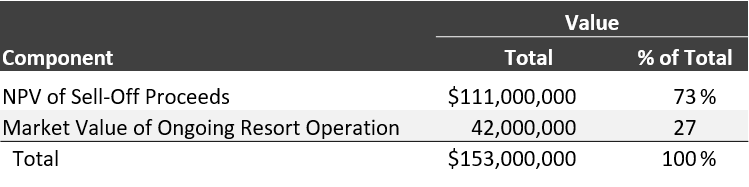

The sum of the net present value of the sell-off proceeds and the discounted cash flow of the ongoing resort operation represents the total property value, calculated as follows.

Total Property Value

Source: HVS

The sum is $153 million, with nearly three-fourths of the total value realized through the unit sell-off. As compared to the ongoing resort operation, the sell-off projections are subject to greater speculation. As such, the allocations reflect the risk associated with investment in the project. Nevertheless, the evaluation is favorable from the perspective of the second owner for two reasons: 1) the total property value is 53% higher than the cost basis (acquisition plus renovation) and 2) the gap between the market value and the original development cost suggests that there is a prohibitive barrier to entry in terms of the economics for projects of this scale and quality level.

Conclusion

The preceding analysis is simplified in several respects. For example, incentive-management fees are invariably a complicating factor, subject to complex calculations; in this analysis, the fees have been projected as a simple percentage of revenue. The cursory analysis is intended to provide a broad sense of the issues associated with an evaluation of a destination resort with a real estate ownership component.