Hotels and the hospitality market are constantly evolving as a result of brands consolidating, owner profiles changing, technology disruption, changing traveler behavior as well as hotel investment trends altering.

The 2019 HVS Middle East Valuation Index highlighted declining hotel values in the Middle East as a result of several factors but most importantly oversupply and increased competition, declining RevPAR and increasing costs.

Consequently, all these shifts in the industry transformed the traditional relationship between owners and operators, which were reflected in the way hotel agreements were negotiated and have resulted in the emergence of alternative agreements.

Since 2005, there has been a considerable increase in hotel developments in the Middle East, and global operators have significantly contributed to growing the hospitality offering supported by aggressive tourism initiatives led by the key cities in the region. Some key cities have witnessed double-digit growth in tourist arrivals and the number of branded hotels was circa 700 hotels or approximately 210,000 hotel rooms by the end of 2019 in the region. New supply was estimated to add some 70,000 hotel rooms by 2025, with most hotel supply planned for the United Arab Emirates and the Kingdom of Saudi Arabia.

A recent HVS survey of the key global operators in the Middle East region shows that 84% of branded hotels operate under a management agreement, 11% operate under a franchise agreement and 5% are leased properties. New signings show an increase in franchise agreements to approximately 20% and the trend suggests that hotel owners in mature markets will look to convert the current hotel management agreements into franchise agreements at the end of the initial term, and in some instances earlier in the term subject to operator’s approval. In comparison, 25% of hotels operate under franchise agreement in Africa, 40% in Europe and close to 70% in the US.

Major changes in hotel management agreements were observed in signings post 2010 and we take the view that further changes are anticipated as there is increased pressure on operators to secure development opportunities while owners’ expectations have drastically shifted, especially in the last couple of years.

This publication summarizes the evolution of a number of key terms in hotel management agreements and our outlook on how these key terms may evolve in the future. Furthermore, it provides an overview of franchise agreements and highlights alternative agreements that are being considered by sophisticated owners in the Middle East region.

.png)

Management Agreements

In the last 15 years, the GCC region specifically witnessed a tremendous increase in new hotel developments, the majority of which were subject to management agreements with international operators. Some local brands have also grown their regional footprint through hotel management agreements. Historically, most new hotel developments attracted upscale and luxury brands, with a noticeable increase in midscale and economy brands in the last 3 to 5 years.

Term & Base Fee

- The average initial term for contracts signed in the Middle East after 2008 dropped from 21 years to 17 years when compared to a global average of 18.3 years. Luxury and upscale brands usually have a longer term when compared to the midscale brands. The length of the term is typically negotiated and tied to the commercial fees offered, which is typically represented by an inverse relationship.

- The base management and license fees only consider the top line of the profit and loss statement and therefore may not necessarily incentivize the operator to minimize the operating expenses and increase the bottom line. Historically, base fees were a flat fee, ranging from (2% to 4%) over the term of the agreement and are largely a function of the size and positioning of the property. More recently, signed contracts include a base fee ramp up in the initial years of operations until the hotel is stabilized. The scaled up average base fee in the Middle East is 1.7% of Gross Operating Revenue (GOR) which is lower than the global average base fee of 2.6%.

.png)

Incentive Fee

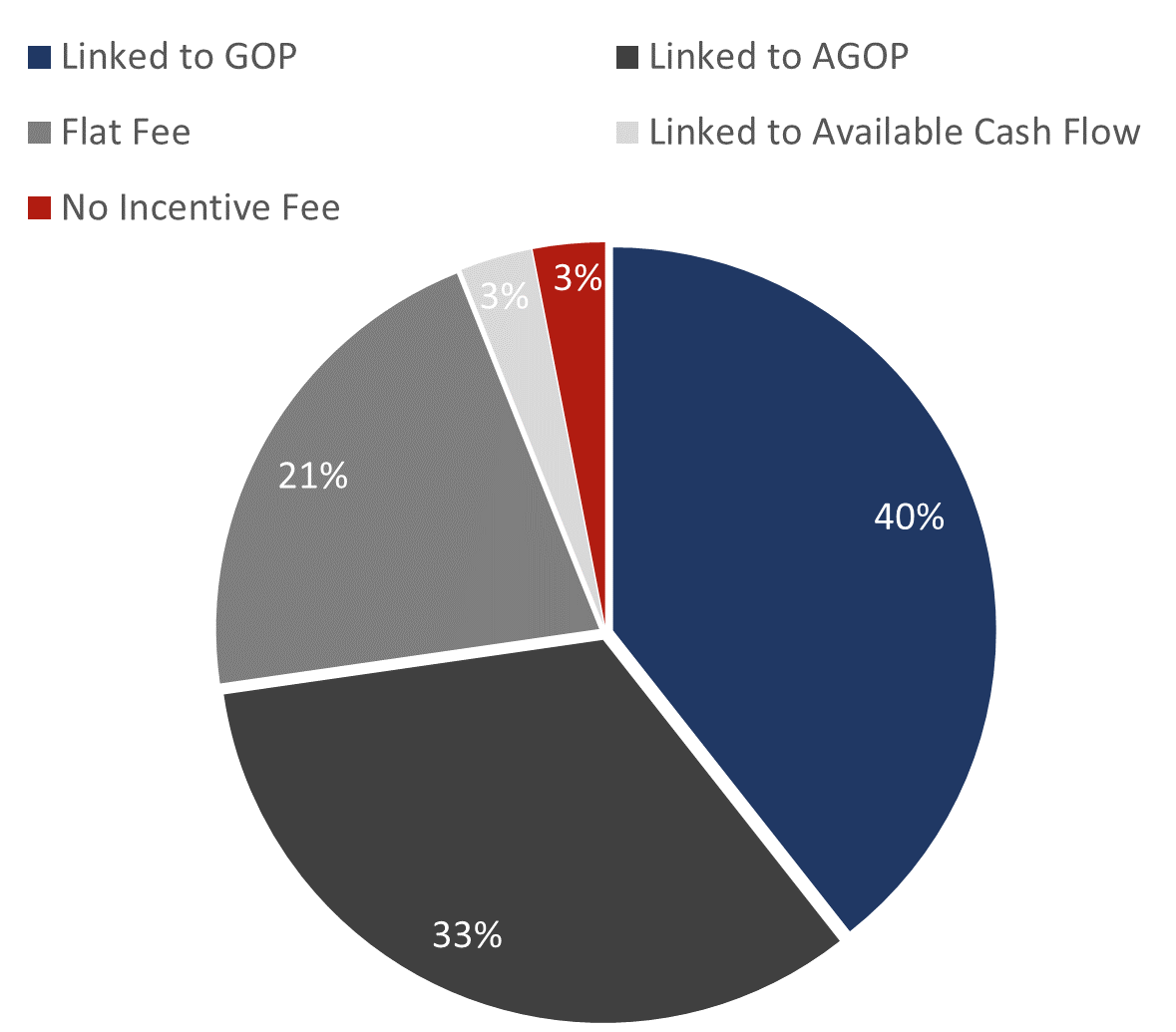

- While the base management fee motivates the operator to focus on the top line, the incentive fee encourages the operator to manage and control the operating expenses. There are several forms of incentive fee structures, but the most common in recent years is the scaled incentive fee linked to the Gross Operating Profit.

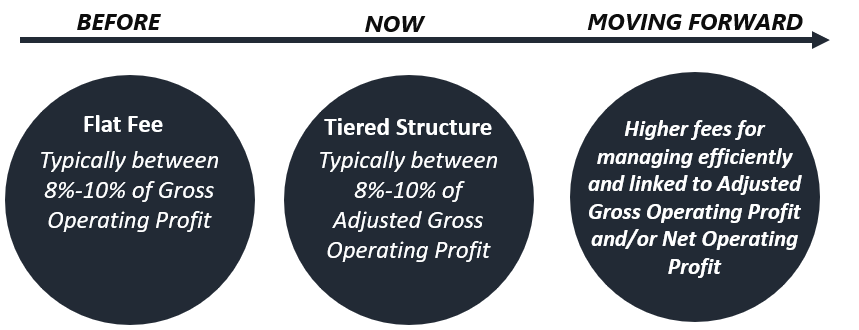

- Historically, incentive fees were flat and ranged between 8% and 10% of Gross Operating Profit. Approximately 73% of reviewed contracts, which were signed after 2008, show a noticeable shift to a scaled incentive fee structure, typically starting at 5% and increasing to 9% based on Gross Operating Profit and Adjusted Gross Operating Profit brackets.

- More recently incentive fees are being tied to the operator achieving a minimum AGOP level of 15% to 20%.

- Definition of Gross Operating Profit and Adjusted Gross Operating Profit have also changed in the last few years. In several contracts, the definition of AGOP includes FF&E deduction and some additional expenses that are agreed with owner.

- As the hotel market matures and owners become more aware of the mechanisms to guarantee acceptable levels of returns on their investments, owner’s priority clause, performance guarantee and maximum fee cap are likely to become the norm.

Minimum Guarantee

Maximum Fee Cap

In recent years, an increasing number of hotel operators accepted capping the sum of the base and incentive fees to acquire the management rights of the strategic assets in the Middle East. The maximum fee cap range varies between 4% and 7% of the Total Revenue based on the project characteristics and the fee generation potential for the operator.

Higher incentive fees to compensate operators when achieving healthy AGOP levels will likely become the norm to incentivize the operator to manage more efficiently. It is also likely that hotel owners will also link the incentive fee to Net Operating Profit or owner’s priority especially in the current unpredictable changes to the hospitality market and the declining EBITDA levels.

Group Services Fee

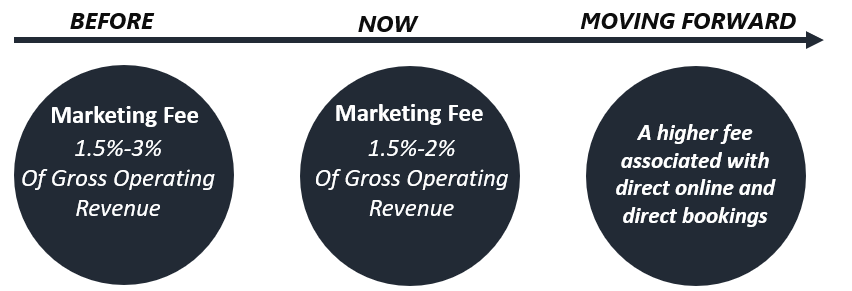

- It is observed that the more developed the brand service systems are, the higher are the fees. On average, a well-established upscale brand charges a marketing fee ranging between 1.5% - 3% of Gross Operating Revenue whereas brands with relatively less established services could charge as low as 0.75% on Gross Rooms Revenue.

- Operators also charge a reservation fee as part of the group services fee. Depending on the source of reservation, the fee can be charged in different forms such as percentage of gross room revenue, fixed fee based on available rooms or fixed fee charged per reservation. Average reservation fee in the Middle East as a percentage of the gross rooms’ revenue is 1% whereas the average for fixed amount per reservation received is USD 9.

As operators acknowledge that direct bookings are rather lower than those booked through other established platforms such as Expedia and Booking.com, additional efforts in recent years have been made to boost direct bookings and reduce reliance on third party platforms. Also, in certain markets, the largest share of bookings is driven by the local sales team which also results in a high marketing and sales cost at the property level. Combined with the Group Marketing fee, this could total approximately 8% of total revenues.

We take the view that operators will have to reassess those fees in response to the new realities and booking dynamics. A higher fee associated with direct online and offline bookings would incentivize the operator to increase its efforts to channel bookings through its own direct mediums, reduce commission pay outs and drive higher profitability.

Area of Protection

Hence, for the owner’s protection, in the majority of the contracts reviewed a territorial restriction is imposed on the operator, where the operator is unable for a specified number of years or throughout the full initial term, to franchise, lease, operate or affiliate with another property with the same or similar brand as of the subject property.

There are two main factors to consider while negotiating the area of protection (AOP). These factors are the duration and the size of the area of protection, which is mostly defined by a radius. As a rule of thumb, the higher the market positioning, the bigger the area of protection. Deciding the radius of a territorial restriction depends on several factors but most importantly the city and future development opportunities.

In some markets in the Middle East, operators are willing to sign only a 3 to 5 km radius as opposed to other markets where the area of protection covers the entire city. The positioning of the hotel plays a key role in the negotiations of this term. Typically, midscale and budget brands are more lenient when compared to upscale and luxury brands. However, the management fees that are forecasted to be generated by the subject property are also a key factor in identifying the owner’s bargaining power. Consequently, if the forecasted operator fees are higher, then the owner is likely to negotiate a bigger radius of AOP. Recent acquisitions and brand consolidation have worked in operators' favor in growing further even in markets where strict AOP have been negotiated.

From an owner’s perspective, the consolidation between operating companies which typically results in an increase in number of hotels/brands under the same platform may dilute the property’s market share rather than allow the brand to capitalize its market presence. It is also arguable as to whether economies of scale could be achieved, especially when the investors/owners of similar branded properties are different.

We take the view that there will be less emphasis on Area of Protection in future contracts, on the account of owner’s ability to reduce the term and link the operator’s fees to AGOP and NOP.

Performance Tests

These tests, if negotiated and agreed in the right manner, grant the owner the right to terminate the contract in case the operator is underperforming within its competitive market or consistently failing to achieve the approved operating budget.

As owners have become more sophisticated and hotels' trading performance has been challenged in the last couple of years, performance tests have become more prevalent. Exit strategy and termination rights gained more importance which also resulted in performance test thresholds becoming stricter and more enforceable.

Although hotel management contracts in the Middle East, since the 90’s, have gained popularity as they allow both parties to maximize returns, rarely has the operator been held accountable for operating shortcomings while owner bears all the financial risk. Since operators are accountable and responsible for the hotel’s performance which in turn impacts the owner’s income potential, owners now expect to have the right to terminate the contract without paying damages or terminate when the operator underperforms. However, if the performance failure occurs in case of a force majeure event, extraordinary events and/or renovation, the owner’s right to terminate cannot be executed.

86% of the Middle East hotel agreements sample set included a performance test in the agreements. The reason why the performance test seems more prevalent in this region is due to the nature of the sample set used for this article. All contracts which did not include a performance test clause from the Middle East reviewed sample were signed before 2007.

There are several factors to take into consideration while imposing a performance test. These factors include commencement year, test period, performance thresholds and operator’s right to cure.

- Commencement Year and Test Period: The testing period typically kicks in once the property is stabilized, which is 3 to 4 years from the hotel opening. Most contracts reviewed have a performance test which stipulates two consecutive years of failure.

- Revenue Per Available Room (RevPAR) parameter usually expects the operator to achieve a RevPAR level that is equal to or more than the pre-defined threshold, which is usually in the range of 85%-95%, of the weighted average RevPAR of the subject property’s mutually agreed competitive set. The main difficulties of RevPAR test are defining the right competitive set along with obtaining reliable data regarding the RevPAR of that competitive set.

- Gross Operating Profit (GOP) parameter typically expects the operator to achieve a GOP level that is equal to or more than the pre-defined threshold, which is also in the range of 85%-95%, of the mutually agreed budgeted GOP.

- The most agreed performance tests in the reviewed contracts are “dual” and “collective” testing, whereby the operator is considered to have failed when it fails both RevPAR and GOP test for two years consecutively from the commencement date. In rare cases, the agreements included either GOP or RevPAR as single tests.

The cure amount equals to the difference between the actual performance and the approved budgeted GOP. In some cases, the management company provides the cure amount in cash or alternatively sets off the cure amount from the next management fee due.

Although the cure amount is usually the last year of the failed test period, current trends indicate that the higher of the two years can be cured as well. Mostly, the cure amount will be the variation of GOP and budgeted GOP, as curing the RevPAR test would include several hypothetical variables.

Once the operator uses its right to cure, the contract remains in effect and the owner’s termination notice regarding the failed test period is no longer valid. Only if the operator does not cure its failure or exceeds the maximum number of rights to cure, then the owner can terminate the contract.

These parameters can be set in motion independently, separately, or collectively. Although the collective tests are the most common, which makes it more difficult for operators to fail and owners to terminate, owners are pushing for single and separate tests while the operators are resisting the same. In the latter, failing either one of the test parameters would grant the owner’s termination notice to hold merit.

To date, there have been only few instances in the Middle East region in which the owner was able to enforce the performance test and terminate an operator for failing the tests. The changes in market dynamics also present an opportunity to explore whether the RevPAR remains a good indicator of the operator’s ability to manage efficiently and create value.

Key Money Contribution

Key money can be offered in a variety of formats, including;

- An absolute monetary amount estimated as a percentage of the Net Present Value (NPV) of the operator’s fees that it expects to earn over the life of the contract, or not exceeding two to three times the stabilized year’s management fees anticipated to be earned by the operator. The amortized key money is often claimed back by the operator if the management contract is terminated prematurely on a pro-rated basis.

- A waiver of the technical services fee or making it reimbursable after the hotel opens in the form of key money.

- Foregoing base and / or incentive fees for a specified number of years with or without a claw back provision as a key money incentive.

.png)

This shift also stems from owners' convictions that they have a stronger ability to manage and reduce the operating costs of running a hotel when compared to the international operators ability to create efficiencies and reduce costs in the local market, especially in emerging and secondary cities. Equally, operators recognize the opportunity to expand the brand footprint in growing economies while mitigating some of the commercial risks and significant capital investment.

Major international hotel operators such as Hilton, Marriott, IHG and Accor amongst others are entertaining and accepting this operating model as an option to grow further subject to the owners’ ability to maintain brand standards and expect owners to have a management team experienced in hotel operations or hire a qualified third-party manager.

Brand attributes play a crucial role in a hotel investor’s choice of franchise affiliation. When evaluating a potential hotel franchise, one of the important economic considerations is the structure and amount of the franchise fees.

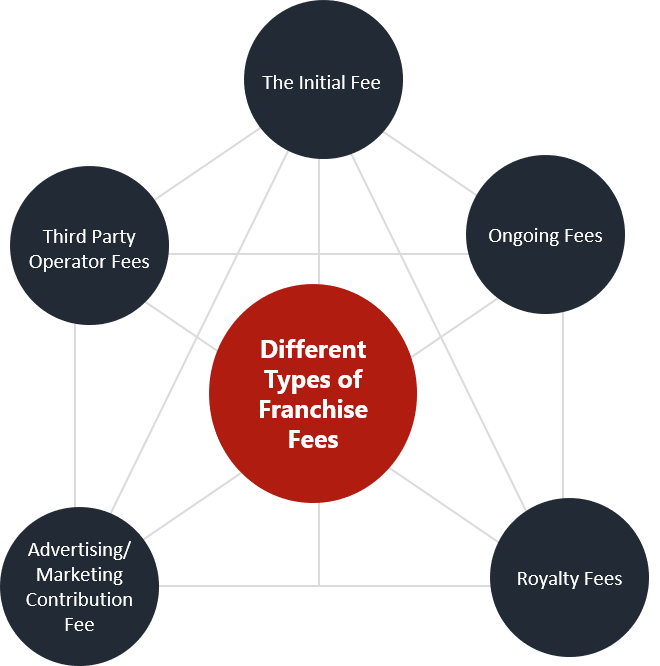

Second only to payroll, franchise fees are among the largest operating expenses for most hotels. Hotel franchise fees are compensation paid by the franchisee to the franchisor for the use of the brand’s name, logo, marketing, and referral and reservation systems. Franchise fees normally include an initial fee with the franchise application, plus ongoing fees paid periodically throughout the term of the agreement.

The typical term of a franchise agreement ranges from 10 to 15 years and the franchisor would typically have the rights to terminate in case the franchisee fails to meet brand standards service requirements.

In certain instances, especially with existing hotels, the Franchisor may also require property investment plan and expenditure to align the hotel quality and offering with the brand image.

Typically consists of a minimum dollar amount based on the hotel’s room count. For example, the initial fee may be a minimum of USD 45,000 plus USD 300 per room for each room over 150. Thus, a hotel with 125 rooms would pay USD 360 per room, and a hotel with 200 rooms would pay USD 300 per room. In cases of re-flagging an existing hotel, the initial fee structure is occasionally reduced or waived. Some franchisors will return the initial fee if the franchise is not approved, while others will retain approximately 5% to 20% to cover administrative costs.

Fees commence when the hotel assumes the franchise affiliation, and fees are usually paid monthly over the term of the agreement. Continuing costs generally include a royalty fee, an advertising or marketing contribution fee, and a reservation fee. In addition, ongoing fees may include loyalty memberships fees and miscellaneous fees.

A royalty fee represents compensation for the use of the brand’s trade name, services marks and associated logos, goodwill, and other franchise services. Royalty fees represent the major source of revenue for the franchisor. These fees are characteristically subject to negotiations between both parties, and can vary by brand, but typically range from 3.0% to 5.0% of rooms revenues. In some instances, franchisors require an additional percentage of other revenue streams, most commonly food and beverage revenue. In these cases, the average amount is 1.0% to 2.0% of total food and beverage revenue (or sometimes all non-rooms revenue), and this is payable on top of the room revenue in certain agreements. If included in the contract at all, F&B and non-rooms revenue fees are more often found in upscale and luxury brands rather than midscale and budget brands.

Brand-wide advertising and marketing consists of national or regional advertising in various types of media, including the Internet, the development and distribution of a brand directory, and marketing geared toward specific groups and segments. In many instances, the advertising or marketing contribution fee goes into a fund that is administered by the franchisor on behalf of all members of the brand. Like the Group Services Fee in hotel management agreement, franchisees ideally want their contribution to impact their region, which may not always be the case.

These fees normally range from 1.0 to 2.0% of total revenue. These fees typically vary by market and in some instances are paired with the reservation fee.

Owners equally may be required to hire a third-party operator to manage the day to day operations. Hiring a third-party manager with local market knowledge gives assurance to the franchisor on one hand and allows hotel owners with limited or no hotel experience to manage efficiently. Third party operator fees typically range between 4% and 6% of total revenues and are structured in a similar fashion to the traditional hotel brands (base fee and incentive fee). Additional details on third party managers is included in the section below.

Clearly, franchise agreements have become more established in mature markets across the US and Europe and are increasing in popularity and acceptance in the Middle East region. While this operating model is expected to replace some of the old contracts and allow owners more control to optimize the value of the asset through top line enhancements and reduced costs, owners need to evaluate the depth to which a franchise agreement can provide a hotel with recognition, operational support, return on investment, and success.

Figure 7: Franchise Fee Types

Independent hotel collections offer the marketing and reservation platform of their parent company, but the development standards and facility programming tend to be more defined and rigorous. The fee structure for these collections appears to be in line with those of similar chain-scale-ranked hotels within the respective parent company. Such hotel companies offer a flexible option for owners who seek to maintain the independent positioning of their property but affiliate with a group boasting national or international recognition and corporate accounts. The properties that comprise these “independent” and “soft brands” portfolios are typically first-class, full-service hotels, often with a smaller guestroom inventory than the norm.

One of the largest discrepancies between independent hotels and the traditional franchise model is the application of fees toward revenues. While a typical franchise applies stipulated fees to total rooms revenue, independent hotel companies only apply fees to reservations that stream through their channels. This is typically a reduced portion of total reservations, which can vary greatly per hotel depending on the product or market type (e.g., resort-style hotels, urban markets etc.). However, the overall “franchise” cost to an owner for an independent hotel would consider only those reservations and revenues derived from the independent hotel company.

Third Party Management Agreements

While this business model is very well-established in North America and growing rapidly in Europe, it is still in its early stages in the Middle East, Asia Pacific, and Africa.

Third-party management companies are loyal to the owner, where branded operators are loyal first and foremost to the brand. While it is not implied that branded operators ignore the owners’ interests entirely, they do have different priorities. Brand managers will aim to present their brands in the best possible light and may omit to achieve the type of bottom-line profitability that third-party operators are more concerned of.

Flexibility is another key strength of third-party operators. As hotel chains impose certain restrictions and brand standards that a hotel must conform to such as property size, facilities, location etc., third-party operators offer more flexibility and adapt more easily to the specific needs and requirements of the owner especially when it comes to independent properties. Owners would also have more influence and control on the operation with a third-party than with a branded operator.

The terms of a third-party management agreement are also characteristically more competitive and flexible than those of the brands. Typically, management fees, both base and incentive fees, are lower for independent operators. The initial term of the management agreement is much shorter (starting at a minimum lock in of five to ten years) and exit options are more flexible (including termination at will).

A third-party management agreement is an obvious choice for unbranded, independent properties, but can also be a valuable inclusion for franchised hotels, as there remains a gap between owners that are unable or unwilling to control the daily operations of the hotel and the hotel chains who are focusing on expanding their presence via the franchise model. Due to the challenge of hotel owners and franchisors to ensure that their mutual interests are in capable hands, the third-party management model has come into prominence.

Although implementing a franchise agreement and a third-party management agreement moves hotels into a double fee scenario (owners would have to pay franchise fees to hotel brands on top of management fees paid to third-party operators), owners are willing to accept this business model for the flexibility of the management contract and more control over the operations. The flexibility also adds to the value proposition when it comes to the sale of the property. For owners of multiple hotels under different brands, selecting a single third-party operator allows for homogenous reporting across all properties, increasing the ease of comparing performance across the portfolio.

Manchise Agreements

From the operators’ perspective, manchising minimizes the risk of diluting the brand equity as opposed to franchise agreements since it enables the operator to establish strict operating controls in the initial years. Hence, some luxury, upper-upscale and lifestyle brands which may not be immediately available for franchising due to the operators’ concerns on maintaining the brand standards can be acquired through manchising agreements. It should also be noted that some of the Tier 1 operators accept manchising agreement on the condition that the owner accepts to appoint a third-party operator who has extensive experience in managing branded hotel operations.

A manchise is a complex agreement where the right to execute to convert into a franchise is typically granted to the owner by the Operator, unless negotiated to be guaranteed after a specified period. Aligning the objectives between the two parties also increase the legal complexity of the agreements. Typically, two sets of agreements are signed between the owner and operator with a typical length of the management agreement being 5 to 7 years. It is also common that the fees payable to the operator are higher during the management term to compensate for the shorter length of the agreement.

Despite the complexity of entering into two sets of agreements, this model is considered to be advantageous to owners who require a greater control of the operations of their hotel and may not be ready to enter into a franchise agreement from the early start. As discussed previously, the “Manchise: Management-Franchise” concept is gaining popularity though it is too early to comment on issues arising at the end of the management term and the start of the franchise term.

Lease Agreements

Under a lease agreement, the owner is the landlord and has no operational responsibilities. The lease agreements provide the most risk-averse operating model for owners with minimum financial risk and a relatively stable income stream. In addition, predictability of the lease income over a certain period provides the owners with the ability to seek financing at more favorable terms. The main disadvantages of the lease agreements for the owners are the opportunity cost of higher potential returns if the hotels perform well and the lack of control over the operation of the asset.

On the other hand, the majority of the hotel operators do not have the same appetite for lease agreements due to their asset-light business model. Under a lease agreement, the operator incurs all operating financial risk. Fixed lease expenses for the operators are considered as liabilities in their balance sheet which do not bode well with their risk-averse strategy. Nevertheless, some operators within the economy segment as well as new operators that are yet to establish their brand in the region consider lease agreements as opportunities to expand their footprint in the Middle East. While the model has not been tested by most of the operators in the region, we are of the opinion that the lease agreements provide an appealing alternative model for the operators who are willing to take risks for higher returns and strategic expansion of their brands.

The length of the lease agreements are typically shorter as opposed to management and franchise agreements. Under a lease agreement, there are different rent structures depending on both the owner’s and the operator’s risk appetites. These structures include fixed fee, share of revenue, and share of net operating income.

- Fixed fee is a fixed rental payment with indexed growth over a certain period. Under the fixed fee structure, the owner bears the minimum risk as the income stream is not contingent upon the performance of the property.

- Share of revenue is a variable lease structure wherein the rent is calculated based on the revenue generated in a year. Both operator and owner share similar level of risk under this structure as the rent is linked to top-line performance of the hotel.

- Share of Net Operating Income is another variable lease structure wherein the rent is calculated as a percentage of the net operating income. Under this structure, the risk for the hotel owner is relatively higher since the income stream is not only dependent on the top line but also operator’s ability to manage expenses and drive bottom-line performance.

In conclusion, while the interest in lease agreements have been mainly from the owners with little enthusiasm from the operators, we believe the lease model has the potential to offer significant benefits to both owners and operators in the Middle East.

Concluding Thoughts:

Disclaimer: This publication, is not intended to provide any recommendation and should not be relied upon for decision making, as each hotel is unique, and a number of factors need to be considered when making a choice of hotel brand and the most suitable hotel operating agreement.

Our team of experts would be pleased to assist and advise you. For more information please contact the authors.

About Hala Matar Choufany

Hala is an experienced Regional President and Managing Partner, an industry expert, and is recognized as one of the most influential leaders in the hospitality industry, notably in the Middle East and Africa region.

Hala has advised on more than 5,000 hospitality and mixed-use projects in the last 20 years across Europe, the Middle East, Africa and Asia. She has advised clients in areas such as Valuations, Acquisitions, Asset Management, Strategic investments and development, Contract Negotiations, and general Real Estate Strategic Advisory.

Hala has authored more than 50 publications and speaks frequently at investment and hospitality related conferences on a range of topics including asset valuation, investments, management issues and women leadership.

In addition to being a Board Member of HVS Global, Hala sits on the Boards of Harvard Business School Club of the GCC, Hotel Investment Advisory Board, and is regularly invited to Boards as a subject matter expert in the industry. Hala is frequently invited to discuss hotel and tourism trends on major news channel including Alarabiya, Bloomberg, Abu Dhabi TV, Forbes, Breaking Travel News and CNN.

Hala is also a member of the International Society of Hospitality Consultants (ISHC).

Hala completed Executive Education at Harvard Business School. She also holds an MBA in Finance and Strategy from IMHI (Essec- Cornell) University, Paris, France and a BA in Hospitality Management from Notre Dame University, Lebanon. Hala is fluent in English, French and Arabic.

Born in Beirut, Hala lived and worked in several cities across Europe, Asia and Middle East and is a mother of three.

For more information, contact Hala at [email protected].

0 Comments

Success

It will be displayed once approved by an administrator.

Thank you.

Error