Among major metropolitan hotel markets across the nation, Denver’s high-end hotels have staged one of the most impressive comebacks from the lows of the recession. RevPAR has risen steadily over the past 18 months, helping to rekindle investor interest in top-tier hotel transactions in the Denver area. The following article provides insight into how these trends are likely to affect Denver’s hotel market in 2011 and beyond.

Hotel Performance

Upscale and luxury hotel markets across the U.S. slipped to their nadir in 2009 as the recession and negative public perception steered would-be higher-rated demand toward more modestly priced hotel tiers. An HVS analysis of a set of 15 upscale, upper-upscale, and luxury hotels in Downtown Denver and Cherry Creek revealed a RevPAR decrease of nearly 18% in 2009, the cumulative consequence of constrained demand channels and rate discounts.

The upper-tier Denver hotel market illustrated its resilience in 2010 as RevPAR rebounded nearly 14%, fostered predominantly by resurgence in demand. Like many urban U.S. markets, local average rates began to strengthen during the summer of 2010; however, multi-year contracted corporate and group rates, which had been negotiated at deep discounts during the worst of the recession, continued to pose a challenge for local hotels.

The graph below illustrates RevPAR performance for 15 full-service Denver-area hotels from 2000 to 2010.

HISTORICAL HOTEL REVPAR:

SELECTED DENVER UPSCALE, UPPER-UPSCALE, AND LUXURY HOTELS

.jpg)

Recent Transactions Trends

Nationwide, economic uncertainty and declining hotel performance, coupled with the higher costs and limited availability of capital, contributed to lower hotel sales prices per room. In 2009, the U.S. hotel transactions market came to a virtual standstill, with fewer transactions recorded than in any one of the previous 19 years.

In 2010, acquisition strategies of newly formed and existing REITs and private equity groups, as well as the easing of capital markets, increased investor confidence in the hotel sector, with interest targeting trophy assets, gateway cities, and primary markets. Strong improvements in lodging industry performance vectors also helped stimulate interest among investors, as borne out by the U.S. transaction data HVS compiled for 2010: the total number of 2010 transactions more than tripled that of 2009, and the average price per room increased by over 45%.

Local sales of top-tier hotels were generally limited to the Colorado mountain resorts in 2010 and included the following transactions:

2010 TOP-TIER COLORADO HOTEL TRANSACTIONS

.jpg)

Denver Hotel Performance and Transactions Trends: 2011 and Beyond

The selected set of full-service hotels in Downtown Denver and Cherry Creek maintained moderate (4%) RevPAR growth through April of 2011. The upper-upscale Embassy Suites and the luxury Four Seasons opened in late 2010, amounting to a 12% increase in supply, yet demand grew by nearly the same amount. Occupancy remained stable as a result, allowing for moderate average rate increases—a step in the right direction for hoteliers seeking to push rate. Because of heightened rate competition among top-tier Denver hotels, rate-driven RevPAR gains are likely to stay around 4% through the end of 2011. Rising room rates, supported by increased demand compression, should lead to greater year-over-year RevPAR gains in 2012.

Full-service hotel transactions have already gained momentum in 2011, driven in part by the improving hotel performance trends that took hold last year. Equity interest in the full-service hotel sector has continued to grow in 2011, and debt is increasingly available. The attraction of more investors and sellers to the market should push 2011 transactions activity well above the levels recorded in 2010.

Notable sales of full-service Denver-area hotels in the first half of 2011 include the following:

2011 TOP-TIER COLORADO HOTEL TRANSACTIONS

.jpg)

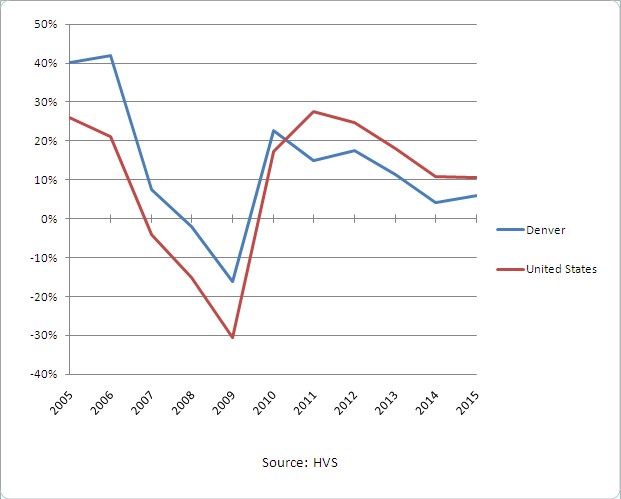

Stability of Denver Hotel Values

The following graph illustrates information on the historical and projected changes in per-room hotel values for the greater Denver market versus the U.S. as a whole.

HOTEL VALUATION INDEX (HVI) 2011

The HVS Hotel Valuation Index (HVI) tracks hotel performance, sales transaction activity, and hotel values in 51 major metropolitan hotel markets across the U.S. Among these markets, Denver tied for seventh in terms of stability, reflecting one of the smaller value changes between 2006 and 2009. U.S. hotel values decreased at almost twice the rate of Denver hotel values in 2009; Denver-area hotel values have also been quicker to rebound1 . The JW Marriott Cherry Creek provides a telling illustration: between the sale of the property at the market peak in 2006 and the subsequent sale in May of 2011, the hotel’s value increased 2.3%. Given the ravages of the recent recession on hotel values nationwide, this increase is especially remarkable and serves as one sign among several that Denver’s hotel market is poised for a strong recovery.

Conclusion

The recalcitrance of average rate for Denver’s top-tier hotels remains the most difficult obstacle to overcome on the path to recovery. Nevertheless, demand, transactions, and values continue to climb, and data show that local hoteliers have regained some pricing power. As access to capital and investment channels continues to broaden, we expect to see more investor interest in Denver-area upscale, upper-upscale, and luxury hotels, especially given recent performance trends. For more insights on the market please contact Bethany Cronk, MBA ([email protected], 720-837-8328) or Tess Federer ([email protected], 847-727-4781).

1 As of year-end 2010, values for Denver-area hotels had risen approximately 23% over the previous year, versus an approximate rise of 17% for the nation as a whole.