The Subject Hotel

The subject property is a branded four-star hotel in the urban core of a first-tier American city. It contains 300 rooms, two food and beverage outlets, ±20,000 square feet of meeting space, and a health club and spa with five treatment rooms. The date of value is April 1, 2013. During the twelve months ending February 28, 2013, the subject property realized an occupancy rate of 70% and an average daily rate of $275, resulting in a RevPAR (revenue per available room) of $192.50. The hotel is located on leased land. The ground lease has 80 years remaining on it and mandates annual ground rent equal to 3.0% of total hotel revenue.

The hotel is 20 years old and is being appraised for purposes of a refinancing. A portion of the financing proceeds will be used to fund the $15 million in renovations that are necessary for the property to continue to conform with the brand’s product standards. The appraisers have been engaged by a prospective lender in order to develop an opinion of the subject property’s “as is” market value.

The Adjustment Grid

The following grid details the calculations applied in order to adjust four selected sales for direct comparison with the appraised interest in the subject property.

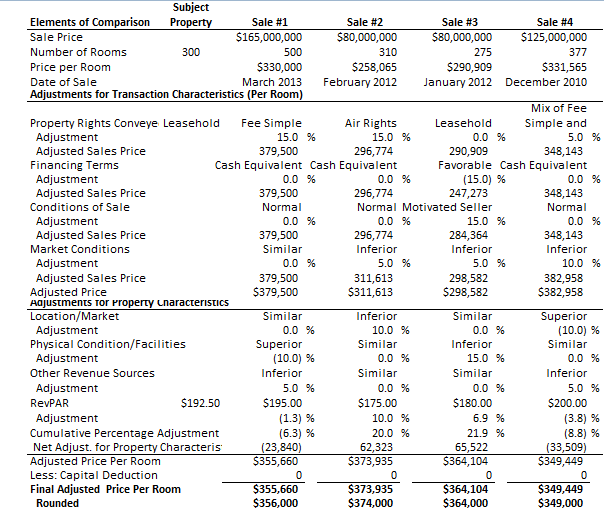

FIGURE 1

COMPARABLE SALES ADJUSTMENT GRID

ADJUSTMENTS FOR TRANSACTION CHARACTERISTICS

Adjustments for transaction characteristics are applied on a linear basis (i.e., item-by-item, as opposed to cumulatively, as is the case with the property characteristic adjustments), consistent with standard appraisal industry practices.

Property Rights Conveyed

The hotel is located on leased land. The ground lease has 80 years remaining on it and mandates annual ground rent equal to 3.0% of total hotel revenue. In order to determine the impact of the lease on the property’s total value, the appraisers ran another iteration of the income capitalization approach methodology, but without the ground rent deducted from the income stream. In addition, the investment parameters used in the discounted cash flow analysis were slightly more stringent under the leasehold valuation, considering that the land is subject to less risk than the real and personal property components. Thus, if the land value is excluded from the valuation due to the ground lease, the investment parameters should be adjusted upward. In the fee-simple iteration of the subject’s valuation, the investment parameters are adjusted down. Comparing the leasehold and fee simple valuations, we conclude that the subject property’s market value is reduced by 15% due to the presence of the ground lease.

In the case of Sale #1, which involved a fee simple transaction, the full 15% adjustment is warranted. Sale #2 involved a hotel constructed over an underground highway and use of the land was granted subject to a 125-year air-rights lease with an annual rent of $1, paid to a municipal highway commission. Based on these terms, the property rights are essentially fee simple. Thus, the full 15% adjustment is warranted. The hotel transferred as part of Sale #3 is also located on leased land, subject to ground lease terms similar to those of the subject property. Thus, no adjustment is warranted. Sale #4 involved a hotel constructed on land owned in fee, but property ownership leases space in an adjoining structure for its meeting facilities. Discussions with parties to the sale indicate that the meeting space rent is approximately $500,000 per year, which based on the overall cap rate associated with the sale (7.0%) removes approximately $7.0 million, or 6.5% of total value from the property, was the space owned in fee. This lease will expire in 20 years and although it may be renewed, there is no guarantee; thus, an additional adjustment factor is warranted in order to account for the risk to the property associated with the potential loss of its meeting space. Overall, we would estimate a 10% downward adjustment is warranted. Against the 15% adjustment associated with the subject property’s lease, a net upward adjustment of 5% is applied in the case of Sale #4.

Financing Terms

With the exception of Sale #3, each of the comparable sales were paid for in cash or cash-equivalent terms. The seller of the hotel sold as part of Sale #3 financed the sale, subject to an interest rate 1.50 percentage points below current market levels, but a 70% loan-to-price ratio, consistent with market standards. Multiplying 1.5 by 70%, the overall capitalization rate indicated by the sale, 6.0%, should be adjusted upward by 1.05 percentage points, to 7.05%. The revised price is 15% lower than the actual transaction price. Thus, this sales price has been adjusted downward by 15%.

Conditions of Sale

With the exception of Sale #3, each of the comparable sales involved “arms-length” transactions with normal conditions of sale. The seller of the hotel sold as part of Sale #3 was motivated to sell the property quickly in order to raise cash for a high-yield investment opportunity. The seller had the option of allowing for a longer marketing period and achieving a market-rate sale. As such, an upward 15% adjustment is applied to offset the downward 15% adjustment associated with the financing terms.

Market Conditions

Adjustments for market conditions can account for two distinct sets of changes realized between the date of value and the date of each comparable sale’s transfer; 1) value appreciation or depreciation rates associated with changes in revenue and/or income levels, and 2) changes in the broader investment market, as far as the availability and cost of capital and related shifts in capitalization rates. As for the first factor, this is accounted for in our RevPAR adjustment factor, which is described in detail below. With respect to the second factor, no adjustment is necessary in the case of Sale #1, considering that it was transferred within one month of the subject hotel’s date of value. Sales #2 and #3 occurred in the first half of 2012. Since this time, market conditions have improved as financing has become easier to obtain and capital costs have declined. The same observation holds true for Sale #4, which closed in late 2010, with a greater adjustment warranted.

(Note that paired-sales data can be used to determine underlying appreciation/depreciation rates over a specific interim period, but this rate of change cannot necessarily be pro-rated and applied generally. For example, if the same property sold in April 2010 and April 2013 and indicated appreciation of 30%, or approximately 10% per year, the rate of appreciation may have been more rapid in the last year than the first two. The calculated adjustment is really only reliable for other sales closed within a few months of the first transfer. In addition, further adjustments would be necessary to account for any capital improvements or other internal changes in the interim period.)

ADJUSTMENTS FOR PROPERTY CHARACTERISTICS

Whereas the transaction characteristic adjustments are applied linearly, the property characteristic adjustments are summed into an aggregate adjustment, consistent with standard appraisal industry practices.

Location/Market

Adjustments for differences between the subject property’s location and market setting and those of the transferred property can be unnecessary if the RevPAR adjustment (described below) is applied. A valid argument can be made that among many other factors, RevPAR differences completely account for variations in location factors, including market context. On the other hand, even if the RevPAR adjustment is applied, an additional adjustment can be applied here. Barriers to entry and upside potential are the key considerations here. A subject hotel or transferred property can be located in areas with radically different rates of growth and/or new supply risk factors to the extent that additional adjustments are warranted. In addition, a hotel with an atypical site (e.g., within a national park, adjacent to an airport, or in a coastal area where new development has become illegal subsequent to the hotel’s development) can warrant an additional adjustment.

In this case study, we have used RevPAR adjustments, but have applied additional adjustments to Sales #2 and #4. The hotel transferred as part of Sale #2 is located in a warehouse district where redevelopment has been slower than was expected when the hotel was constructed. Although this disadvantage is reflected in RevPAR adjustment to a significant degree, we have applied an additional upward adjustment to account for the greater level of risk associated with investment in this location. In contrast, a downward adjustment is applied to Sale #4, considering that this hotel has the benefit of a waterfront location, offering atypical aesthetic advantages and a setting that will be challenging to replicate. In addition, the property is located in a city with a somewhat stronger reputation among institutional real estate investors.

Physical Condition/Facilities

Beyond the corrections implied in the RevPAR adjustment, an additional adjustment can be warranted to account for differences in physical condition, age, underlying construction, and facilities scope, in the event the appraiser determines that these factors are not fully accounted for by the RevPAR adjustment. In the case of Sale #1, the transacted hotel was opened two years prior to the date of value and its historical RevPAR level reflects a hotel that was still in the process of ramping up to a stabilized level. In addition, because it is newer, the property has a longer economic life remaining as compared to the subject hotel, which consideration is also not accounted for in the RevPAR adjustment. Thus, an additional downward adjustment is warranted. The inverse is true of the hotel transferred as part of Sale #3, which has a shorter economic life remaining, as compared to the subject hotel. An additional upward adjustment is warranted.

Correcting for this category is perhaps the most nettlesome among the adjustments described here due to the matter of pending capital improvements – planned at either the subject property or the transacted properties – and how this matter relates to the RevPAR adjustment. The basis for the RevPAR adjustments are the historical RevPAR levels. Thus, in the case of the subject property, the historical RevPAR figure does not reflect the economic benefits associated with the planned $15 million in renovations. Because our objective is to render an “as is” market value indication, we have two potential premises. We can either 1) adjust the sales for comparison to the subject property’s market value “as renovated,” and then deduct the planned expenditure in order to get to an “as is” market value, or 2) adjust the comparables sales to the subject property’s “as is” physical condition, obviating the need for a subsequent capital-improvement adjustment. If the first option is selected, upward adjustments in this category may be warranted if the subject property, after renovation, will have a substantially superior product quality relative to the comparable hotels. It is also possible that the subject property’s condition will be inferior to that of a comparable hotel, even following renovation, perhaps necessitating a downward adjustment.

Either premise is valid, so long as it is uniformly applied among the comparable sales. In this case study, we followed the second premise. As such, the fact that the hotels transacted as part of Sales #2 and #4 were also slated for substantial renovations subsequent to sale is not factored into the adjustment grid. Rather, the relationship between each of the comparable hotels’ historical RevPAR to their respective sales prices is consistent with the “as is” adjustment premise we’ve used here.

Other Revenue Sources

The subject hotel has a full-service spa with approximately five treatment rooms. Similar facilities are offered at the hotels transferred as part of Sales #2 and #3, but are lacking at the hotels transferred as part of Sales #1 and #4. The subject hotel’s spa makes a modest direct contribution as a profit center but allows for a premium to RevPAR performance because the spa improves the property’s broader appeal. The RevPAR differential is accounted for in the RevPAR adjustment, thus this adjustment is limited to profit center contribution.

RevPAR

The RevPAR adjustment has been referred to throughout this case study because it bears much of the burden of several of the other adjustments, including those relating to differences in market conditions, location, market setting, physical condition, age, and facilities scope. RevPAR (revenue per available room) is calculated either 1) as the product of occupancy and average rate, or 2) by dividing total rooms revenue by the number of available rooms. (The same figure will result.) As opposed to occupancy rate (rooms occupied divided by rooms available), or average daily rate (rooms revenue per occupied room), RevPAR is a more complete measure of a hotel’s revenue-generating performance because it accounts for both occupancy and average rate in a single measure. Because hotels are purchased and sold based on their ability to generate revenue and net income, a comparison and adjustment based on RevPAR performance is highly relevant. The adjustment is based on the percentage difference between the subject property’s historical RevPAR and that of the transacted hotel.

Capital Improvement Deduction

Our appraisal assumes that a $15-million renovation will be completed within one year of the date of value. The renovation will have a positive impact on the subject hotel’s RevPAR performance. Several of the transacted properties were also slated for renovation subsequent to sale, which would also presumably have a positive impact on these properties’ RevPAR performance. However, unless offsetting adjustments are otherwise built into the grid (consistent with “premise one” described above), factoring capital expenditures into the analysis skews the logistics of the RevPAR adjustment, which relies upon the relationship between historical RevPAR and the sales price. In consideration of these factors, we have restricted the analysis to exclude both the costs and potential economic benefits of the renovations of the subject hotel and the transacted properties (consistent with “premise two” described above).

One More Thing: Business Value?

The subject hotel is operated subject to a binding long-term contract with the branding company; thus, there are no franchise fees. In hotel industry parlance, this is known as a first-tier management contract. Consistent with typical first-tier management contracts, the subject agreement calls for a base management fee equal to 3.0% of total revenues plus an incentive management fee calculated as a share of net income left over after the owner’s priority return. The incentive management fee essentially substitutes for the royalty fee deduction that would apply if the property was not brand-operated. Historically, the base and incentive management fees result in a total annual deduction of approximately 5% of total revenues. The appraisers conclude that all income attributable to the business is removed from the subject property’s appraised interest. Because the management contract has another 40 years remaining in its term (including all extension options available to the operator), the value of the business remains under the control of the management company.

As for the comparable sales, each of the transacted properties are subject to either first-tier management contracts such as the subject property’s, or else the buyer assumed deductions for brand royalties and third-party management fees into their investment analysis.

Business value adjustments are rarely addressed in comparable hotel sales analyses. Our experience suggests that it is extremely unusual for buyers and sellers of investment-grade hotels to perceive and account for business value as part of the transaction process. In this regard, the market participants are following the lead of the lending sector, which doesn’t loan on business value. Standard hotel lender under-writing calls for deductions for base management fees, and either brand royalties or an incentive management fee, even where those particular income streams might be collected by the buyer. HVS recently performed internal analyses for a first-tier hotel company as part of its acquisition of a first-class hotel in a gateway US city. Despite the fact that this company would collect the income streams attributable to the business, their investment decision was based on a net income forecast that included a substantial management fee deduction, which income stream determines the level of debt financing that can be provided. The experience suggests that perhaps only in cases involving small hotels motels with either no brand or a down-market flag – where purchase prices are primarily based on a rooms revenue multiplier and the property is family run – is business value perceived by both the buyer and the seller. The consensus opinion on business value issues (expressed here) has been subject to some debate in recent years. Ultimately, however, consultants and appraisers are obliged to rely upon the perceptions and practices of actual hotel buyers and sellers, who act in concert with the lending community.

Conclusion

The sales comparison approach is typically used as a check against income capitalization approach, as opposed to serving as a primary valuation methodology. Comparable sales are useful and informative, but the number of adjustments necessary to create an equivalent expression of value are usually so numerous and challenging to objectively quantify that the approach’s utility is reduced. This article means to provide insight into the various bases for adjustment, and illustrate the most recent methodologies and logic.