Private Student Housing has emerged as a mainstream global asset class worth an estimated €180 billion. While the USA and the UK are currently well-established as markets for student housing investments, the European market remains relatively unexploited and a popular choice among investors. Greek market is considered to be in its infancy since the first purpose-built student residences were constructed only a couple of years ago. Many of the information presented in this report regarding global trends were extracted from other reports conducted by professional firms on the subject matter.1, 2, 3, 4, 5, 6

Highlights

- The world student housing sector reached a high of €14.4 billion of investment from June 2014 until December 2015. Transactions in the UK, the most active market, bounced from €2.4 billion to €6.7 billion during 2015, while in the USA, considered to be the most mature student accommodation market, the volume of activity totalled €6.8 billion between June 2014 and December 2015.

- In 2014, global higher education students amounted to 176 million while this number is estimated to reach 263 million by 2025. University students are increasingly international and mobile. Global student mobility is constantly gaining ground, with students studying abroad forecast to grow to 8.0 million by 2025 from 4.1 million in 2010.

Student Housing Market Overview

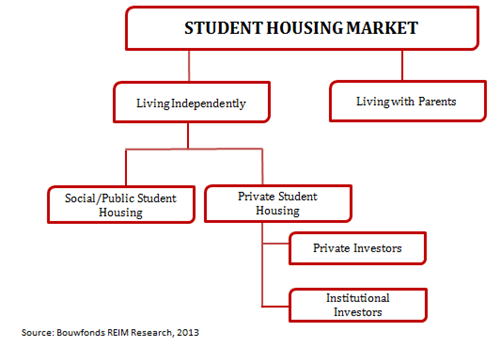

FIGURE 1: GENERAL STRUCTURE OF THE MARKET

In a world which is constantly changing and millenials are picking up the slack from the previous generations, new needs and expectations have emerged like that of a totally different model of student residence which will fit the profile of the modern student who demands a positive living experience within a supportive, safe, and fun environment. Since higher education constitutes a much greater expense than it did in the past – and consequently a much more considered decision by parents and students – but also as students want to live in a place which would enforce their independence and make them productive, the proccess of finding the right type of accommodation has become crucial. Figure 1 provides a simplified overview of the ownership structure of the student housing market. A clear distinction can be made between public ownership and private ownership, although the definition of the ‘social sector’ differs amongst countries.

By far, the largest part of the student housing market worldwide is owned by private (often non-professional) investors, who implement an operating model comparable with conventional housing: the tenant pays the owner a monthly amount for an unfurnished room. In principle, the contract is for an indefinite period. Professional investors also work according to these kinds of operating models. In these cases, the accommodation is comparable to ordinary one-bedroom apartments. In this sector, supply is higly diversified, while private flats vary in size, comfort, rent price, and construction quality.

On-campus accommodation is only available to students who are enrolled at a university. Social housing companies also impose specific student requirements, generally an income criterion, before a student can rent student accommodation. After graduation, students are no longer permitted to stay in their student lodgings. In most cases, and especially in Europe, most of the buildings which serve as public student residences face a serious degree of obsolescence due to poor maintenance.

A third, limited group of suppliers, on which this report is focused on, is that of the professional real estate investors. There are several specialised investment companies active in this field, especially in the USA and the UK. These companies provide students with modern, well-furnished studios and/or apartments which vary from high-end luxury housing to more moderately-priced accommodations. This type of student housing very often resembles that of a hotel as the building usually features some additional shared services such as a fitness room, a meeting room, a kitchen or other facility depending on the culture of each country. In this model, the owner is usually not the operator as the building is rented to a special operator for a fixed amount who is responsible for setting rents, attracting tenants, and dealing with the rules and regulations of the building. The model of the student housing of the future could be even more diversified by offering more than just living spaces. Housing properties can incorporate recreational and retail space to facilitate life for students but also increase their revenue potential.

Nowadays, when universities compete to attract a higher number of students, apart from factors like location and structure of their academic programs, student housing is also included in the main topics of their strategic planning for expansion and awareness. In the face of rising housing cost levels close to universities and since today’s university applicants are looking for an experience-based academic life, housing has moved from a basic need into a vital strategic asset for universities.

Even though the purpose-built student acccommodation (PBSA) has become a top-class investment, due to the sector’s rapid growth – that is underpinned by the active rise in student numbers worldwide – there is still a shortage in supply of qualitive student housing in many major cities.

The student housing sector has evolved into a mature and globally-recognised investment. Global student transaction volumes increase year by year, while ownership is moving away from private developers towards large-scale institutional investors, such as equity funds, sovereigh wealth funds, pension funds, investment managers, and REITs, hence revealing the maturity of the market.

The key appealing attributes of the sector, according to a recent report by a reputable financial and professional services firm, are :

- Relatively stable income and solid rental growth as the sector delivers relatively secure and steady rental growth above inflation rates;

- Resilient, less cyclical performance as the student housing market stays relatively unaffected by macroeconomic factors. More specifically, the sector’s ability to perform well in economic downturns was proven during the recent economic turndown as there was a surge in student numbers globally due to the deficit in jobs and the recessionary tendency for employees for further expertise took hold;

- Constant supply and demand imbalance as historically-increased demand conditions outpaced supply, causing a significant gap in the market and pushing rents of existing properties at higher, and sometimes unjustified, levels;

- Strong demand is reflected in high occupancy rates. Private student housing investment demonstrated its resilience during the economic turndown as many facilities were operating close to full occupancy.

Mature Student Housing Markets

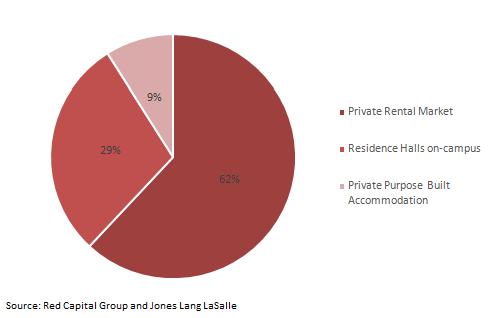

FIGURE 2: STUDENT HOUSING PROVISION - USA 2011

The USA and the UK are home to the most mature markets when it comes to private student accommodation investment activity. This can be attributed to the fact that demand for studying in these countries has been exceptionally high compared to others as education is conducted in the English language. In general, countries where English is the language of instruction (USA, UK, Australia, and Canada) have become dominant student destinations. Consequently, the rise in demand for English-speaking higher education has led several universities in non-English speaking countries to offer courses in English in order to attract international students. Other reasons for the rising of the specific market in these countries is that traditionally English-speaking nations tend to showcase some of the most well-developed and sophisticated real estate markets but also universities in these countries are considered to be the leading education providers worldwide.

The USA has been the leader in the PBSA market since its emergence in the early 1990s. The sector was developed in response to outdated on-campus accommodation coupled with the growing demand from domestic and international students seeking superior living space. The US market is characterized by a huge higher education population (totalling 20.6 million) and its reputation as top destination for foreign students. Reflecting this maturity, some investors now see the sector as more tapped than newer markets. This has slowed recent activity and led to a decline in investment volumes since 2012.

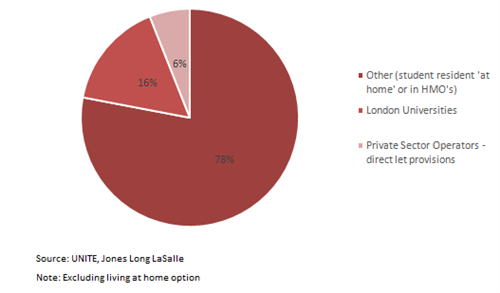

FIGURE 3: STUDENT HOUSING PROVISION – LONDON 2011

Investment in the UK student housing exceeded that of the USA for the first time in 2013. The growth of the UK sector has been driven by the consolidation of portfolios funded by cross border investment, which accounted for 72% of activity by volume in 2013. The majority of this capital originated from the USA, the country with the longest track record in the sector. The Americas contribute 54% of all cross-border investment outside their home country globally, with Asia and EMEA equally sharing the rest. The sudden awakening of investments in this sector has led to yield compression in the market – with yields on London PBSA hardening from 6.3% in 2012 to 4.5% in 2015, reflecting both robust land value appreciation and intense competition between investors who desire to enter this profitable market.

Despite the fierce competition in these markets, there is still room to grow and the potential for further investments has not reached its ceiling since the number of international students continues to rise. However, the pace of growth will not be as high as in the last five years as there are a lot of factors inhibiting the continuous rise such as the congested market in both countries or the tougher immigration rules on student visas that will most probably be imposed for all students outside the UK, after the outcome of the recent British referendum which was in favor of the UK leaving the European Union.

Student Profile and Demand Drivers

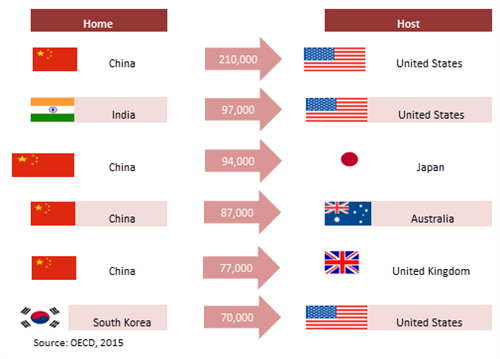

Due to its strong economic growth, Asia is the main source continent for international students. Over the last years, countries like China, India, and Vietnam experienced rapid growth in the wealthier middle class which fuelled demand for higher education. Since the quality in education in these countries was quite low compared to the desired level of education that the applicants wanted to obtain, they started looking overseas for recognised universities which offer courses in the English language. In 2009, over half (52%) of international students in OECD destinations (which capture the bulk of global demand) came from Asia, followed by Europe (23%), Africa (12%), South America (7%), North America (4%), and Oceania (1%).

FIGURE 4: LARGEST INTERNATIONAL FLOWS OF STUDENTS

International students have become more mobile and choose their preferred study destination based on several criteria, the most critical of which are: the quality of education, the language of instruction, housing options, cost of living, visa regulations, distance from home country, future employment options, and fees.

Growth Opportunities

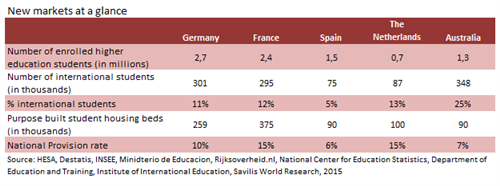

FIGURE 5: NEW MARKETS AT A GLANCE

Apart from the well-established and reputable markets, like the UK and the USA, there are several other markets with solid demand conditions that are underserved by quality student housing, where the sector is either in the early phase of development or still immature like Australia or continental Europe. These markets offer significant untapped potential for investment as they are free from concerns such as high tuition fees and often offer an affordable cost of living compared to the mature markets. Having realised the alluring and determinant factor of English language as the language of instruction, most of the institutions have introduced plenty of English-taught degrees while they constantly try to upgrade the quality of offered education and climb up some positions in the global ranking system. The majority of investments in these countries has stemmed from private domestic capital; international investors are getting ready to enter the game.

The top five countries, outside the UK and the USA, where the student housing investment market is flourishing are Germany, France, Spain, the Netherlands, and Australia. Germany has seen a rapidly growing development and investment market as the number of students increased by 36% in the last decade while it is characterized by a decentralised student market where well-established universities are scattered throughout the country. France is considered by a large number of students as a very appealing study destination as Paris is ranked number one student city in the world by QS, a report compiled by higher education data experts. Factors like low tuition fees and well- regarded institutions provide the French capital with an additional advantage. The Netherlands is considered as one of the fastest maturing markets as it was the first European country to fully incorporate English language in most of its universities while the rapid growth in international students – due to the country’s fresh approach towards the new generation – has aroused investors’ interest. Spain is the newest player in Europe’s student housing market. There is an increasing foreign demand and as part of the country’s strategic plan to attract more students, a target is set that one third of the university courses will be offered in English by 2020. There is high investment potential as the country is seriously undersupplied in terms of PBSA. Finally, Australia has seen the number of international students, and especially Asians, grow due to its globally-recognised level of education and its enviable quality of life. By 2020 the total number of purpose-built beds (in 100+ bed accommodation buildings) is expected to exceed 100,000. Figure 5 depicts the current situation in the student housing market in these emerging countries.

Purpose-Built Student Accommodation in Greece

Market Overview

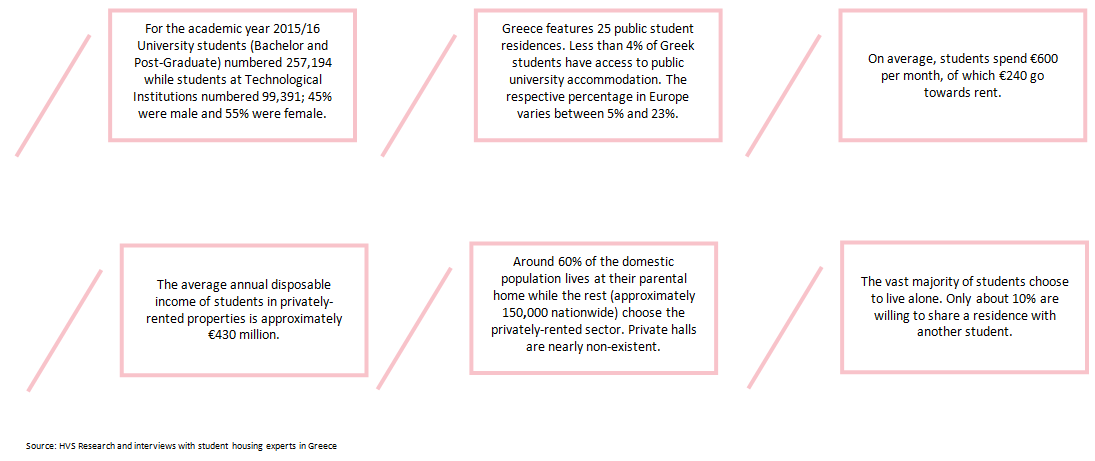

PBSA in Greece is still in its infancy compared to other emerging European markets and global investors think of it as a market with no significant interest as the number of international students is quite low. Even though there are great investment opportunities for potential domestic investors which lie in established university cities featuring high mumber of domestic students, low provision of student housing and poorly-maintained buildings, this sector still remains unknown to them. It is a fact that investments should be made after considering and researching each city independently as study destination and evaluate its ease of assess to attract students. Greece is characterised by a wide range of universities located all over the country with some of them enjoying European recognition. Smaller cities with low housing provision have become renowned study destinations, especially for domestic students. Since the beginning of the recession, as in many other European countries, youth unemployment has soared as more people in their effort to increase their level of expertise in this competitive market have sought higher education. Traditionally, due to cultural influences, students in Southern Europe tend to live or study in their home town and the majority of them choose not to leave their guardian home. Even though this phenomenon was enhanced since the beginning of the financial crisis as families could not afford the cost of renting an extra property, there are still places where low market risk coupled with the shortage in modern and affordable rooms could create the appropriate conditions for investing.

While private student accommodation is becoming a marketable option in many European countries, it still remains an unexploited investment choice in Greece. Investors should look into this oppurtunity after taking into consideration some critical factors. The main reasons why private student residences remains an unknown product within the Greek market are considered to be the following:

- Investors are not fully aware of this type of product

- Lack of specilization and competent administration of these properties by Greek professionals

- Shortage in English-offered courses which could attract international students

- Uncertainty of Greek economy

- Unstable tax legislation

- Lack of appropriate legal framework concerning private student accommodation

- High competitive level within the student housing market

- VAT during construction period is not deductable, thus raising the initial investment

- Non-subsidized investments

Facts and Figures

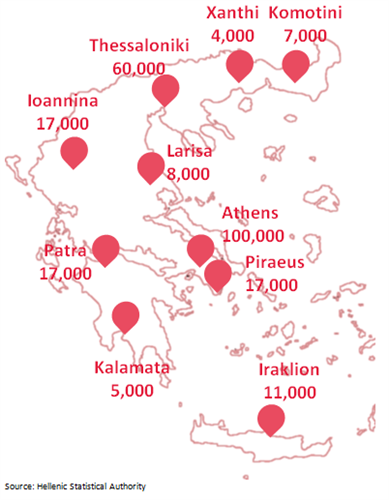

Main Study Destinations in Greece

Figure 6 illustrates the dominant study destinations in Greece according to the number of enrolled students. The cities depicted constitute target cities for potential investors in the Greek purpose-built student accommodation market.

FIGURE 6: NUMBER OF STUDENTS IN TARGET CITIES

Indicative Rental Prices of Private Properties in Main Study Destinations

The rental prices of flats owned by private (often non-professional) investors are determined by various criteria such as the popularity of the destination, the location within the city, the size of the flat, the age of the building, any recent renovation that the property has gone through, and any extra offered facilities (the type of heating, the existence of A/C units or any other electrical appliances, and storage space). According to a research conducted by CNN Greece, the indicative rental prices of private properties destined to be used as student residences are the following:

- In Athens and more specifically in the district of Zografou, the most common area chosen by students to live due to its proximity to most universities, prices fall between €150 and €210 for studios and €220 and €270 for a bigger apartment, while the corresponding prices for flats located in the city center range from €220 to €250 and €250 to €330. In other popular student districts like Ampelokipi, Goudi, and Egaleo, prices start from €155 to €190 and €180 to €250, respectively. In Pireaus, prices range from €200 to €230 for studios and €240 to €300 for bigger apartments.

- In Thessaloniki, prices for studios measuring 25 – 30 m2 fall between €180 and €340 depending on the quality of construction and the facilities included, while studios ranging from 40 to 60 m2 have a starting price of €250; this increases as the distance between the property and the university becomes smaller. For bigger apartments, prices fall between a broader spectrum, starting from €300 and reaching €600.

- In Volos, prices for properties built around 30 to 35 years ago range between €160 and €180 while the corresponding prices for most recent constructions start from €180 to €200. For bigger apartments, prices fall between €230 and €300 depending on the age of the building.

- In Chania, prices for new studios start from €260 to €350 while for older constructions prices range from €200 to €220. Concerning this specific destination, there is a need for more student residences as the flourishment of tourism and the development of Airbnb as a philosophy has pushed a lot of private owners to provide their properties to incoming tourists rather than to students, leading to unaccommodated student demand. The reason for that is that tourists are willing to pay a much higher amount than students, while Chania’s seasonality pattern is a mixture of an island’s seasonality pattern – characterized by intense but short visitation volume – and a city’s seasonality pattern – characterized by mild but prolonged visitation volume – has led private owners to take advantage of this opportunity in the most effective way.

- In Patras, prices for studios range from €160 to €210 while for bigger apartments prices start from €180 and may reach €280.

- In Larisa, Ioannina, and Xanthi the corresponding prices are €160 - €210 and €170 - €260, €130 - €170 and €160 - €220, and €160 - €180 and €280 - €210, respectively.

Prominent Private Student Residences in Greece

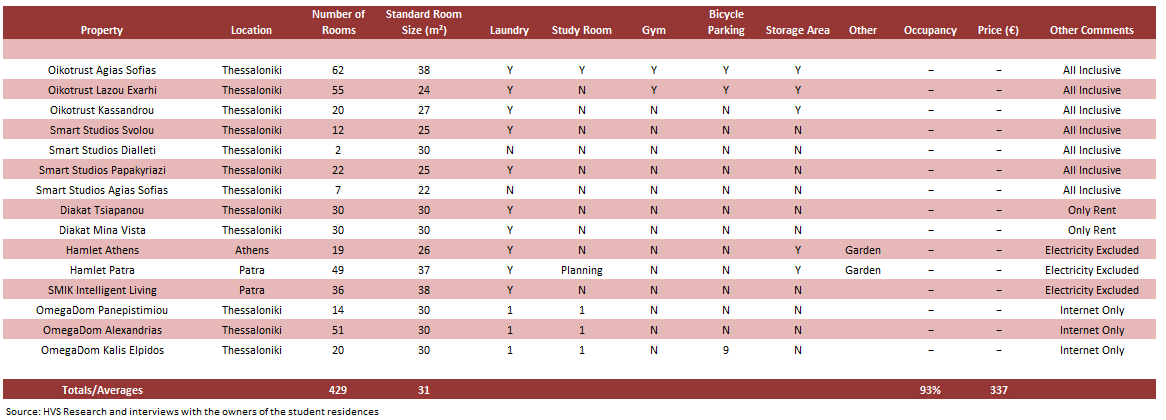

FIGURE 7: MARKET AREA ANALYSIS – PRIVATE STUDENT HOUSING

During our research we found a very limited number of private halls within Greece complying with European standards that have been set in the PBSA market. Through interviews we conducted with owners, we gathered information about their

operating model. For legal reasons we are unable to show the individual units’ operating data from which the aggregate numbers are derived. We contacted the owners of four student housing residences in Thessaloniki: Oikotrust, OmegaDom, Smart Studios, and Diakat. Each brand operates more than one building located in various parts of the city. The total number of student rooms available in Thessaloniki is 325, the highest number of rooms than in any other city in Greece, while the price of rent differs depending on the included facilities, the offered communal amenities, and the age of the building. Although Athens, features the highest number of enrolled students on a national level, the prοvision of student housing accommodation is not substantial. During our research we found only one property featuring 19 rooms under the brand “Hamlet Athens” located in the city center that caters for the needs of students who look for a private residence in a student environment. The list with the cities that have entered the PBSA market in Greece ends with Patra which hosts two of the newest private student residences in the country; Hamlet Patras, owned and operated by the same team as Hamlet Athens, and SMIK Intelligent Living. Together they feature 85 rooms in total, fully furnished and equipped, large communal areas, broadband internet, and laundry facilities. Figure 7 lists the PBSA properties in Greece and their individual characteristics. The total number of rooms is 429,

|

HAMLET RESIDENCES IN KIPSELI, ATHENS |

HAMLET RESIDENCES IN PATRAS |

|

|

|

OIKOTRUST IN THESSALONIKI |

SMIK INTELLIGENT LIVING IN PATRAS |

|

|

Reasons to Invest

- Given the current situation in the domestic housing student market which is still in its infancy, Greece could be considered as a trully ‘virgin’ marketplace in which sophisticated investors could try to replicate models that have been pursued succesfully in other mature markets. Some of the reasons why someone would find the idea of investing in Greece appealing are the following:

- Since competition is quite low, there are unprecedented opportunities for an operator to build new quality accommodation or convert an existing building, even with limited capital requirements.

- Greek student mobility to European universities has decreased, so there is plenty of room for investors to attract tenants from the domestic market.

- Occupancy rates in the existing limited number of PBSA residences are extremely high and reach nearly 100% annually with long waiting lists.

- Yields in the student housing market are considered to be very attractive and may reach 10-15% globally while on a national level they are likely to reach up to 9%.

- Low asset values combined with a steady rental income, which is less prone to political and economic changes, should most probably deliver long-term satisfactory returns.

- Strong demand and limited supply: state university halls account for less than 3% of the total needs, while the private rental sector is overpriced and most of the times the infrastructure is poorly maintained.

- PBSA is a global trend always looking for fresh markets to enter and always rewards the pioneers in each market.

Conclusion

Around the world, students are looking for quality housing that will enhance their academic and social experience. Purpose-built student accommodation has been introduced as an investment activity to fill in the gap between undersupply of quality housing and the growing number of students looking for a place that will inspire them to fulfill their educational goals. With transaction volumes reaching several billion dollars globally, student accommodation is no longer a niche market but has been recognized as a major asset class. The USA and the UK markets are considered as the world’s most mature ones supported by a huge number of students who consider them as the top destinations to study. Considering this maturity and the fact that these markets may have reached their full potential, investors are now looking for fresh markets where they can satisfy their investment appetite. Major European countries and Australia are now the places where significant untapped potential is presented. While Greece is not amongst the countries with an appealing profile for international investors, the sector has been pioneered by local business people who have foreseen the growth potential in this sector. The current state of the Greek economy and the property market create the ideal conditions for investment oppurtunities which lie in established university towns with low housing provision, where domestic or Erasmus students are looking for quality, secure and service-oriented product that will be in line with what is offered in the rest of the world.

1 Jones Lang LaSalle. (2012). Advance – Student housing: a new global asset class.

2 Savills. (2014). Spotlight World Student Housing. London, UK.

3 Savills. (2015/16). Spotlight World Student Housing. London, UK.

4 Bouwfonds REIM. (2013). Investing in European Student Housing. The Netherlands.

5 Cushman & Wakefield. (2015/16). UK Student Accommodation Report. London, UK.

6 Savills. (2013). Spotlight European Student Housing. London, UK.